JPY: Verbal Rhetoric On FX Picks Up, USD/JPY 1 mth Change Still Modest

Earlier we saw some verbal jawboning on FX comments cross from Japan officials. See below. Aoki is the Deputy Chief Cabinet Secretary

Via BBG: "*AOKI: CONCERNED ABOUT MOVES IN FX MARKET INCL. SPECULATIVE ONES, *AOKI: KEY FOR FX RATE TO MOVE STABLY, REFLECT FUNDAMENTALS"

- This comes after the recent period of yen weakness. USD/JPY sits close to 148.45 in latest dealings. Recent highs rest at 149.18 (seen on Wednesday before Trump firing Powell headlines crossed, which were later denied). Earlier in July, lows in the pair came in just under 142.68.

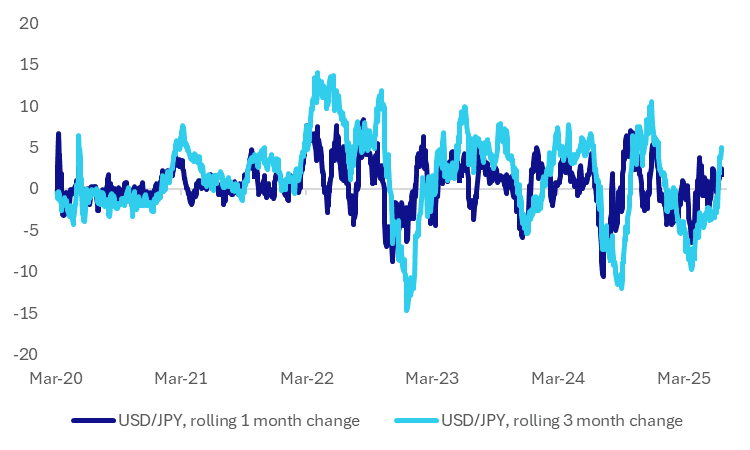

- The chart below presents the rolling 1 month and 3 month rates of change for spot USD/JPY. We are below extreme readings for both metrics going back over the past few years. The 1 month rise is now a little over 2%, while the 3 month change is near +5%.

- Recent extremes in the 1 month rate of change was above 7% seen in 2024, but periods of beyond 5% tend not be sustained. For the 3 month rate of change, recent extremes rest close to +10%. Moves into the 10-15% region on this metric are quite rare.

- If we extrapolate USD/JPY moves to the end of this move where we assume USD/JPY has rise to around 152.00 that puts the rolling 1 month change above 5%, while the 3 month change would be at 7%.

- So we still have some distance to go to reach more extreme shifts in these metrics, but it will be something on the markets radar in light of the above comments.

Fig 1: USD/JPY Rolling 1mth, 3mth Rate Of Change

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - JPY Longs Conviction Being Tested

This morning's post by President Trump that everyone should evacuate Tehran immediately has seen stocks open soft in our session, if something significant is not seen the danger is this move will also just be reversed. ESU5 -0.40%, NQU5 -0.50%. You would normally think the JPY crosses would be moving lower on this but for the moment the JPY longs conviction is being challenged in the crosses. The BOJ coming up could also add some volatility.

- EUR/JPY - Overnight range 166.37 - 167.46, Asia is trading around 167.50. The move higher is beginning to gain momentum, dips look likely to remain supported. First support seen back towards 165/66, focus now turns back to 170.00.

