MNI EUROPEAN MARKETS ANALYSIS: RBA Aug Cut Nearly Fully Priced

- Trump reiterated that he would like Powell To resign, but stated he has been told financial markets will react if he fires the Fed Chair. Trump also stated many small countries will have a tariff rate of 10% or 15%.

- Australian jobs data missed, while the unemployment rate rose to multi year highs, weighing on the AUD and local yields. A 25bp rate cut in August is given a 98% probability, with a cumulative 63bps of easing priced by year-end.

- Japan exports fell in y/y terms for the second straight month, while verbal jawboning on FX emerged today as well (market impact was limited).

- Looking ahead, the May UK labor force data is out, while in the US retail sales and initial jobless claims are out.

MARKETS

The TYU5 range has been 110-13+ to 110-20 during the Asia-Pacific session. It last changed hands at 110-14, down 0-06 from the previous close.

- The US 2-year yield has edged higher trading around 3.906%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.477%, up 0.02 from its close.

- The 10-year yield has broken above 4.45% in response to the CPI Data, this implies price is likely to turn its focus back to 4.65% and could see further paring back of longs. Support is now back towards the 4.35/40% area which has been the pivot in the larger 4.10% - 4.65% range.

- Nick Timiraos on X: “Removing Powell as Fed chair could lead to a messy, drawn-out standoff. The Fed owns its buildings and controls its security. If Trump attempts removal, Powell could try to stay until the courts uphold it or the Senate confirms a replacement.”

- FED'S WILLIAMS: IT'S NOT SURPRISING THAT TARIFF IMPACTS HAVE BEEN GROWING, NOT SURPRISED TARIFF IMPACTS MODEST SO FAR THERE'S BEEN GOOD NEWS ON SERVICE SECTOR INFLATION, UNDERLYING DISINFLATION PROCESS STILL UNDERWAY" - BBG

- "FED'S WILLIAMS: WITHOUT TARIFFS INFLATION WOULD BE CLOSING IN ON 2% - [RTRS]"

- (Bloomberg) -- “JPM stops out of 10s/30s flatteners on the extent of the recent move and lingering headline risk, though the strategists still say the long-end of the curve appears too steep at current levels.”

JGBS: Twist-Steepener, US Tariff Impact In Trade Data, Natl CPI Tomorrow

JGB futures are little changed but near session highs, +2 compared to settlement levels.

- (Dow Jones) “Japan's exports fell for a second straight month in June, fueling fears that U.S. tariffs will halt the nation's economic recovery and complicate the central bank's policy plans. Exports fell 0.5% compared with the same period a year earlier, according to the Ministry of Finance on Thursday. That was an improvement from May's 1.7% drop but well short of an LSEG-compiled forecast for a 0.5% increase.”

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs have twist-steepened across benchmarks, with yields 2.3bps lower (10-year) to 2.2bps higher (30-year). The benchmark 10-year yield is at 1.562% versus the cycle high of 1.60%.

- (Bloomberg) -- Japan's mounting debt burden and an election that risks making it worse are fuelling debate on whether the nation's sovereign credit rating may be cut sooner rather than later.

- Swap rates are 1bp higher to 2bps lower, with a flatter curve.

- Tomorrow, the local calendar will see Natl CPI data.

JAPAN DATA: Exports Fall Y/Y For Second Straight Month, Below Forecasts

Japan June export growth was marginally below market forecasts. We printed at -0.5%y/y (+0.5% was forecast and -1.7% was the May outcome), while imports were slightly stronger relative to expectations, up 0.2%y/y, versus -1.1% forecast and -7.7% in May. This saw the trade balance print at ¥153.1bn, below market forecasts of ¥353.9bn. In seasonally adjusted terms the deficit was at -¥235.5bn, which was close to market expectations (-¥274.7bn).

- This was the first y/y back to back export falls since Q3 2023. In volumes terms exports were better though (+2.5%y/y).

