CHINA STOCKS: Tech/Govt Initiatives In Focus, Attractive Valuations Help Gains

- Artificial Intelligence (AI): The AI sector, particularly AI chips, has been a primary driver of the recent market rally, benefiting from investor optimism and policy support. Though the AI / tech sector has somewhat lagged behind that of Korean and Japanese names, an opportunity some asset allocators are focusing on

- Domestic Semiconductor Production: A central pillar of Beijing's push for tech self-reliance, with directive-driven demand for Chinese-made AI chips in state data centers.

- New Energy Technologies: This sector is expected to benefit from continued government policy support and the country's pivot toward innovation-led growth.

- Innovative Drugs: The innovative pharmaceuticals industry is another area identified for potential growth within the new market phase.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

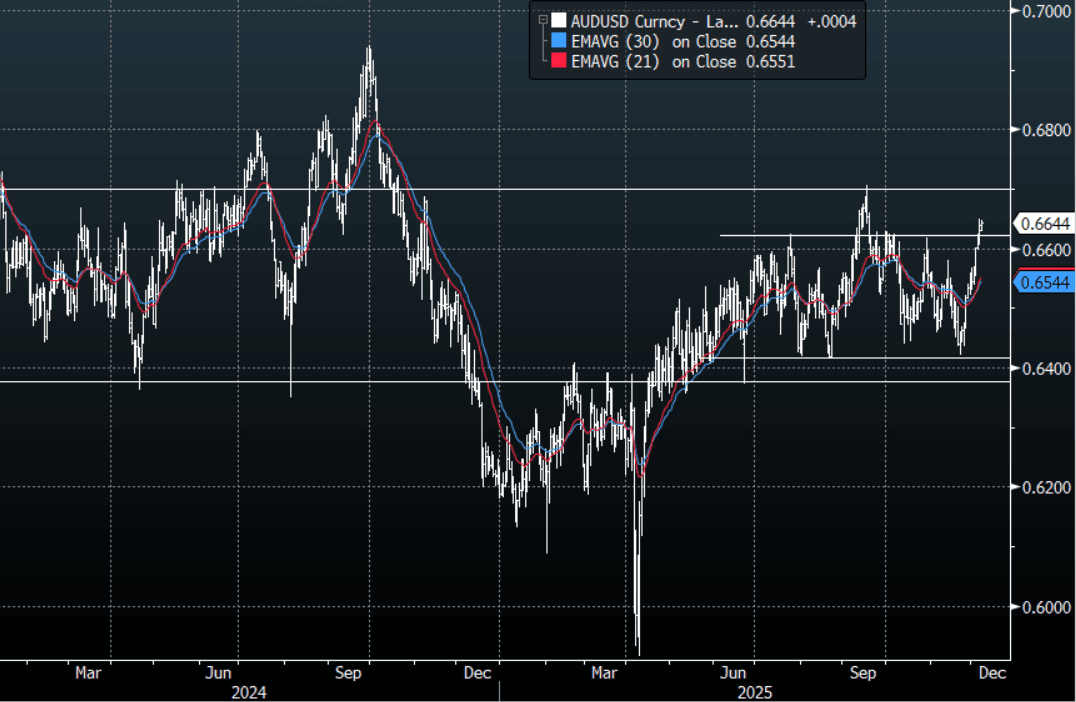

AUD: AUD/USD - Trying To Build On Break Above 0.6630

The AUD/USD has had a range today of 0.6631 - 0.6648 in the Asia- Pac session, it is currently trading around 0.6645, +0.10%. The AUD/USD is trying to build some momentum on its break above 0.6630. The AUD price action remains very constructive and indicative of a market with solid buying interest. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, look to see if the AUD can hold above this 0.6620/30 area. It has come a long way so if this does not hold we could see a pullback, first support below that is toward 0.6570/90 where we should see demand reappear. Ultimately the AUD is looking to rebuild momentum to have another look back toward the 0.6700 area at some point. RBA tomorrow and the FOMC later this week should dictate the upcoming price action.

- MNI AU - The focus of the week is on Tuesday’s RBA decision but Thursday’s November jobs data will also be important. The RBA is unanimously expected to leave rates at 3.6% with the market pricing in no chance of a move in either direction. Therefore, the statement will be scrutinised to gauge the Board’s thinking regarding the outlook and especially if there is a change to the balance of risks and a shift to concern about upside ones to inflation after October trimmed mean printed at 3.3%.

- “CHALMERS: TO DELIVER MID YEAR BUDGET OUTLOOK NEXT WEEK" : BBG

- MNI AU - RBA-dated OIS pricing is slightly firmer today, showing tightening across all meetings, with the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6475(AUD814m), 0.6500(AUD342m). Upcoming Close Strikes : 0.6550(AUD1.59b Dec 11) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 35 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Heavy Session Outright & Relatively Vs $-Bloc

NZGBs closed 5-10bps cheaper, led by the 5-year. Accordingly, NZGBs sit amazingly 18-38bps higher than pre-RBNZ levels. (see chart)

- On a relative value basis, the 5-year swap is at its cheapest valuation since mid-2022, based on the 2-/5-/10-year butterfly spread.

- Versus the $-bloc, NZGBs also underperformed sharply, with the NZ-US and NZ-AU 10-year yield differential 5-6bps higher. At +30bps, NZ-US differential is back at April levels.

- Swap rates closed 10-13bps higher, with a steeper 2s10s curve.

- RBNZ-dated OIS pricing closed firmer across meetings. No easing is now priced for February, while November 2026 assigns 44bps of tightening.

- The local calendar was empty today and will remain so until Wednesday, when RBNZ Governor Breman hosts a media Q+A alongside Net Migration data.

- On Thursday, the NZ Treasury plans to sell NZ$175mn of the 4.50% May-30 bond, NZ$200mn of the 3.50% Apr-33 bond and NZ$75mn of the 5.00% May-54 bond.

Bloomberg Finance LP

MNI EXCLUSIVE: The BoJ & JGB Yields

MNI discusses the BOJ's stance on recent JGB yield moves.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com