MNI EUROPEAN MARKETS ANALYSIS: Precious Metals Pare Rally

- November CPI inflation data moved in the right direction for the RBA to prolong its pause but remain cautious as underlying 3-month momentum remains elevated. RBA-dated OIS is slightly firmer versus pre-CPI levels. The A$ has outperformed, but is away from best levels.

- Oil has faced further downward pressure today after US data showed large product inventory builds and President Trump announced Venezuela will ship “between 30 and 50 MILLION barrels of High Quality Sanctioned Oil” to the US. After rallying on Tuesday as geopolitical risks drove safe haven flows, gold & silver are lower in Wednesday’s APAC session.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.

MARKETS

US TSYS: Yields Grind Lower on Mixed Day for Equities

US treasury futures remain up in Wednesday trade across all maturities. The US 10-Yr is up +03+ at 112-13+. The rally for TYH6 takes it near to the 100-day EMA of 112-14+ which it traded below at the start of trading this week.

Cash is seeing lower yields with longer bonds outperforming ahead of a big data release tonight.

- The 2-yr is flat at 3.465%

- The 5-yr is at 3.71% - down -0.5bps

- The 10-yr is at 4.165% - down 1bps

- The 30-yr is at 4.854% - down 1.2bps.

Tonight markets will focus on the ADP Employment change, ISM Services and JOLT Job openings, Factor Orders and Durable Goods orders. For the ADP, forecasts are for +50k in December, from -32k prior. Other key data out will be the ISM Services Index which is forecast to moderate to 52.2 from 52.6 in November. JOLT job openings is forecast at 7648k for December, from 7670 in November. Factory and Durable goods orders are both forecast to contract.

Tonight sees a US$69bn 17-week bill auction. Last 17-week auction had a bid to cover of 3.11x

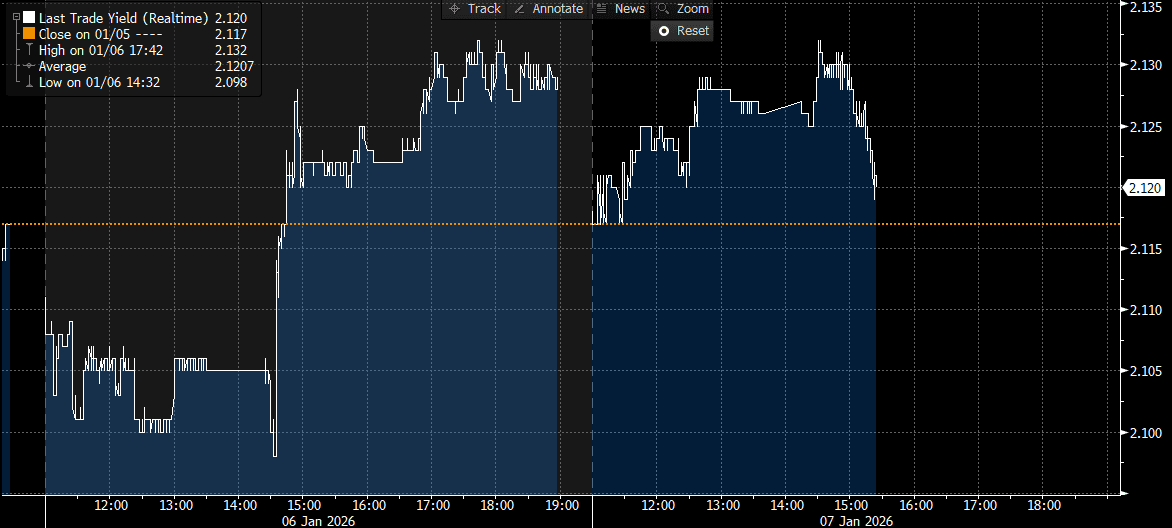

JGBS: Twist-Steepener Ahead Of Tomorrow's 30Y Supply

JGB futures are stronger, +16 compared to settlement levels, but off session bests.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- (Bloomberg) “JGB traders continue to be aggressive sellers of bonds in the mid-section of the curve when the BOJ comes calling at Rinban operations. The selling ratio rose today to 3.11 in the three-to-five year sector, up from 2.37 at the previous round.”

- Nevertheless, the cash JGB curve has twist-steepened across benchmarks, with yields 1.3–1.7bps lower in the 3–5-year sector and around 2.5bps higher at the 40-year point, ahead of tomorrow’s long-end supply.