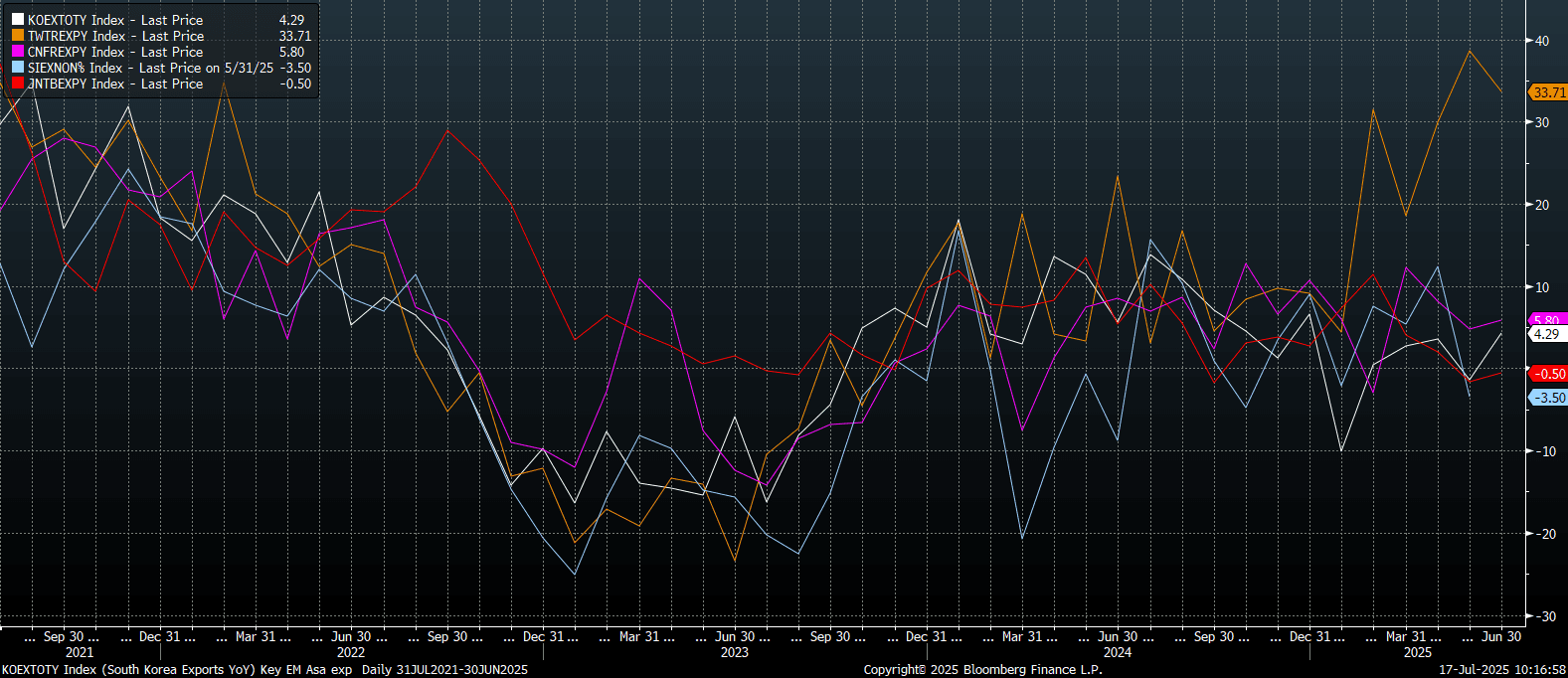

- Japan's export trend is slightly underperforming the likes of China and South Korea, where growth is modestly positive. For the region, Taiwan remains the standout performer, see the chart below (note Japan is the red line on the chart).

- Japan exports to the US fell by 11.4%y/y, while in volume terms we were -1.6%y/y for exports to the US. The trade surplus with the US widened modestly on the May outcome to ¥669.26bn, but is still below end Dec levels (over ¥1trln).

- This comes as both sides try to reach a trade deal before the Aug 1 deadline.

- Export to China were also down, -4.7%y/y, but better to the EU, up 3.6%y/y.

Fig 1: Key Asian Economy Export Growth - Y/Y

Source: Bloomberg Finance L.P./MNI

JAPAN DATA: Japan Investors Continue To Buy Offshore Bonds

Japan outbound flows were mixed in the week ending July 11. Local investors continued a strong run of purchasing offshore bonds. We had another ¥759.3bn in net purchases last week. Since the middle of May this brings cumulative net buying in this space too nearly ¥4.8trln. We have seen 5 consecutive weeks of net buying to overseas bonds. The focus will be on whether these trends are sustained, particularly given the roll over in global bond returns since the start of the month, as US yields have rebounded higher.

- Local investors did sell overseas equities for the second straight week in decent size. This brings net selling in this space to 8 out of the last 9 weeks.

- In terms of inflows into Japan bonds/equities from offshore investors, trends were positive but in lower absolute levels. Appetite for Japan equities remained strong, with cumulative inflows into this space since early April at just over ¥8.4trln, with only one week of net outflows during this period.

- Offshore investors purchases local bonds, but this just offset modest outflows from the week prior.

Table 1: Japan Offshore Weekly Investment Flows

| Billion Yen | Week ending July 11 | Prior Week |

| Foreign Buying Japan Stocks | 446.0 | 611.5 |

| Foreign Buying Japan Bonds | 170.4 | -167.8 |

| Japan Buying Foreign Bonds | 759.3 | 1659.1 |

| Japan Buying Foreign Stocks | -767.9 | -514.4 |

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Holding Post-Jobs Gains, Nov-31 Supply Tomorrow

ACGBs (YM +8.0 & XM +5.0) are holding +4-7bps after a weaker-than-expected June Employment Report.

- The Australian June jobs report was below market expectations. Jobs growth was just +2k, versus +20k forecast, after a revised -1.1k fall in May (originally reported as a -2.5k fall). The unemployment rate rose to 4.3% against a 4.1% forecast and 4.1% May outcome.

- (AFR) But it’s the momentum in the jobs market that should worry Bullock and the RBA board. The underemployment rate rose from 5.9 per cent to 6.0 per cent. The underutilisation rate jumped from 10.1 per cent to 10.3 per cent. And hours worked dropped by 0.9 per cent month-on-month in June. (via BBG)

- Cash ACGBs are 5-8bps richer on the day, 3-6bps richer post-data, with the AU-US 10-year yield differential at -12bps (-3bps pre-data).

- The bills strip has extended its bull-flattener after the data, with pricing +6 to +9.

- RBA-dated OIS pricing is 2-10bps softer across meetings today. A 25bp rate cut in August is given a 98% probability, with a cumulative 63bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$1100mn of the 1.00% 21 November 2031 bond.

AUSTRALIA DATA: Jobs Growth Modest U/E Rate Up To Late 2021 Levels

The Australian June jobs report was below market expectations. Jobs growth was just +2k, versus +20k forecast, after a revised -1.1k fall in May (originally reported as a -2.5k fall). Full time jobs fell -38.2k, after a revised 41.9k gain in May. The opposite trend occurred in part time jobs, with +40.2k created in June, after a revised -43k fall in May. The unemployment rate rose to 4.3% against a 4.1% forecast and 4.1% May outcome. This move was aided by a slight rise in the participation rate to 67.1% (67.0% was forecast).

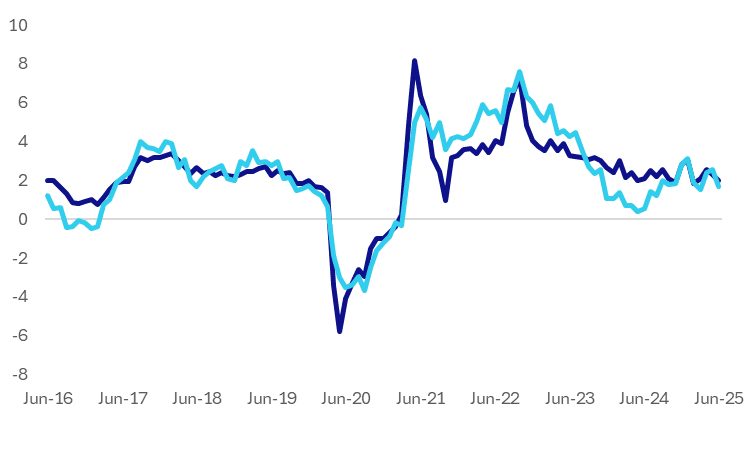

- The first chart below overlays Australia total employment growth and full time employment growth, both in y/y terms. Aggregate jobs growth at +2%y/y is only slightly below average rates of growth seen in recent years. For full time jobs, y/y growth at +1.7% is also modestly below recent averages, so it might be too soon to say this is the start of a jobs market correction.