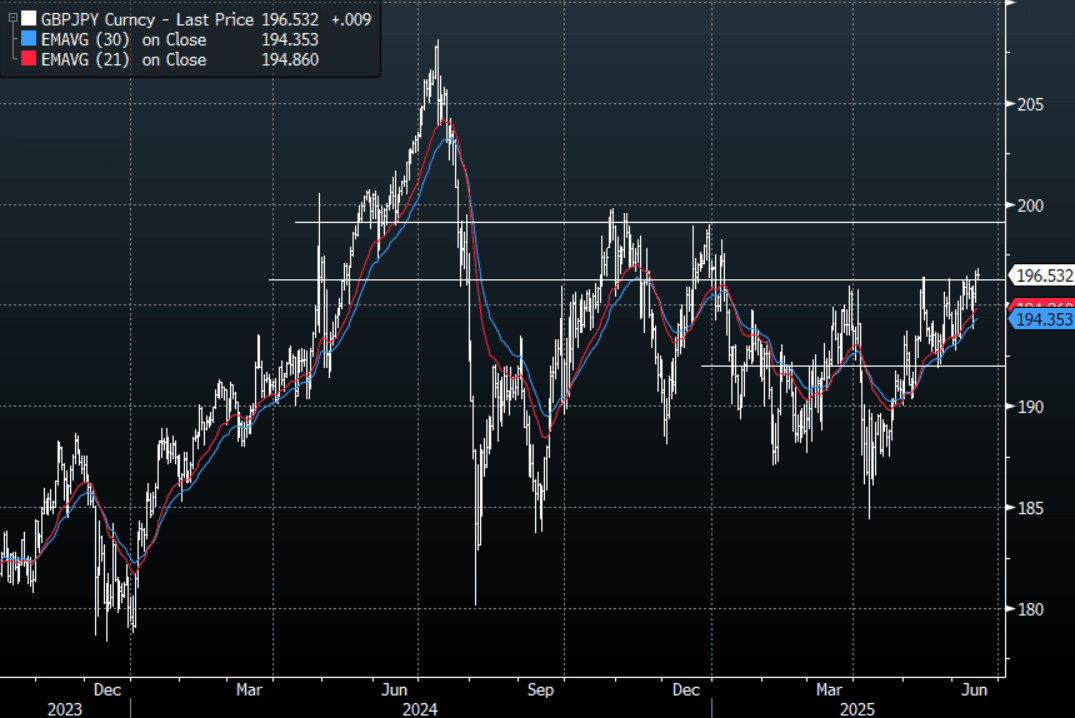

- GBP/JPY - Overnight range 195.43 - 196.69, Asia trades around 196.70. GBP/JPY is breaking its multiple tops around 196.50, a sustained move through could see the move gain momentum and focus will then turn towards the 200.00 area.

- NZD/JPY - Overnight range 86.75 - 87.78, Asia is currently dealing 87.85. NZD/JPY is looking to break back above 88.00, a sustained break above here and the market would target the 90.00 area.

- CNH/JPY - Overnight range 20.0082 - 20.1675, Asia is currently trading around 20.1850. CNY/JPY trades sideways for now in a 19.70 - 20.30 range.

Fig 1 : CNH/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Little Changed Ahead Of BoJ Decision, Jobs Data On Thurs

ACGBs (YM +1.0 & XM +0.5) are little changed on a data-light Sydney session.

- May's jobs data is on Thursday. Bloomberg consensus sees a 20k rise in new jobs, in line with the 3-month average, with the unemployment and participation rates stable at 4.1% and 67.1% respectively.

- Cash US tsys are 2-3bps richer in today's Asia-Pac session, partially reversing yesterday's cheapening.

- MNI - Former Fed Board of Governors economist Joseph Gagnon expects the FOMC to be on hold all year as inflation rises more than unemployment.

- The BoJ Policy decision is due shortly, with the market expecting an unchanged decision. The key area of interest will be Governor Kazuo Ueda's post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes. The second area of market focus is on the BoJ's JGB purchase program. Market expectations suggest a slower pace of reductions during fiscal year 2026.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at -19bps.

- The bills strip is little changed, with pricing -1 to +1.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in July is given an 86% probability, with a cumulative 80bps of easing priced by year-end.

JGBS: Modestly Cheaper Ahead Of BOJ Policy Decision

At the Tokyo lunch break, JGB futures are slightly stronger, +3 compared to the settlement levels, after paring overnight gains.

- This comes despite cash US tsys being 2-3bps richer in today’s Asia-Pac session, partially reversing yesterday’s cheapening.

- We are getting closer to the BoJ policy announcement release window. As usual, the general rule of thumb is that the later the policy announcement time, the greater the likelihood that a potential policy change is being debated.

- The BoJ is expected to keep its policy rate unchanged at 0.50% today. The key area of interest will be Governor Kazuo Ueda's post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes.

- The second area of market focus is on the BoJ's JGB purchase program. Market expectations suggest a slower pace of reductions during fiscal year 2026. (See MNI BoJ Preview here)

- Cash JGBs are flat to 2bps cheaper across benchmarks, with the 7-10-year zone underperforming. The benchmark 10-year yield is 1.5bps higher at 1.453% versus the cycle high of 1.596%.

- Swap rates are flat to 2bps higher, with a mild steepening bias. Swap spreads are mixed.