- The benchmark 10-year yield is 0.9bp lower at 2.120% versus the cycle high of 2.134% (see chart).

- The 10-year JGB auction yesterday delivered weakish results, with the low price failing to meet expectations at 100.00, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.3037x from 3.5913x.

- Swap rates are 1bp lower to 1bp higher, with a steeper curve.

- Tomorrow, the local calendar will see Cash Earnings, Tokyo Avg Office Vacancies, Consumer Confidence and Weekly International Investment Flows alongside 30-year supply.

Source: Bloomberg Finance LP

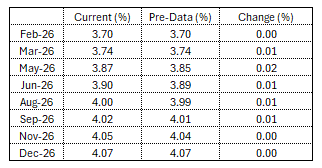

AUSSIE BONDS: Slightly Richer Post-CPI, Mixed On The Day

ACGBs (YM -1.0 & XM +2.0) are 2-3bps stronger versus pre-CPI levels, but well off post-date highs.

- November trimmed mean CPI inflation moderated 0.1pp to 3.2% y/y in line with consensus, while headline fell more than expected at 3.4% after 3.8%. The complete monthly series is new with little track record and so the RBA will focus on the quarterly data for now with Q4 printing on 28 January.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- Cash ACGBs are flat to 2bps richer with the AU-US 10-year yield differential at +59bps.

- The bills strip is -2 to -4 across contracts.

- RBA-dated OIS is slightly firmer versus pre-CPI levels. The pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 41% for February to 121% by June and 189% by December 2026.

- TCV A$ Nov 2037 Benchmark Bond Tap, 10Y EFP+88-90bp Area

- Tomorrow, the local calendar sees Trade balance data for November.

Figure 1: RBA-Dated OIS – Current

Source: Bloomberg Finance LP / MNI

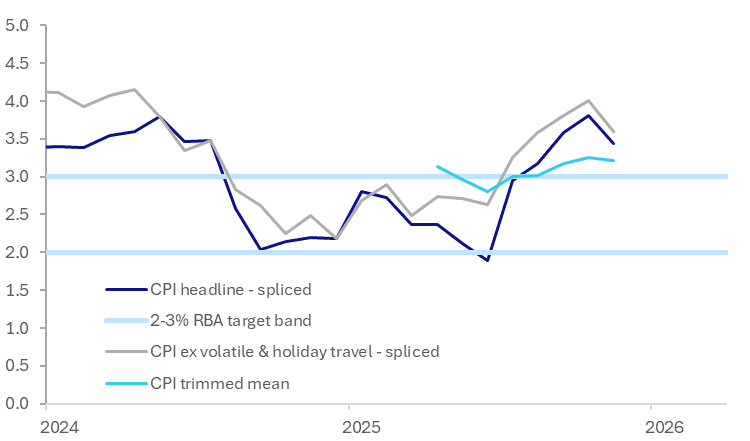

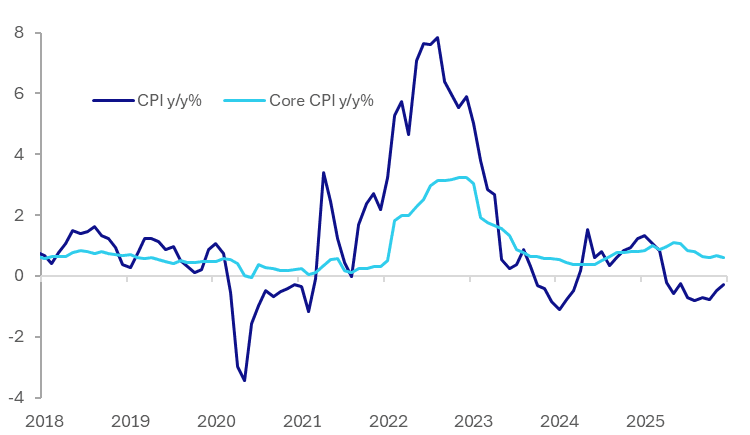

AUSTRALIA DATA: November Inflation Moderates, Q4 CPI Key February RBA Input

November CPI inflation data moved in the right direction for the RBA to prolong its pause but remain cautious as underlying 3-month momentum remains elevated. As this data is only new with little track record, the RBA will be looking to the Q4 data due on 28 January but November is a start in achieving its forecast of a return of trimmed mean to the band by end 2026.