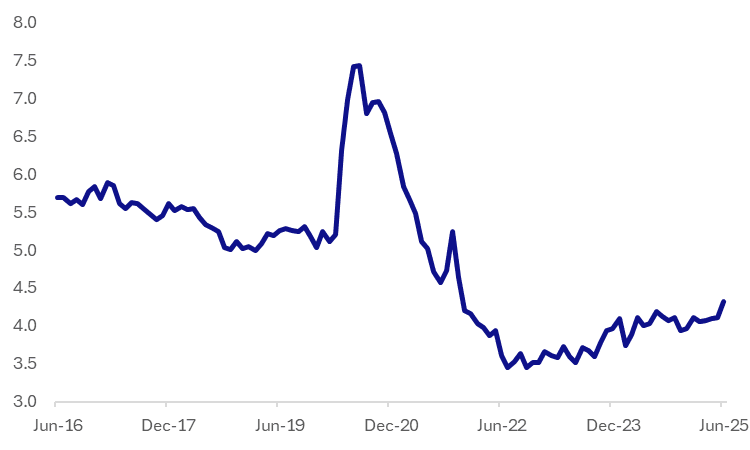

- Still the number of people unemployed rose by 34k, the largest rise since April of last year. This, combined with the slight tick up in the participation rate was enough to drive a rise in the unemployment rate to 4.3%, which was the highest outcome since Nov 2021 (see the second chart below). The unemployment rate to two decimal places was 4.32% versus 4.11% last month.

- The ABS noted: "‘This month we saw a decrease in full time hours worked, down 1.3 per cent, associated with a 0.4 per cent fall in full time employees,’ Mr Crick said."

Fig 1: Australia Employment Growth, Total & Full Time Jobs Y/Y

Source: ABS/MNI

Fig 2: Australian Unemployment Rates (%)

Source: ABS/MNI

BONDS: NZGBS: Modestly Richer, NZ-AU 10Y Diff Wider After AU Jobs

NZGBs closed mid-range, with benchmark yields flat to 2bps lower.

- Today’s supply was well received with cover ratios ranging from 2.83x (May-36) to 3.68x (May-30).

- The NZ-US 10-year yield differential was little changed, with the US 10-year 2bps cheaper in today’s Asia-Pac session. The NZ-AU 10-year differential was 4bps wider after a solid post-employment rally for ACGBs.

- June food prices rose 1.2%m/m, versus a 0.52% gain in May. This saw the y/y pace for food prices rise 4.6%, which was the strongest annual pace since late 2023. Stats NZ noted: "Higher prices for the grocery food group and the meat, poultry, and fish group contributed most to the annual increase in food prices, up 4.7 per cent and 6.4 per cent, respectively." Note, we get Q2 inflation next Monday.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed mostly slightly softer across meetings. 17bps of easing is priced for August, with a cumulative 33bps by November 2025.

- Tomorrow, the local calendar will be empty.

NEW ZEALAND: June Sees Higher Food/Utility Prices, Q2 CPI Out Next Monday

New Zealand June food prices rose 1.2%m/m, versus a 0.52% gain in May. This saw the y/y pace for food prices rise 4.6%, which was the strongest annual pace since late 2023. Stats NZ noted: "Higher prices for the grocery food group and the meat, poultry, and fish group contributed most to the annual increase in food prices, up 4.7 percent and 6.4 percent, respectively."

- Elsewhere, rent prices rose 0.1%, to be up 2.6%y/y, the slowest pace since 2011. Electricity prices were up 1.6%m/m, after the 2.3% gain in May. Y/Y for this segment is now +10.4%, Gas prices are up 16.4%y/y.

- Petrol and diesel prices continued to fall in m/m terms, albeit at a reduced pace compared to May declines. Both segments are still down comfortably in y/y terms (petrol -5.3%).

- Airfares were up m/m but didn't recoup all of the falls seen in May. Accommodation services fell 1.4% in y/y, but is still +5.2%y/y.

- The strength in food and utility prices is something the RBNZ was mindful of when it held policy rates steady last week. They expect this to bias headline inflations pressure in the near term.

- Note we get Q2 inflation next Monday.

FOREX: Asia FX Wrap - Is The Powell Sacking Rumour Enough To Turn The USD Lower?

The BBDXY has had a range of 1203.66 - 1206.99 in the Asia-Pac session, it is currently trading around 1206, +0.20%. What is clear from the price action is the market is very quick to sell USD’s again if given the excuse, is the mere threat of Powell being dismissed enough to turn the USD lower again. (Bloomberg) - 'The narrative around a long-term decline in the dollar has found fresh fuel from renewed concern about political interference in US monetary policy. The mere revival of discussions - however implausible legally - around firing Federal Reserve Chair Jerome Powell has reintroduced a key bearish catalyst for the dollar.'

- EUR/USD - Asian range 1.1614 - 1.1641, Asia is currently trading 1.1620. The pair is testing its first support around the 1.1600 area. The price still looks a little stretched in the short term and is vulnerable to any correction in the USD, first support around 1.1600 then more importantly the 1.1450 area.

