FOREX: A$ Gains The Standout, AUD/NZD At Fresh Cycle Highs, Steady Elsewhere

Outside of AUD gains, the price action in the G10 has been very muted so far today. The USD BBDXY index sits little changed near 1205.10 in latest dealings. The A$ sits up 0.35% to 0.6760/65, fresh highs back to 2024. We saw a brief dip to 0.6717 post a slightly softer Nov CPI read, but this was well supported. We are just above the Oct 11 2024 high of 0.6759, with the 0.6800 region now likely to come into focus. AU rates, particularly at the front end, were also supported from a yield stand point. RBA tightening expectations for 2026 sit slightly firmer versus pre CPI levels. Outside of rate expectations, the metals commodity backdrop is also aiding the AUD, with iron ore gains notable today.

- Shifts elsewhere in the G10 space are less than 0.1% at this stage. NZD/USD is little changed, last 0.5780/85, while USD/JPY is just under 156.60. EUR/USD is up a touch but still under 1.1700 at this stage.

- The AUD/NZD cross is trending towards 1.1700, fresh highs back to 2013. AUD/JPY is near 105.90, fresh highs back to mid 2024.

- We are seeing softer gold and silver trends so far today, but the BBG metals spot sub index is up 16% since late Nov lows. Iron ore is above $108.50/ton per the active SGX contract.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Holding Onto Gains As Watching Ukraine Developments

Oil prices are marginally higher as the market monitors Ukraine/Russia developments with negotiations ongoing, US President Trump criticizing Ukraine’s President Zelenskyy, Ukraine striking Russian refineries and Russia’s President Putin encouraging Indian oil purchases. Market expectations that there would be a peace deal faded over last week driving oil prices higher and they remain sensitive to events.

- WTI is up 0.2% to $60.21/bbl after falling to $59.97 with moves below $60 short-lived. It rose 2.7% last week. Brent is 0.2% higher at $63.88/bbl following a peak of $63.94 and a low at $63.63. It was up 2.4% last week.

- Both benchmarks have been in a very narrow range today as they wait for more information regarding geopolitical developments, including Venezuela, and monthly oil reports. Forecasts will be monitored closely for any upward revisions to 2026 surplus projections. The EIA short-term energy outlook is on Tuesday and OPEC & IEA reports on Thursday.

- Trump said that he was disappointed with how Zelenskyy has treated the latest US proposal and accused him of not reading it.

- The US and Ukraine agreed on a “framework for security arrangements” with “necessary deterrence capabilities to sustain a lasting peace”, according to the US State Department. However, Russia said that Trump’s National Security Strategy was “largely consistent” with Russia’s view.

- Ukraine struck Rosneft’s Ryazan refinery on the weekend in response to heavy attacks on its energy generation. This followed strikes late last week on Russia’s Syzran refinery and Temryuk port.

- Later US November NY Fed 1-yr inflation expectations and German October IP print. The ECB’s Cipollone and BoE’s Taylor & Lombardelli speak.

FOREX: USD - BBDXY Testing 1210-1211 Again

The BBDXY has had a range today of 1210.91 - 1212.57 in the Asia-Pac session; it is currently trading around 1211, -0.10%. The USD has traded slightly softer in the Asian session. US yields extended their bounce last week and risk has consolidated its recent gains. The USD saw decent demand back toward the 1211 area at the back-end of last week and it looks like the range 1210-1230 could be here for the moment. On the day look for resistance again back towards the 1215-1217 area where sellers should remerge initially, support remains toward 1210/11 which needs to be worked through and then the more important 1205 area.

- EUR/USD - Asian range 1.1639-1.1655, Asia is currently trading 1.1655. The pair continues to consolidate around the 1.1650 area. On the day it looks like dips back toward 1.1580-1600 could be supported initially, looking to retest the 1.1680 area again eventually.

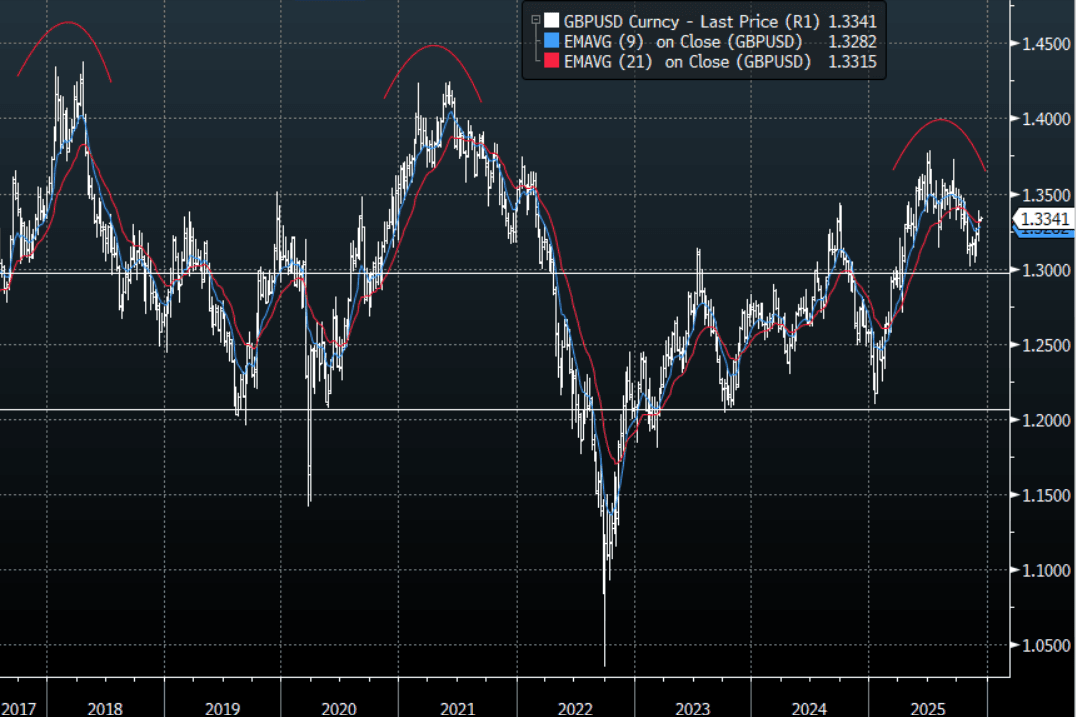

- GBP/USD - Asian range 1.3323-1.3342, Asia is currently dealing around 1.3340. The pair is consolidating on a 1.33 handle. I remain skewed toward shorts but patience is required and we are now approaching levels where I will be watching for any signs of potentially topping out. On the day GBP should see support back toward the 1.3260-1.3290 area, while above here look for the market to test the 1.3370-90 area again at some point.

- Cross asset : SPX +0.20%, Gold $4210, US 10-Year 4.133%, BBDXY 1211, Crude Oil $60.22

- Data/Events : EZ Sentix Investor Confidence, Germany Industrial Production SA

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Markets Await FED as Japan Growth Stumbles

- Despite the worse than expected GDP, the NIKKEI has hovered around where it began the day at 50,478 above the 20-day EMA of 49,919

- The KOSPI is up again with key tech stocks like Samsung over up over +1.2% today, seeing the index up by +0.25% and the TAIEX rose +0.93% has TSMC jumped over 2% Monday.

- The onshore offshore divide was evident in China with the Hang Seng down heavily by -1.1%, whilst the CSI 300 rose by over 1%. Shenzhen is the outperformer on the day with gains of +1.3% with some tech stocks up strongly. The performance highlights a strong investor focus on technology and advanced manufacturing sectors, which have been a key growth area in the region

- The NIFTY 50 continues to moderate and is down -0.12% Monday. Since hitting new highs on NOV 27, the NIFTY has fallen five out of seven trading days though the losses have been contained. The NIFTY sits only 0.25% below the high of 26,215.

- SE Asia's bourses are led again by the Jakarta Composite which is up strongly by +0.95%, to reach overbought on the 14-day Relative Strength Index. It last reached overbought in August where it remained for several trading days. The FTSE Malay KLCI is down -0.55% and teh SE Thai -0.10%