PRECIOUS METALS: Gold & Silver Lower Ahead Of The Week’s US Jobs Data

After rallying on Tuesday as geopolitical risks drove safe haven flows, gold & silver are lower in W...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USD - BBDXY Testing 1210-1211 Again

The BBDXY has had a range today of 1210.91 - 1212.57 in the Asia-Pac session; it is currently trading around 1211, -0.10%. The USD has traded slightly softer in the Asian session. US yields extended their bounce last week and risk has consolidated its recent gains. The USD saw decent demand back toward the 1211 area at the back-end of last week and it looks like the range 1210-1230 could be here for the moment. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, support remains toward 1210/11 which needs to be worked through and then the more important 1205 area.

- EUR/USD - Asian range 1.1639-1.1655, Asia is currently trading 1.1655. The pair continues to consolidate around the 1.1650 area. On the day it looks like dips back toward 1.1580-1600 could be supported initially, looking to retest the 1.1680 area again eventually.

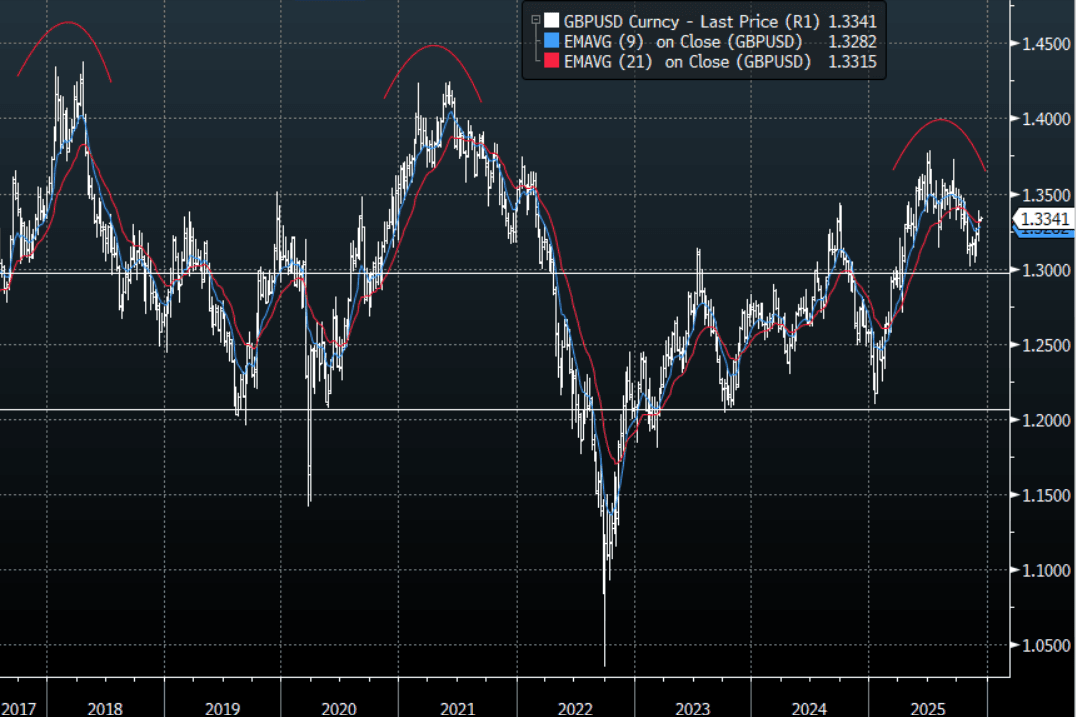

- GBP/USD - Asian range 1.3323-1.3342, Asia is currently dealing around 1.3340. The pair is consolidating on a 1.33 handle. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3260-1.3290 area, while above here look for the market to test the 1.3370-90 area again at some point.

- Cross asset : SPX +0.20%, Gold $4210, US 10-Year 4.133%, BBDXY 1211, Crude Oil $60.22

- Data/Events : EZ Sentix Investor Confidence, Germany Industrial Production SA

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Markets Await FED as Japan Growth Stumbles

- Despite the worse than expected GDP, the NIKKEI has hovered around where it began the day at 50,478 above the 20-day EMA of 49,919

- The KOSPI is up again with key tech stocks like Samsung over up over +1.2% today, seeing the index up by +0.25% and the TAIEX rose +0.93% has TSMC jumped over 2% Monday.

- The onshore offshore divide was evident in China with the Hang Seng down heavily by -1.1%, whilst the CSI 300 rose by over 1%. Shenzhen is the outperformer on the day with gains of +1.3% with some tech stocks up strongly. The performance highlights a strong investor focus on technology and advanced manufacturing sectors, which have been a key growth area in the region

- The NIFTY 50 continues to moderate and is down -0.12% Monday. Since hitting new highs on NOV 27, the NIFTY has fallen five out of seven trading days though the losses have been contained. The NIFTY sits only 0.25% below the high of 26,215.

- SE Asia's bourses are led again by the Jakarta Composite which is up strongly by +0.95%, to reach overbought on the 14-day Relative Strength Index. It last reached overbought in August where it remained for several trading days. The FTSE Malay KLCI is down -0.55% and teh SE Thai -0.10%

GOLD: Range Trading As Wait For Wednesday’s Fed Decision

Gold prices are slightly higher in Monday’s APAC trading supported by a lower US dollar (BBDXY -0.1%) but have moved in a very narrow range of $4195.60/4213.17. They are currently up 0.3% to $4211.8/oz. Bullion, like other assets, will probably remain in a narrow range ahead of the Fed decision on Wednesday. The market has 23bp of easing priced in but it could be a hawkish cut, which may weigh on gold.

- Silver is down 0.6% to $58.02 oz today, driven by profit taking, after rising 2.1% on Friday. It finished last week up 3.3% and has been hovering around overbought on a 14-day RSI basis, according to Bloomberg. It started today at a high of $58.789, just below initial resistance at $58.979. The metal remains in an uptrend supported by a resumption of ETF inflows.

- Gold continues to trade between initial resistance at $4264.7 and initial support at $4139.7, 20-day EMA. The bull trigger is at $4381.5.

- PBoC data for November showed a 30k troy oz rise in gold reserves, the thirteenth consecutive monthly increase.

- Equities are mixed with the S&P e-mini up 0.2% and CSI 300 +1.0% but Hang Seng down 1.1% and ASX -0.2%. Oil prices are little changed with WTI +0.2% to $60.23/bbl. Copper is down 0.3%.

- Later US November NY Fed 1-yr inflation expectations and German October IP print. The ECB’s Cipollone and BoE’s Taylor & Lombardelli speak.