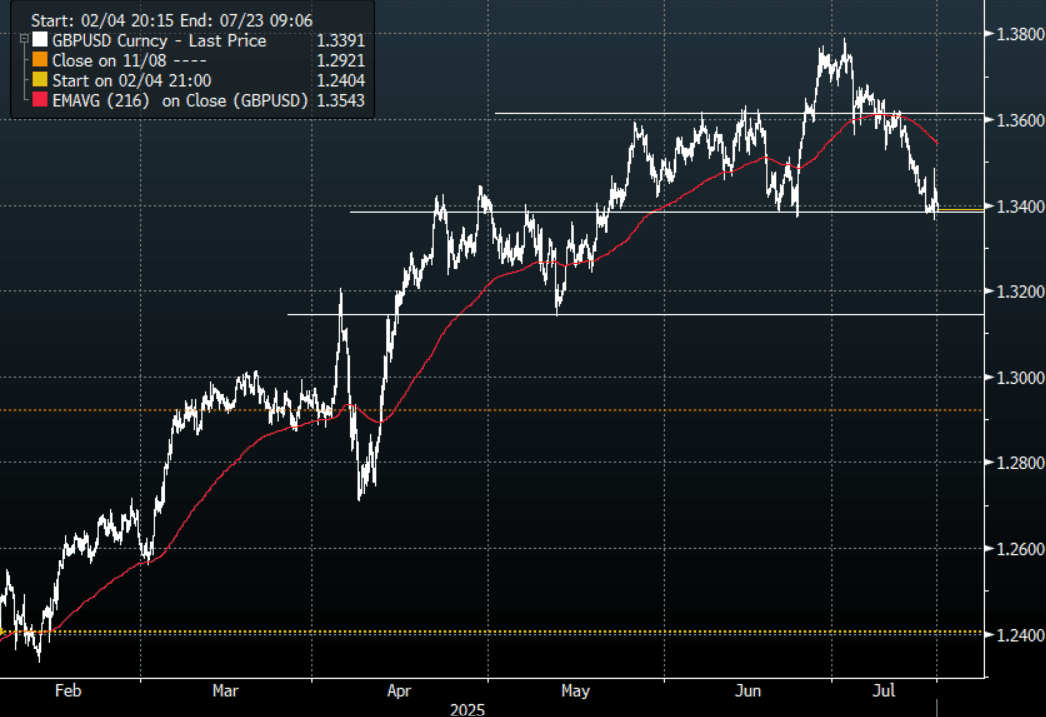

- GBP/USD - Asian range 1.3384 - 1.3430, Asia is currently dealing around 1.3390. Price has rejected the move higher and Bailey’s hint that bigger rate cuts are on their way if the job market deteriorates further will have all eyes on the data out today. The pair has moved very quickly to test important support around 1.3350/1.3400. We have seen some demand initially around this support but a sustained break below and a deeper pullback towards 1.3000/1.3200 could be on the cards. Bounces back towards 1.3500 should now see offers first up.

- USD/CNH - Asian range 7.1781 - 7.1845, the USD/CNY fix printed 7.1461, Asia is currently dealing around 7.1820. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.25%, Gold $3355, US 10-Year 4.47%, BBDXY 1207, Crude oil $65.67

- Data/Events : EZ CPI

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

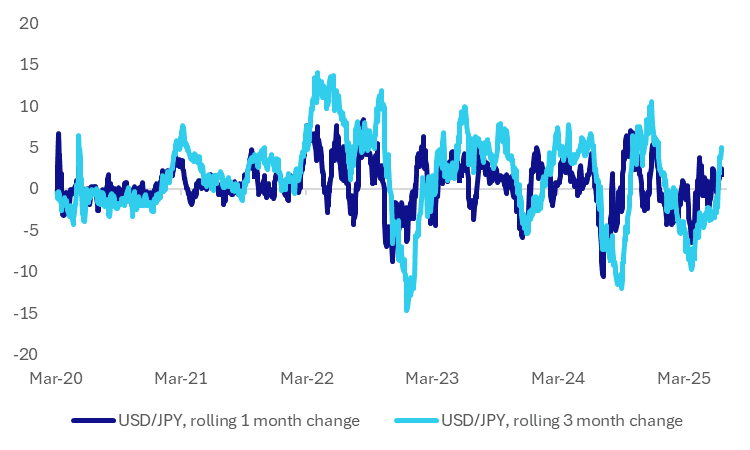

JPY: Verbal Rhetoric On FX Picks Up, USD/JPY 1 mth Change Still Modest

Earlier we saw some verbal jawboning on FX comments cross from Japan officials. See below. Aoki is the Deputy Chief Cabinet Secretary

Via BBG: "*AOKI: CONCERNED ABOUT MOVES IN FX MARKET INCL. SPECULATIVE ONES, *AOKI: KEY FOR FX RATE TO MOVE STABLY, REFLECT FUNDAMENTALS"

- This comes after the recent period of yen weakness. USD/JPY sits close to 148.45 in latest dealings. Recent highs rest at 149.18 (seen on Wednesday before Trump firing Powell headlines crossed, which were later denied). Earlier in July, lows in the pair came in just under 142.68.

- The chart below presents the rolling 1 month and 3 month rates of change for spot USD/JPY. We are below extreme readings for both metrics going back over the past few years. The 1 month rise is now a little over 2%, while the 3 month change is near +5%.

- Recent extremes in the 1 month rate of change was above 7% seen in 2024, but periods of beyond 5% tend not be sustained. For the 3 month rate of change, recent extremes rest close to +10%. Moves into the 10-15% region on this metric are quite rare.

- If we extrapolate USD/JPY moves to the end of this move where we assume USD/JPY has rise to around 152.00 that puts the rolling 1 month change above 5%, while the 3 month change would be at 7%.

- So we still have some distance to go to reach more extreme shifts in these metrics, but it will be something on the markets radar in light of the above comments.

Fig 1: USD/JPY Rolling 1mth, 3mth Rate Of Change

Source: Bloomberg Finance L.P./MNI

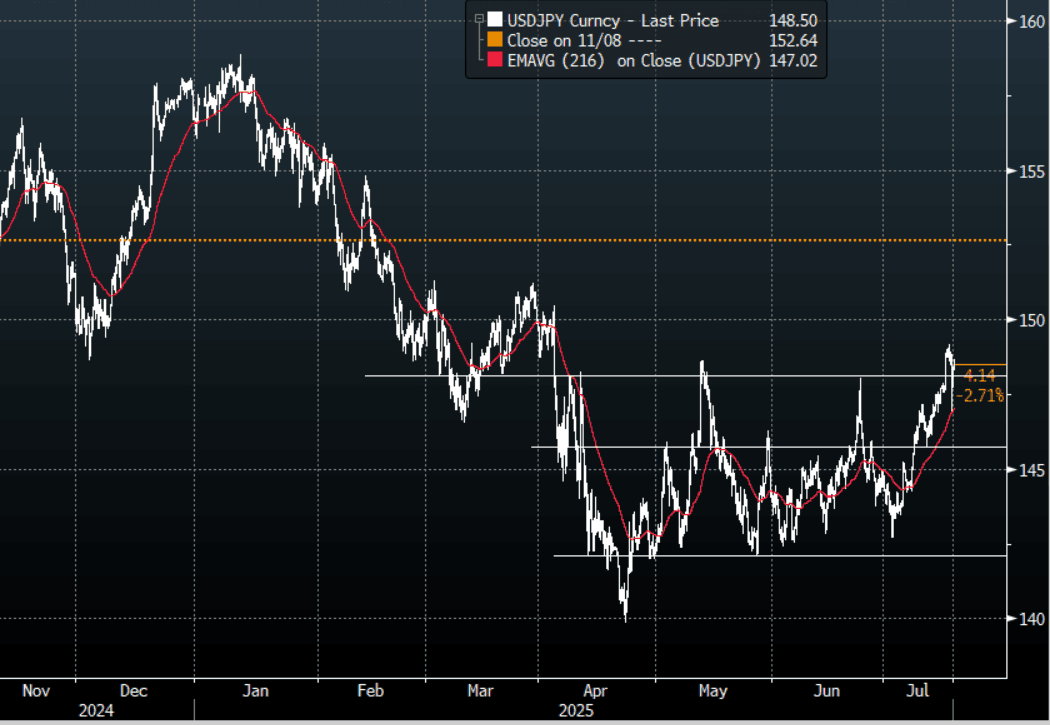

JPY: Asia Wrap - USD/JPY Finds Demand On The Dip

The Asia-Pac USD/JPY range has been 147.73 - 148.66, Asia is currently trading around 148.50, +0.45%. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. What is clear from the price action is the market is very quick to sell USD’s again if given the excuse, the last couple of weeks has been painful for the JPY longs but the market still strongly believes the USD will ultimately end lower and does not want to miss out. Decent demand was seen towards the 147.00 area overnight and would think unless there is confirmation of Powell being dismissed dips lower should be supported initially.

- (Bloomberg) - USD/JPY is seeing a short squeeze as algo systems react to headlines from Fed’s Williams which sound supportive of the US dollar. There was also likely dollar buying going into the Tokyo yen fixing as it was set at 148.51. “WILLIAMS: FACTORS SUPPORTING STRENGTH OF DOLLAR STILL IN PLACE.”

- JAPAN DATA Exports Fall Y/Y For Second Straight Month, Below Forecasts.

- Earlier we saw some verbal jawboning on FX comments from Japan officials. Aoki is the Deputy Chief Cabinet Secretary Via BBG: "AOKI: CONCERNED ABOUT MOVES IN FX MARKET INCL. SPECULATIVE ONES, KEY FOR FX RATE TO MOVE STABLY, REFLECT FUNDAMENTALS"

- Personally I don’t feel the BOJ would consider intervention again unless USD/JPY is back above 155.00 and looking to challenge 160.00 again.

- The USD/JPY market did not hold above its breakout very long, is the mere threat of Powell being dismissed enough to turn around the fortunes of USD/JPY ?

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.25b).Upcoming Close Strikes : 147.00($1.29b July 22), 145.50($1.29b July 21) - BBG.

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Testing Support Below 0.6500 On Poor Employment Data

The AUD/USD has had a range of 0.6473 - 0.6533 in the Asia- Pac session, it is currently trading around 0.6485, -0.67%. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. The price action was very clear though, if Powell is removed the USD will be swiftly sold. Australian unemployment climbed to a 4-Year high and this saw the AUD tumble across the board. The AUD/USD is attempting to break through its support just below 0.6500, one would think we would need the USD to catch a bid into the London session if this is to follow through. A break below here signals a deeper correction back towards the 0.6350 area.

- (Bloomberg) -- Australian unemployment unexpectedly climbed to a four-year high in June as hiring almost stalled, suggesting a loosening of the labor market and bolstering the case for the Reserve Bank to reduce interest rates next month.

- (Bloomberg) -- The RBA will likely cut rates by a quarter point at their August, November and February meetings, according to Nomura Singapore Ltd. “With cracks now appearing — particularly the drop in full-time workers — this opens the door wider for RBA cuts.” “The fall in AUD/USD makes sense as a solid job market has been a key reason why the RBA has been patient thus far in cutting rates.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6540(AUD556m), 0.6500(AUD473m). Upcoming Close Strikes : 0.6480(AUD886m July18), 0.6500(AUD739m July 21), 0.6600(AUD725m July 21)

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

- AUD/JPY - Today's range 96.11 - 96.77, it is trading currently around 96.35, +0.20%. The pair collapsed lower with risk but has not really recovered its losses as well as the broader market. Demand was seen again this morning toward the initial breakout area of 95.50/96.00 and this will need to hold to build a platform from which to probe higher again. A Deeper correction in risk though would clearly provide strong headwinds to further gains.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

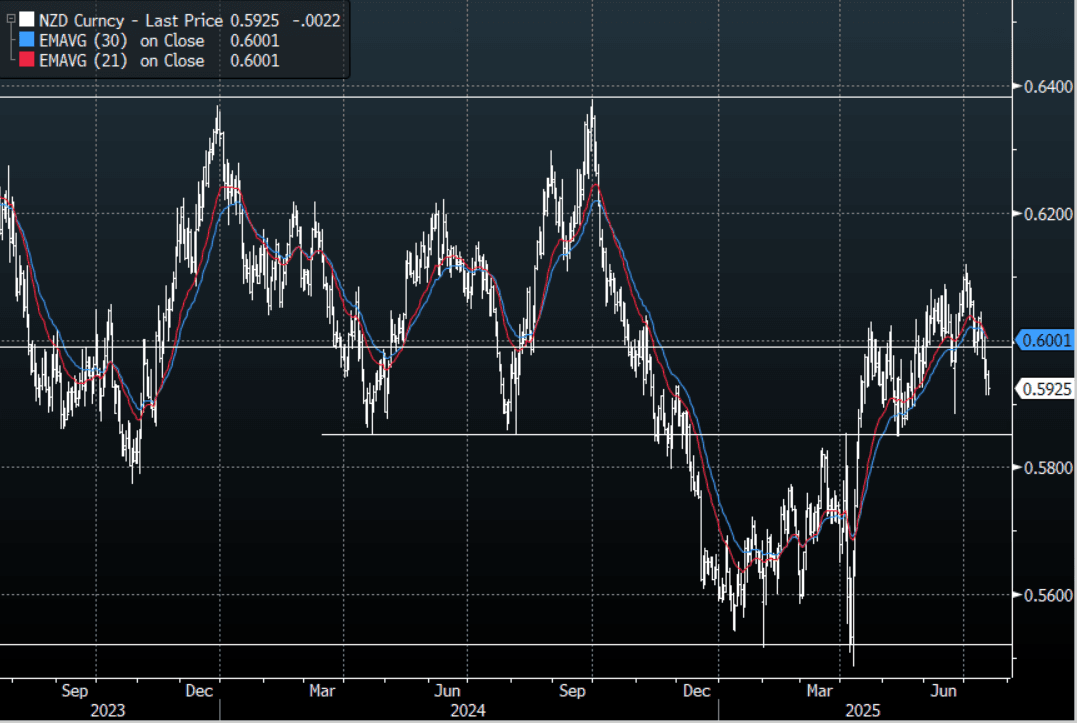

NZD: Asia Wrap - NZD/USD Trades Heavy Rallies Should Be Capped For Now

The NZD/USD had a range of 0.5912 - 0.5953 in the Asia-Pac session, going into the London open trading around 0.5925, -0.40%. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. The price action was very clear though, if Powell is removed the USD will be swiftly sold. NZD/USD has broken below its recent support just under 0.6000 and the price action now suggests we could have a look back towards the important 0.5850 support area. Look for supply now on bounces back towards 0.6000 to cap initially. Any hint of Powell being removed though would clearly see the NZD surge higher once more.

- NEW ZEALAND June Sees Higher Food/Utility Prices, Q2 CPI Out Next Monday

- "NZ Westpac Sees Q2 Inflation Up 0.6%q/q, 2.8% y/y : The local bank weighs in on expectations for next week's Q2 CPI outcome. It expects y/y at 2.8%, which is above RBNZ projections." - BBG

- “ANZ Bank raises Q2 inflation pick to 2.9% from 2.8% previously. “The RBNZ will find the details of the CPI a little more uncomfortable than they hoped back in May.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5932(NZD317m July 18), 0.6000(NZD300m July 22). - BBG

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654

- AUD/NZD range for the session has been 1.0939 - 1.0981, currently trading 1.0950. The cross has moved lower in response to the AU Employment data. Dips back to 1.0850/1.0900 should still find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Most Regional Bourses Higher, Thailand Up Over 2%

Regional Asia Pac equity indices are mostly higher in the first part of Thursday trade. Firmer trends are evident in South East Asia (SEA) at the moment, with Thailand the standout, up close to 2.4% at this stage. US equity futures are down modestly, while EU futures are faring better. US cash trade on Wednesday saw sentiment whipped around by headlines/stories on Trump firing Fed Chair Powell (which was later denied, but is still a possibility).

- Hong Kong markets sit up a touch at the break, the HSI near 24535, still close to recent highs. The CSI 300 is up 0.31%, near 4020, so within recent ranges.

- Japan markets are modestly higher at this stage, the Topix +0.50%. USD/JPY is recovering from Wednesday's dip, while the authorities issued fresh verbal jawboning on FX markets. June trade data showed export growth stayed negative as shipments to the US fell.

- The Kospi and Taiex are little changed so far. TSMC earnings will be in focus for Taiwan and the broader AI/tech space.

- In SEA, Thailand stocks are up strongly, the SET around 1185, which is fresh highs back to May. A move above 1200 could be targeted. THB is outperforming in the FX space as well. Direct catalysts don't appear apparent. Less offshore selling pressures have been evident in Thailand markets so far in July, a potential positive.

- Indonesian stocks are up as well, last +1.20%, putting the JCI at fresh highs since January of this year. Australia's market is up around 0.65%, with earlier jobs data firmed RBA easing odds for August.

- The Philippines benchmark is down 0.65%, bucking positive trends seen elsewhere in SEA.

ASIA STOCKS: Taiwan Inflows Remain The Standout (+2bn In The Past Week)

Yesterday, continued positive inflow momentum to Taiwan remained the standout in the region. The past 5 trading days has seen just over $2bn in net offshore inflows for the country. Optimism around TSMC's quarterly earnings may be spurring continued inflow momentum. Earlier the company reported a better than expected 39% rise June quarter revenue. South Korean inflows remained positive, albeit just, with the local Kospi index continuing to struggle above the 3200 level. In early dealings today the index is off around 1%.

- Elsewhere, Indonesia's trade deal with the US, didn't provide a positive impetus to offshore inflow momentum, with recent negative trends continuing. The BI also cut rates yesterday. The local equity index is close in on recent highs above 7200.

- Thailand saw positive inflow momentum, driving outperformance against other SEA economies over the past week.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 17 | 1109 | -8120 |

| Taiwan (USDmn) | 510 | 2043 | -885 |

| India (USDmn)* | -20 | -459 | -8440 |

| Indonesia (USDmn) | -67 | -153 | -3659 |

| Thailand (USDmn) | 68 | 106 | -2327 |

| Malaysia (USDmn) | -41 | -96 | -2854 |

| Philippines (USDmn) | -61 | -65 | -617 |

| Total (USDmn) | 406 | 2487 | -26902 |

| * Data Up To July 15 |

Source: Bloomberg Finance L.P./MNI

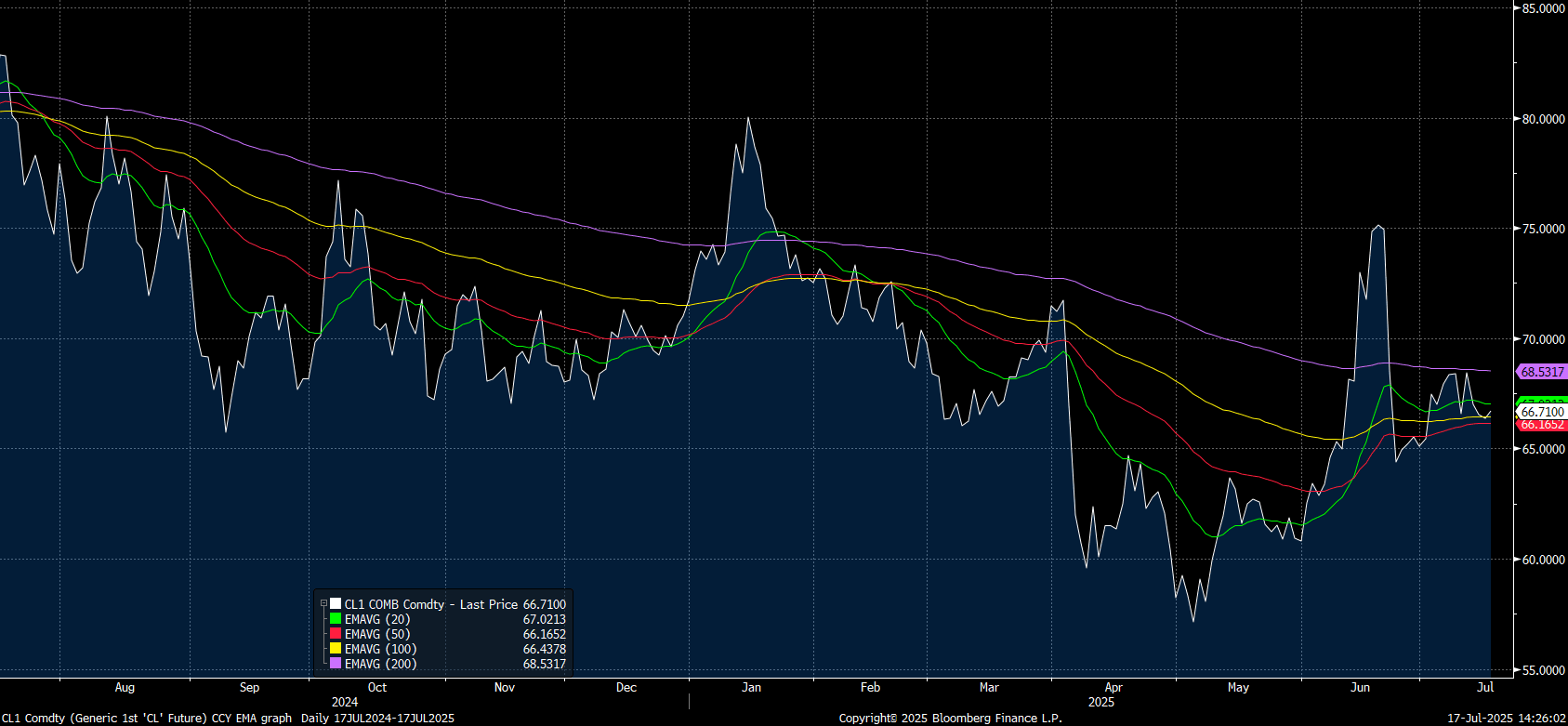

Oil Snaps Three Down Days with Modest Gains

- Oil broke three days of losses to eke out some minor gains in the Asia trading day today.

- WTI is up +34c to US$66.72 bbl. Having traded briefly below the 100-day EMA of $66.43, it has moved back above. The 20-day EMA is above at $67.02

Source: Bloomberg Finance L.P./MNI

- Brent is up also to snap three down days, rising 25c to US$68.77 bbl.

- Oils fortunes continue to ebb and flow between OPEC+ supply headlines and tariff headlines. President Donald Trump said he would send letters to more than 150 countries notifying them of tariff rates, and that the levies imposed could be 10% or 15%..

- Crude oil put spreads and other bearish strategies were active as weekly EIA oil inventory data showed signs of a softening physical market.

- Iranian authorities seized an unidentified foreign oil tanker on charges of smuggling 2 million liters of fuel in the Sea of Oman, semi-official Mehr agency reports.

- Multiple oil fields in the Kurdistan region in northern Iraq were attacked by drones on Wednesday, adding to a spate of hits on energy installations in the area this week. A majority of oil companies in the region suspended production after the attacks, resulting in the loss of nearly 200,000 barrels of oil production, according to an official.

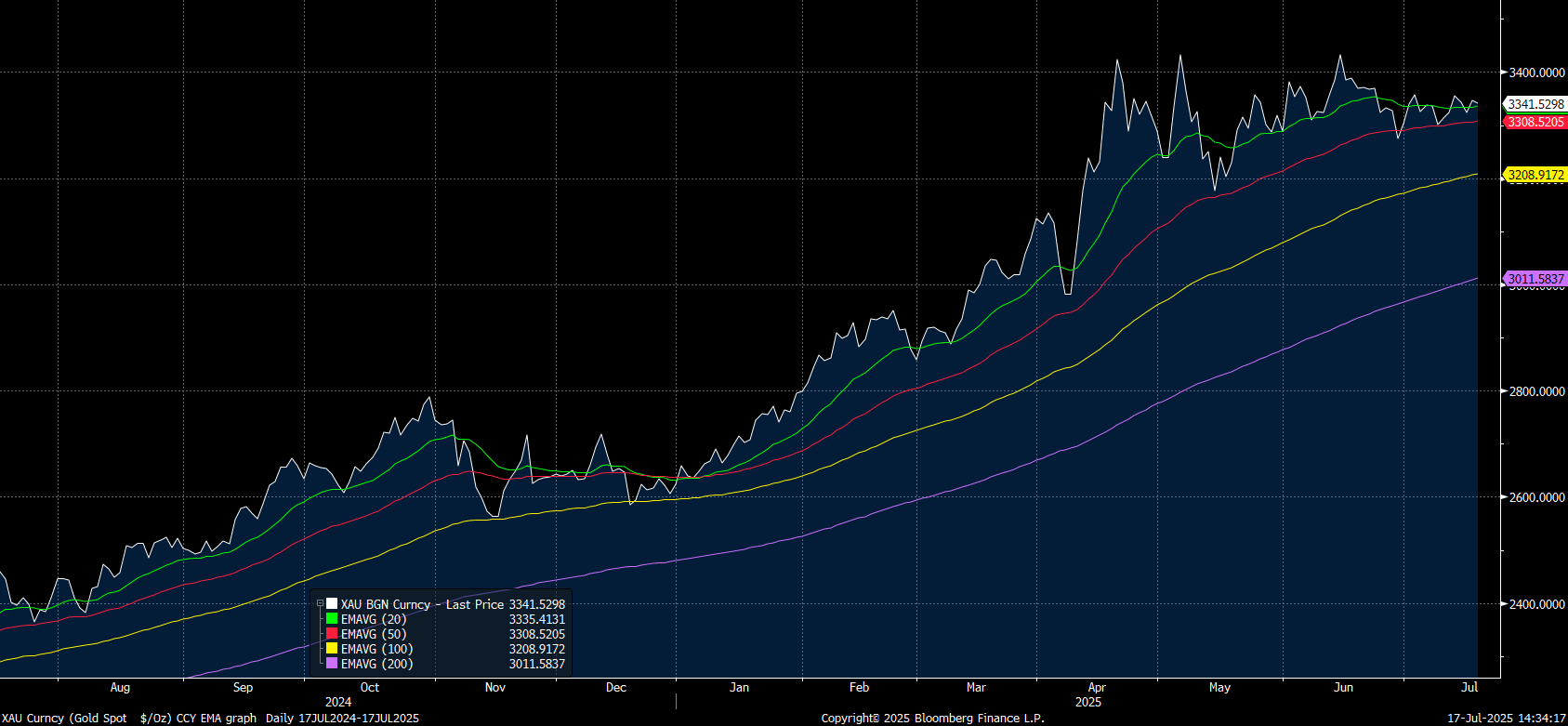

Gold Tests Key Technical Level

- Gold softened marginally today and if that continues through the European trading day, a key technical level will be tested.

- Gold is re-acting to the headlines out of the US as the President continues his attack on the Fed Chairman Powell.

- Gold is responsive to interest rate cuts as it does not earn or pay interest and lower interest rates flow through to lower costs of funding gold purchases. President Trump's main issue with Powell is he wants lower rates.

- Gold is lower today in the Asia trading day by -0.16% to be US$3,341.65 and sits just above the 20-day EMA of $3,335.45. A breach below sees the next technical level at $3,308.54 for the 50-day EMA.

Source: Bloomberg Finance L.P./MNI

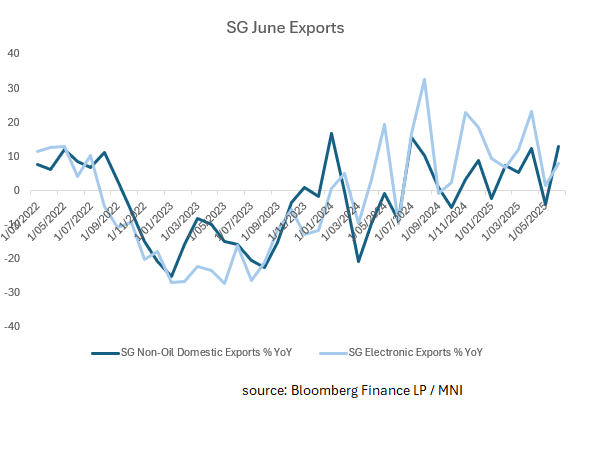

SINGAPORE: Non-Oil Domestic Exports Up +13% YoY vs est. +5.0% YoY

- The surge in June exports surprised economists jumping +13.0% YoY.

- Forecasts were expecting a rebound of +5.0% following May's contraction of the revised -3.9% YoY.

- This was the strongest result since July 2024 in what is typically a volatile release.

- As one of the most open economies in Asia, Singapore is exposed to the volatilities of the region and often market watchers follow Singapore data releases closely, using it as guide for the broader region.

- Electronic exports were up +8.0% after rising just +1.6% in May.

- Electronic exports had surged by 23% in April in what is likely an attempt to ship goods ahead of the implementation of tariffs.

ASIA FX: Firmer CNY Fixing Bias Helps CNH, KRW & TWD Down A Touch

In North East Asia markets, the bias has been for firmer USD levels, although CNH has outperformed. KRW and TWD have lost modest ground, while USD/HKD remains near the top end of the peg band, just under 7.8500 in latest dealings.

- USD/CNH hasn't drifted too far from the low 7.1800 region, which is outperforming firmer USD levels against the majors and elsewhere in Asia Pac. Helping sentiment has been the firmer CNY fixing bias, which rose today to fresh highs since Nov last year. This is despite the USD index being comfortably above recent lows.

- Spot USD/KRW has drifted a little higher, last near 1392. We remain sub overnight highs in the pair, which were just under 1395. Local equities have been volatile, struggling to hold gains above 3200. We were last little changed for the session.

- USD/TWD spot is holding a touch higher, last close to 29.42, with earlier highs in the pair at 29.45. Local equities in Taiwan are also little changed so far today.

ASIA FX: THB & MYR Outperform, IDR & PHP Weaker

In South East Asia FX markets, trends have been mixed, with aggregate moves not large at this stage. PHP and IDR has lost further ground, while THB and MYR have modestly outperformed. USD/SGD is up a touch despite a decent export beat.

- USD/THB is back close to 32.46, down around 0.25% versus end Wednesday levels. Gold prices are down slightly, but remain within striking distance of $3400. The authorities are aiming to break the firm link between gold and THB. Local equities have surged, +2.85% at this stage, another potential positive for the local FX. USD/THB is still above recent lows near 32.30 though.

- USD/MYR is relatively steady, holding near 4.2450 in latest dealings. USD/SGD is up a touch to 1.2850, in line with the majors losing ground versus the USD. Highs yesterday were close to 1.2875. Earlier we had stronger than expected export data (+13.0%y/y, versus +5.0% forecast).

- USD/IDR is up through 16320 in latest dealings, fresh highs since late June. We haven't seen a return of portfolio inflows, at this stage, in either the equity or debt space, despite the trade deal announced with the US.

- USD/PHP also continues to rise, last in the 57.15/20 region, which pits us through the 200-day EMA resistance point.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0900/1100 | *** | HICP (f) | |

| 17/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1315/0915 | Fed Governor Adriana Kugler | ||

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/07/2025 | 1645/1245 | San Francisco Fed's Mary Daly | ||

| 17/07/2025 | 1730/1330 | Fed Governor Lisa Cook | ||

| 17/07/2025 | 2000/1600 | ** | TICS | |

| 17/07/2025 | 2230/1830 | Fed Governor Christopher Waller | ||

| 18/07/2025 | 2330/0830 | *** | CPI | |

| 18/07/2025 | 0600/0800 | ** | PPI | |

| 18/07/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/07/2025 | 0900/1100 | ** | Construction Production | |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts |