IDR: USDIDR Higher Again, 16800 Resistance Close By, BI Decision Looming

- Domestic news articles in recent day suggest that markets are increasingly concerned about the Rupiah potentially breaking past the Rp17,000 per USD level due to the perceived policy uncertainty from the Subianto government. As the line between government policy and the independent central bank appear to be blurring, the rupiah has underperformed, down -3.2% since July of last year.

- USDIDR is up again today by +24 and is near 16,776 / 16,785 on last dealings.

- The rupiah has lost -0.14% today whilst remaining neutral on the relative strength index.

- Next up for the embattled currency with be the Central Bank meeting on the 21st of January with current expectations that the December hold to support the currency will be mirrored.

- Tomorrow sees the release of the December foreign reserves, watched closely for guidance on intervention. BI employs a dual intervention strategy involving both foreign exchange spot and domestic non-deliverable forward markets, and purchasing government securities (SBN) in the secondary market. This is intended to address both exchange rate pressures and domestic liquidity conditions but of late seems to have limited impact on the direction of the currency, whilst smoothing volatility

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

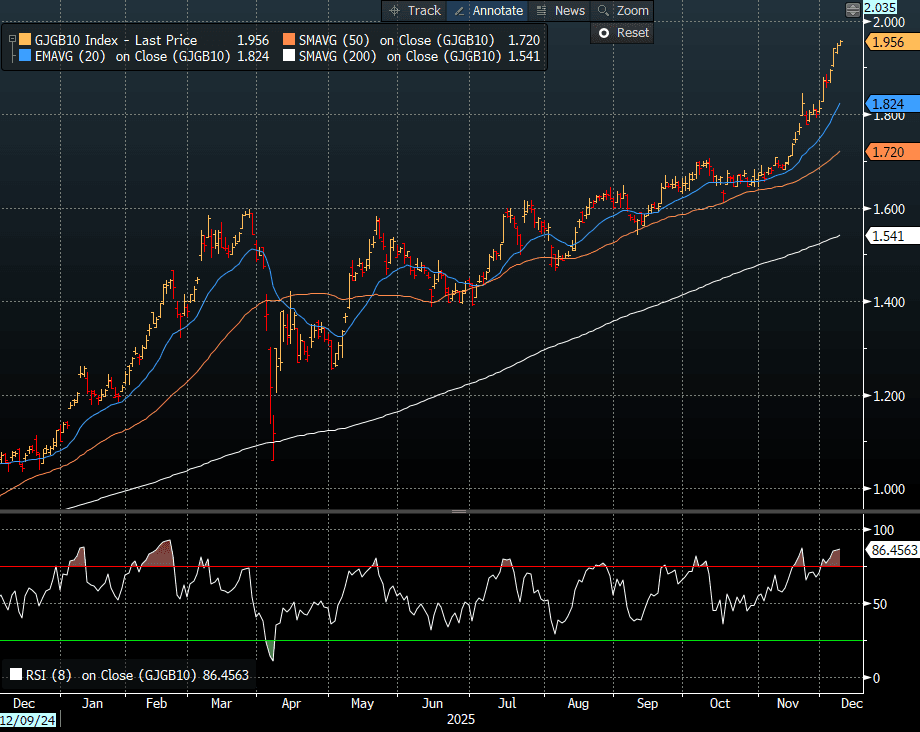

JGBS: Mostly Cheaper With 10YY A Fresh Cycle High ut A Subdued Session

JGB futures are slightly weaker, -3 compared to settlement levels, after a relatively subdued session.

- MNI Techs Team - Futures prices traded to new pullback and cycle lows again Friday, weighed by building expectations of a December BoJ rate hike and a breach of support in futures prices. This affirms the firm downtrend that's dominated prices since mid-September, and prices will need to challenge resistance before signalling any broader reversal. Key short-term resistance has been defined at 137.30, the Sep 8 high.

- MNI - Japan's Q3 GDP fell 0.6% q/q, or an annualised -2.3%, compared with the initial estimate of -0.4% q/q, or -1.8% annualised, as capital investment and public spending were revised down, although private consumption was revised slightly higher. Private consumption, which accounts for about 60% of Japan's GDP, was revised up to 0.2% from 0.1%, though its contribution remained unchanged at 0.1 pp.

- Cash US tsys are little changed in today's Asia-Pac session after Friday's modest sell-off.

- Cash JGBs are 2.5bps cheaper (20-year) to 0.5bp richer (40-year) across benchmarks, with the 10-year yield 1.0bp higher at 1.958%, a fresh cycle high.

- Swap rates are 1-3bps higher, with a steeper curve.

- Tomorrow, the local calendar will see Money Stock and Machine Tool Orders data alongside 5-year supply.

Source: Bloomberg Finance LP

US TSYS: Bonds Give Back Early Gains

US bond futures gave back earlier gains to be near where they started in the afternoon session. The US 10-Yr is flat at 112-17+ near to the 100-day EMA of 112-15. Topside resistance is the 50-day EMA of 112-26.

Cash has trended back to relatively unchanged across the curve having been lower in yields earlier.

- The 2-Yr is at 3.563%

- The 5-Yr is at 3.713%

- The 10-Yr is at 4.137%

- The 30-Yr is at 4.793%

There are no Tier 1 data releases tonight with markets looking ahead to the JOLTs Job Openings for October

Ahead tonight is a 13 and 26 week bill auction, with the focus being the U$58bn 3-Year auction.

OIL: Crude Holding Onto Gains As Watching Ukraine Developments

Oil prices are marginally higher as the market monitors Ukraine/Russia developments with negotiations ongoing, US President Trump criticizing Ukraine’s President Zelenskyy, Ukraine striking Russian refineries and Russia’s President Putin encouraging Indian oil purchases. Market expectations that there would be a peace deal faded over last week driving oil prices higher and they remain sensitive to events.

- WTI is up 0.2% to $60.21/bbl after falling to $59.97 with moves below $60 short-lived. It rose 2.7% last week. Brent is 0.2% higher at $63.88/bbl following a peak of $63.94 and a low at $63.63. It was up 2.4% last week.

- Both benchmarks have been in a very narrow range today as they wait for more information regarding geopolitical developments, including Venezuela, and monthly oil reports. Forecasts will be monitored closely for any upward revisions to 2026 surplus projections. The EIA short-term energy outlook is on Tuesday and OPEC & IEA reports on Thursday.

- Trump said that he was disappointed with how Zelenskyy has treated the latest US proposal and accused him of not reading it.

- The US and Ukraine agreed on a “framework for security arrangements” with “necessary deterrence capabilities to sustain a lasting peace”, according to the US State Department. However, Russia said that Trump’s National Security Strategy was “largely consistent” with Russia’s view.

- Ukraine struck Rosneft’s Ryazan refinery on the weekend in response to heavy attacks on its energy generation. This followed strikes late last week on Russia’s Syzran refinery and Temryuk port.

- Later US November NY Fed 1-yr inflation expectations and German October IP print. The ECB’s Cipollone and BoE’s Taylor & Lombardelli speak.