- November trimmed mean rose 0.3% m/m sa and moderated to 3.2% y/y from 3.3% but the Q4 average to date at 3.2% is above Q3’s 3.1% average and Q2’s 3.0%. The quarterly Q3 release was 3.0%. CPI ex volatile items & holiday travel eased 0.4pp to 3.6% y/y.

- The new trimmed mean CPI appears less volatile than the incomplete series but printed 0.7pp higher at 2.8% y/y in June 2025, which was the recent trough. Q2 was at 2.7% y/y overall. Ex volatile items & holiday travel has a better fit with the old monthly data.

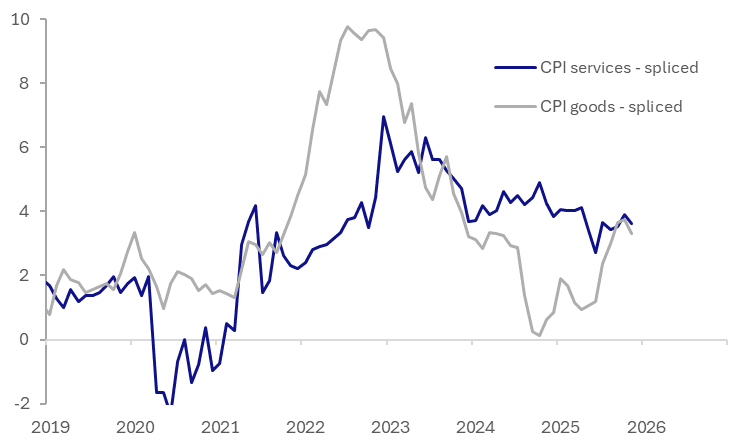

Australia CPI y/y%

Source: MNI - Market News/ABS

- The RBA is focused on domestically-driven services prices, as they have been sticky here and overseas. November services moderated to 3.6% y/y from 3.9% with underlying market services at 2.9% after 3.2%. The Q4 average of the latter is 3.0% after Q3’s 2.9% (Q3 average 2.84%).

- Good prices moderated to 3.3% from 3.8% with core goods at 2.6% after 2.8%. The ABS notes that the new series has more information on “temporary effects” and it observed Black Friday discounts in 2025 were “not a major contributor to the change in annual CPI inflation” in November.

- Headline continues to be impacted by government electricity rebates which drove a moderation to 3.4% y/y from 3.8% and rose 0.2% m/m sa. Electricity inflation was up 19.7% y/y down from 37.1% and excluding rebates electricity rose 4.6% y/y after 5.0%.

Australia CPI goods vs services y/y%

Source: MNI - Market News/ABS

*The new monthly CPI series is spliced onto the old CPI given the close fit.

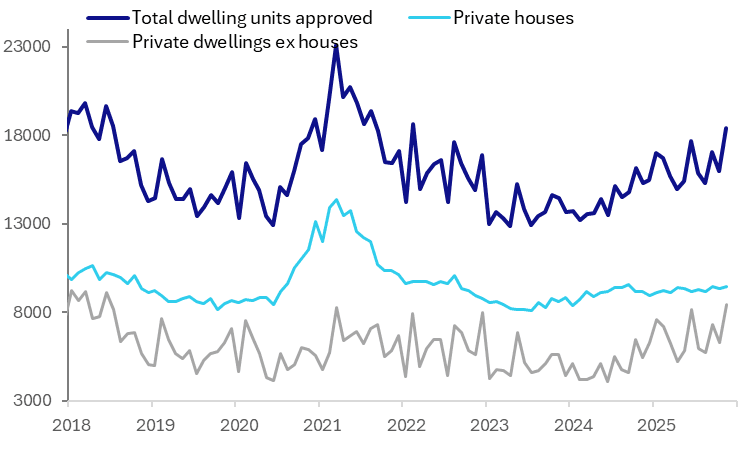

AUSTRALIA DATA: Multi-Dwellings Jump But House Approvals Remain Soft

The number of building approvals in November jumped 15.2% m/m after falling 6.1% m/m driven by the volatile multi-dwelling component. Private houses rose 1.3% m/m after falling 1.3% in October but were still up only 3.2% y/y. They appear to be recovering from the Q2/Q3 2025 dip. Momentum is picking up across both houses and apartments but the former is still soft.

- Strong demand and supply shortages have driven home prices higher. Approvals have struggled to improve as needed. A gradual uptrend in the total has been due to the non-house component but it remains 20% below the 2021 peak.

- Queensland and Victoria drove the jump in multi-dwelling approvals, which were their highest since June 2018 and up 55.3% y/y.

- The level of house approvals has been moving sideways since Q3 2024. The November rise was due to NSW and Queensland while they fell in SA.

Australia number of dwellings approved

Source: MNI - Market News/ABS

BONDS: NZGBS: Bull-Flattener But Swap Curve Remains At Highs

NZGBs closed showing a bull-flattening, with benchmark yields flat to 2bps.

- NZ-US and NZ-AU 10-year yield closed unchanged at +33bps and -28bps.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- NZ swap rates are flat to 3bps, with a flatter curve. Nevertheless, the 2s10s curve remains near cycle highs, the steepest since 2021.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

- The local data calendar is very light this week. Next week we get Nov filled jobs, along with food prices as well.

Bloomberg Finance LP

FOREX: A$ Gains The Standout, AUD/NZD At Fresh Cycle Highs, Steady Elsewhere

Outside of AUD gains, the price action in the G10 has been very muted so far today. The USD BBDXY index sits little changed near 1205.10 in latest dealings. The A$ sits up 0.35% to 0.6760/65, fresh highs back to 2024. We saw a brief dip to 0.6717 post a slightly softer Nov CPI read, but this was well supported. We are just above the Oct 11 2024 high of 0.6759, with the 0.6800 region now likely to come into focus. AU rates, particularly at the front end, were also supported from a yield stand point. RBA tightening expectations for 2026 sit slightly firmer versus pre CPI levels. Outside of rate expectations, the metals commodity backdrop is also aiding the AUD, with iron ore gains notable today.

- Shifts elsewhere in the G10 space are less than 0.1% at this stage. NZD/USD is little changed, last 0.5780/85, while USD/JPY is just under 156.60. EUR/USD is up a touch but still under 1.1700 at this stage.

- The AUD/NZD cross is trending towards 1.1700, fresh highs back to 2013. AUD/JPY is near 105.90, fresh highs back to mid 2024.

- We are seeing softer gold and silver trends so far today, but the BBG metals spot sub index is up 16% since late Nov lows. Iron ore is above $108.50/ton per the active SGX contract.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.

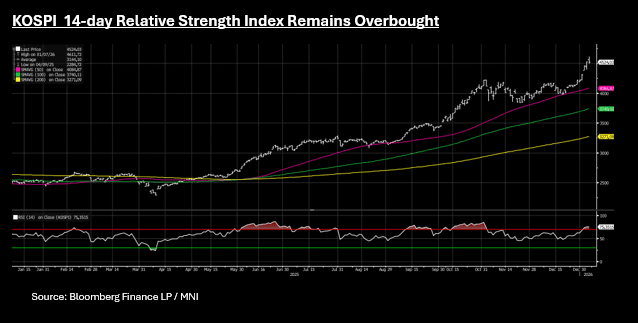

ASIA STOCKS: Mixed Day for Stocks, KOSPI Remains Overbought on RSI

A mixed day across Asia with profit taking driving key markets as they back away from near term highs. A mixed day for key AI / Tech stocks with Taiwan's TSMC - 1.7%, Korea's AI /Tech names have had a strong rally with Samsung Electronics +1.6%, +3.3%, Whilst Japan's Softbank fell -1.5%. The weakness in oil has had a limited impacted with some energy linked companies like Petronas in Malaysia up 1% today. There is growing recognition from markets of the stretched valuations for the tech sector, a risk that will continue in the background for now whilst the euphoria continues.

- The NIKKEI has had its first fall of the year, down -1.2% today whilst remaining up over 3% in the first three trading days, reaching a new high of 52,518 yesterday.

- The KOSPI is flat today despite the bounce back from the AI Tech names despite growing concerns over their valuations. The KOSPI maintains its position of overbought on the 14-day relative strength index, likely feeding into the the lacklustre performance today.

- China's bourses are mixed today with the Hang Seng following the lead from Japan and Korea with falls of -1.2%, dragging the CSI 300 down -0.22% with it. Onshore bourses have fared better with Shanghai up +0.15% and Shenzhen +0.21%

- SE Asia's major bourses were stable with SE Thai and FTSE Malay flat and the JCI in Indonesia up by a modest +0.14%

- India's NIFTY 50 continues to moderate down -.20% at early Wednesday for its third day of falls. Having reached new highs Friday of 26,328 it has fallen -0.60% in subsequent trading days.

CHINA STOCKS: Tech/Govt Initiatives In Focus, Attractive Valuations Help Gains

- Artificial Intelligence (AI): The AI sector, particularly AI chips, has been a primary driver of the recent market rally, benefiting from investor optimism and policy support. Though the AI / tech sector has somewhat lagged behind that of Korean and Japanese names, an opportunity some asset allocators are focusing on

- Domestic Semiconductor Production: A central pillar of Beijing's push for tech self-reliance, with directive-driven demand for Chinese-made AI chips in state data centers.

- New Energy Technologies: This sector is expected to benefit from continued government policy support and the country's pivot toward innovation-led growth.

- Innovative Drugs: The innovative pharmaceuticals industry is another area identified for potential growth within the new market phase.

CHINA STOCKS: Tech IPO Pipeline Eyed

- Shanghai Biren Technology: This GPU developer successfully listed on the Hong Kong Stock Exchange on January 2, 2026, raising approximately HK$5.6 billion as it jumped from HK$20 to HK$33 in three days of trading.

- Kunlunxin (Baidu AI chip unit): Baidu's AI chip unit filed a confidential listing application with the Hong Kong stock exchange in early January 2026 for a potential spin-off IPO.

- Iluvatar CoreX Semiconductor: This GPU developer is also expected to list in Hong Kong during 2026.

- News out Wednesday January 7 that BAIDU is planning to IPO its AI CHIP arm with expectations of up to $2bn in an IPO in Hong Kong.

OIL: Crude Continues Selling Off As Venezuelan Oil To Flow To US

Oil has faced further downward pressure today after US data showed large product inventory builds and President Trump announced Venezuela will ship “between 30 and 50 MILLION barrels of High Quality Sanctioned Oil” to the US. Both events added to ongoing concerns over a global supply glut pushing prices down further after Tuesday’s 2% decline. In addition, the discussion of security guarantees Tuesday may have brought a Ukraine deal closer.

- WTI is down 1.6% today to $56.24 after falling to $55.76 following Trump’s Truth Social post but holding above initial support at $54.89. Brent is 1.1% lower at $60.02 with the break below $60 short-lived. While technicals signal a dominant downtrend, it is holding above support at $58.53.

- Chevron & Quantum are set to bid for Lukoil’s assets after US imposed sanctions on Russia’s oil majors, according to the FT.

- Without a timeframe it is difficult to understand how Venezuela will be able to send 30-50mn barrels of oil to the US. The IEA reported that it produced only 860 kbd in November 2025 down from around 1mbd earlier.

- It is reported that Chevron, who still has operations in Venezuela, has sent 11 tankers to begin transporting oil to the US. Gulf refineries are geared to refine heavy, sour crude of the type that Venezuela produces.

- Bloomberg reported that there was a 2.8mn barrel US oil inventory drawdown last week, according to people familiar with the API data. Gasoline inventories rose 4.4mn and distillate 4.9mn. The official EIA data is out Wednesday.

- Later on Wednesday US December ADP employment, November JOLTS job openings, December ISM services and final October orders print. The Fed’s Bowman speaks on banking regulation. In Europe, preliminary December euro area CPI and November German unemployment & retail sales are released.

PRECIOUS METALS: Gold & Silver Lower Ahead Of The Week’s US Jobs Data

After rallying on Tuesday as geopolitical risks drove safe haven flows, gold & silver are lower in Wednesday’s APAC session. Precious metals appear to be steadying ahead of this week’s US jobs data, which finishes with payrolls on Friday and is likely to influence Fed easing expectations. Also the discussion of security guarantees Tuesday may have brought a Ukraine deal closer. US yields are little changed while the US dollar is down slightly.

- Gold is down 0.6% to $4465.5/oz after falling to $4459.92. It approached the 26 December record high at $4549.92 on Tuesday, which is the bull trigger. Any sell off is still corrective for now.

- Silver is 1.9% lower at $79.78/oz, close to the intraday low. It rose to $82.754 early in trading below the 28 December record at $84.0075, which is also the bull trigger. It remains in an uptrend but is also in overbought territory.

- Precious metals will be watching this week’s US labour market data closely given OIS pricing seems unsure if there will be another Fed rate cut in Q1 with a full 25bp not priced in before June.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.

- Equities are mixed with the S&P e-mini is slightly lower, the CSI is flat and Hang Seng down 1.0%. Oil continues to sell off with WTI -1.5% to $56.26/bbl. Copper is down 1.1%.

THAILAND: No Progress In Returning Inflation To Target Which BoT Is Aiming For

December Thai headline inflation printed in line with expectations at -0.3% y/y up from -0.5%, the ninth consecutive month of deflation, as lower energy prices and government price caps put downward pressure on prices. Core moderated to +0.6% y/y from +0.7%, slightly lower than expected, with the 2025 average at 0.8% up from 2024’s 0.6%. The government expects 2026 inflation to be positive at around 0-1.0%. but still only -0.5-0.0% in Q1.

- Underlying inflation spent most of last year below the bottom of the Bank of Thailand’s 1-3% band. It noted this week that while it will consider its limited policy space, it wants to ensure that inflation returns to the corridor and is ready to adjust policy as needed. It cut rates 100bp in 2025 and its next decision is 25 February.

- BoT has also been concerned about the degree of THB strength, which is driving imported inflation lower, and is not only monitoring it but also considering ways to manage the currency. In January to date, USDTHB is down 0.9% m/m and 8.6% y/y while the BIS THB NEER is up 5.0% y/y.

- There was an increase in food inflation to 1.5% y/y in December from -0.5% driven by fruit & vegetables. Rice & flour prices continued to fall at -1.9% y/y after -1.8%. Inflation rates of most non-food components fell further including energy at -7.0% y/y from -6.1%.

Thailand CPI y/y%

Source: MNI - Market News/LSEG

IDR: USDIDR Higher Again, 16800 Resistance Close By, BI Decision Looming

- Domestic news articles in recent day suggest that markets are increasingly concerned about the Rupiah potentially breaking past the Rp17,000 per USD level due to the perceived policy uncertainty from the Subianto government. As the line between government policy and the independent central bank appear to be blurring, the rupiah has underperformed, down -3.2% since July of last year.

- USDIDR is up again today by +24 and is near 16,776 / 16,785 on last dealings.

- The rupiah has lost -0.14% today whilst remaining neutral on the relative strength index.

- Next up for the embattled currency with be the Central Bank meeting on the 21st of January with current expectations that the December hold to support the currency will be mirrored.

- Tomorrow sees the release of the December foreign reserves, watched closely for guidance on intervention. BI employs a dual intervention strategy involving both foreign exchange spot and domestic non-deliverable forward markets, and purchasing government securities (SBN) in the secondary market. This is intended to address both exchange rate pressures and domestic liquidity conditions but of late seems to have limited impact on the direction of the currency, whilst smoothing volatility.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/01/2026 | 0700/0800 | ** | Retail Sales | |

| 07/01/2026 | 0745/0845 | ** | Consumer Sentiment | |

| 07/01/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/01/2026 | 0855/0955 | ** | Unemployment | |

| 07/01/2026 | 0900/1000 | *** | Bavaria CPI | |

| 07/01/2026 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 07/01/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 07/01/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 07/01/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 07/01/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 07/01/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 07/01/2026 | 1315/0815 | *** | ADP Employment Report | |

| 07/01/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | *** | JOLTS jobs opening level | |

| 07/01/2026 | 1500/1000 | *** | JOLTS quits Rate | |

| 07/01/2026 | 1500/1000 | * | Ivey PMI | |

| 07/01/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 07/01/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/01/2026 | 2110/1610 | Fed Vice Chair Michelle Bowman | ||

| 08/01/2026 | 2330/0830 | ** | average wages (p) | |

| 08/01/2026 | 0030/1130 | ** | Trade Balance | |

| 08/01/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 08/01/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 08/01/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 08/01/2026 | 0730/0830 | *** | CPI | |

| 08/01/2026 | 0745/0845 | * | Foreign Trade | |

| 08/01/2026 | 0830/0930 | ECB de Guindos Fireside Chat at Next Spain | ||

| 08/01/2026 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 08/01/2026 | 0930/0930 | BOE Decision Maker Panel data | ||

| 08/01/2026 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 08/01/2026 | 1000/1100 | ** | EZ PPI | |

| 08/01/2026 | 1000/1100 | ** | EZ Unemployment | |

| 08/01/2026 | 1330/0830 | *** | Jobless Claims | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity |