MNI EUROPEAN MARKETS ANALYSIS: JGB 10yr Above 2.00% Post BoJ

- The BoJ hiked rates as expected and maintained a tightening bias, but gave not hints on timing. JGB yield gains gained momentum as the session progressed, the 10yr through 2.00%. All eyes now on BoJ Governor Ueda's upcoming press conference. USD/JPY rose post the BoJ, but found selling interest above 156.00.

- NZ consumer and business sentiment data rose for Dec (business readings at cycle highs), pointing to an improved economic outlook, but NZD and local yields didn't react positively.

- Regional equities are ending the week firmer, with tech related bourses outperforming.

- Looking ahead, UK and Canadian retail sales are scheduled Friday, alongside US existing home sales data. The Fed Williams appears on CNBC as well.

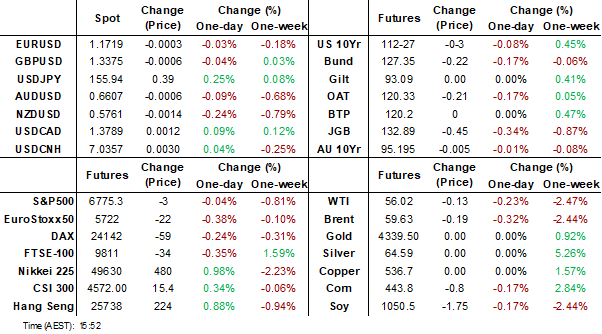

MARKETS

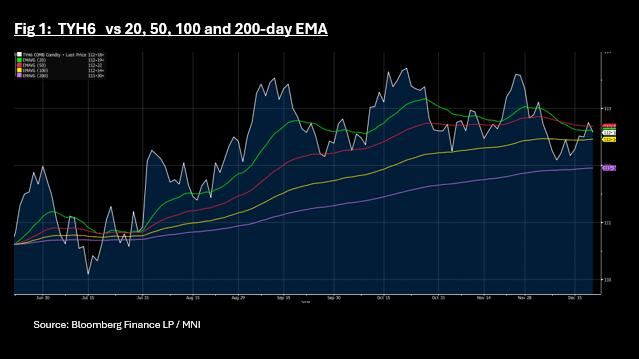

US TSYS: Yields Ending Week Near Bottom End of Recent Ranges

US bond futures fell today as equities rebounded and the BOJ raised rates. The 10-Yr is down -05 to 112-18. TYH6 remains higher by +12+ for the week, and near to the 20-day EMA of 112-19. A break below would see downside resistance from the 100 day EMA of 112-14+.

Cash is weak with yields higher across the curve, with the 2-year and 10-year near the bottom end of the weekly range.

- The 2-Yr is up +1.1bps today to 3.473%: weekly range 3.462% - 3.5044%

- The 5-Yr is up +1.8bps today to 3.681%: weekly range 3.663% - 3.726%

- The 10-Yr is up +1.8bps today to 4.141%: weekly range 4.124% - 4.176%

- The 30-yr is up +1.7bps today to 4.822%: weekly range 4.805% - 4.848%

There are no scheduled bond auctions at this stage tonight.

Data wise home sales, Michigan sentiment and Kansas City Activity are out.

BOJ: Hikes & Retains Tightening Bias, No Hints On Timing

The BoJ hiked rates by 25bps to 0.75%, as widely expected by both sell-side economists and what was priced in by the market. As expected the BoJ kept the bias for further rate hikes intact, by stating it will keep raising rates if the economic and price outlook is realized. Timing on further rate hikes wasn't provided though. Supporting the stance around further rate hikes, the BOJ stated that accommodative conditions will keep supporting the economy and that real rates remain at a significantly low level. This fits with the BoJ still seeing policy rates under neutral levels (with the range being described in the 1-2.5% area for neutral). This is something that is likely to be a focus point at Governor Ueda's press conference later. This is held at 3:30pm local time.

- While the decision was unanimous to raise rates, board members Tamura and Takata objected to the description of the price outlook. Takata stating that the rate of increase in CPI inflation, along with underlying CPI, was already around the price stability target.

- The core board view was that underlying inflation was likely to converge with the BoJ's target in the latter half of the 3yr projection period. On growth, the economy was seen as recovering modestly with some pockets of weakness.

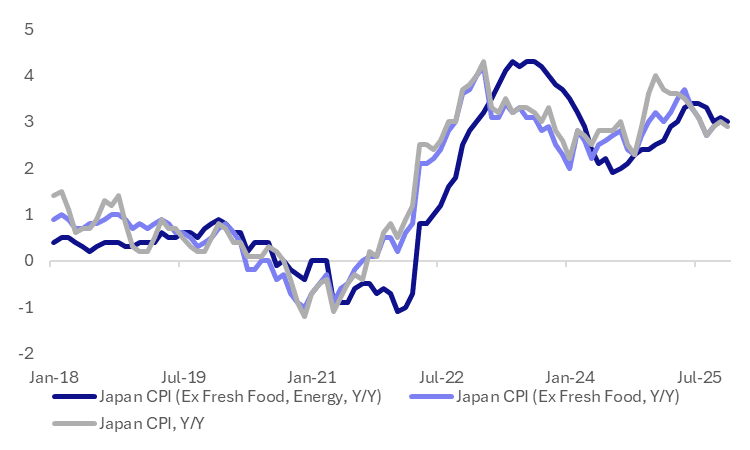

JAPAN DATA: Nov CPI Around 3%y/y, Services Inflation Unchanged At 1.6%y/y

Japan Nationwide CPI for Nov was in line with market forecasts and suggested little shift in y/y momentum relative to Oct. The headline was 2.9%y/y (prior 3.0%), while the core ex fresh food was 3.0% (unchanged versus Oct), while core ex fresh food, energy was 3.0%y/y (against 3.1y/y for Oct). The chart below plots these three inflation metrics in y/y terms, with recent trends settling near the 3% y/y, off earlier 2025 highs, but well above the BoJ's 2% inflation target. Still, services inflation, a key BoJ watch point, remained unchanged in y/y terms at 1.6%.

- In m/m terms, headline rose 0.4%, the same as the Oct pace, while the core measures were positive but lower than Oct's pace. Goods prices rose 0.7%m/m, while services were +0.2% higher.

- By sub category, outside of utilities (+3.8%m/m) other segments were mostly softer compared to the Oct outcome. Transport fell 0.3%m/m, entertainment was -0.3%m/m and household goods were down by 0.6%m/m.

Fig 1: Japan CPI Trends Y/Y, Broadly Unchanged In Nov

Source: Bloomberg Finane L.P./MNI

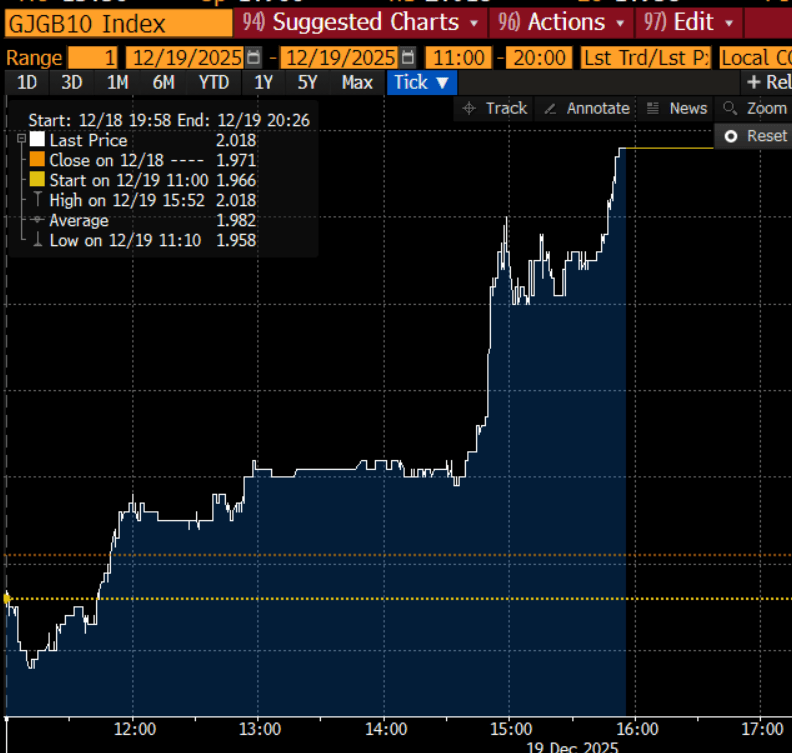

JGBS: Post-BOJ Decision Sell-Off Gathers Pace

JGB futures (JBH6) have cheapened dramatically, -45 compared to settlement levels, after an initial muted reaction to the BOJ decision to hike rates.

- The BOJ unanimously raised the overnight call rate to 0.75%, the highest in 30 years, citing a significantly low real rate and growing confidence that its economic and price outlook will be realised. The BOJ signalled it will continue raising rates in line with improvements in growth, wages and inflation, while maintaining accommodative conditions to support the economy.

- While the decision was unanimous to raise rates, board members Tamura and Takata objected to the description of the price outlook. Takata stated that the rate of increase in CPI inflation, along with underlying CPI, was already around the price stability target.

- Cash US tsys are ~2bps cheaper in today's Asia-Pac session.

- BOJ-dated OIS is slightly firmer after the hike, assigning a 68% probability to a 25bp hike by June, rising to 108% by September 2026.

- Cash JGBs are 2-4bps cheaper across benchmarks, with the 5-year yield 5bps higher. The benchmark 10-year yield is 4.7bp higher at 2.018%, a fresh cycle high (see chart).

- Swap rates are 2-5bps higher.

- On Monday, the local calendar will be light, with Tokyo Condominiums for Sale the only release.

Source: Bloomberg Finance LP

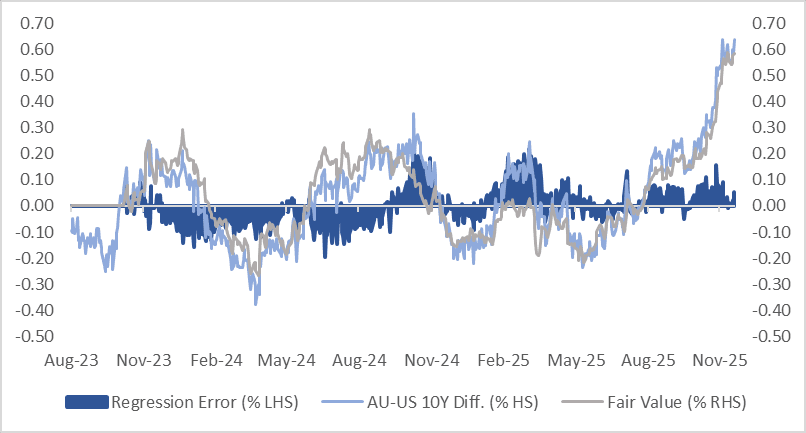

AUSSIE BONDS: Cheaper & Near Worst Levels, AU-US 10Y Diff At Highs

ACGBs (YM -4.0 & XM -2.0) are modestly weaker, although trading near the session’s worst levels.

- Private credit rose 0.6% m/m (estimate +0.6%) in November versus +0.7% in October.

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +62bps, around its cycle high. While the differential has moved a considerable distance, the bias remains higher, given the relative outlook for the respective central bank policy rates in the first part of 2026.

- That said, a simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is around 5bps above fair value.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 35% for February to 100% by June and 153% by December 2026.

- Next week, the local calendar will be light apart from the RBA Minutes of the December Meeting on Tuesday.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Bloomberg Finance LP / MNI

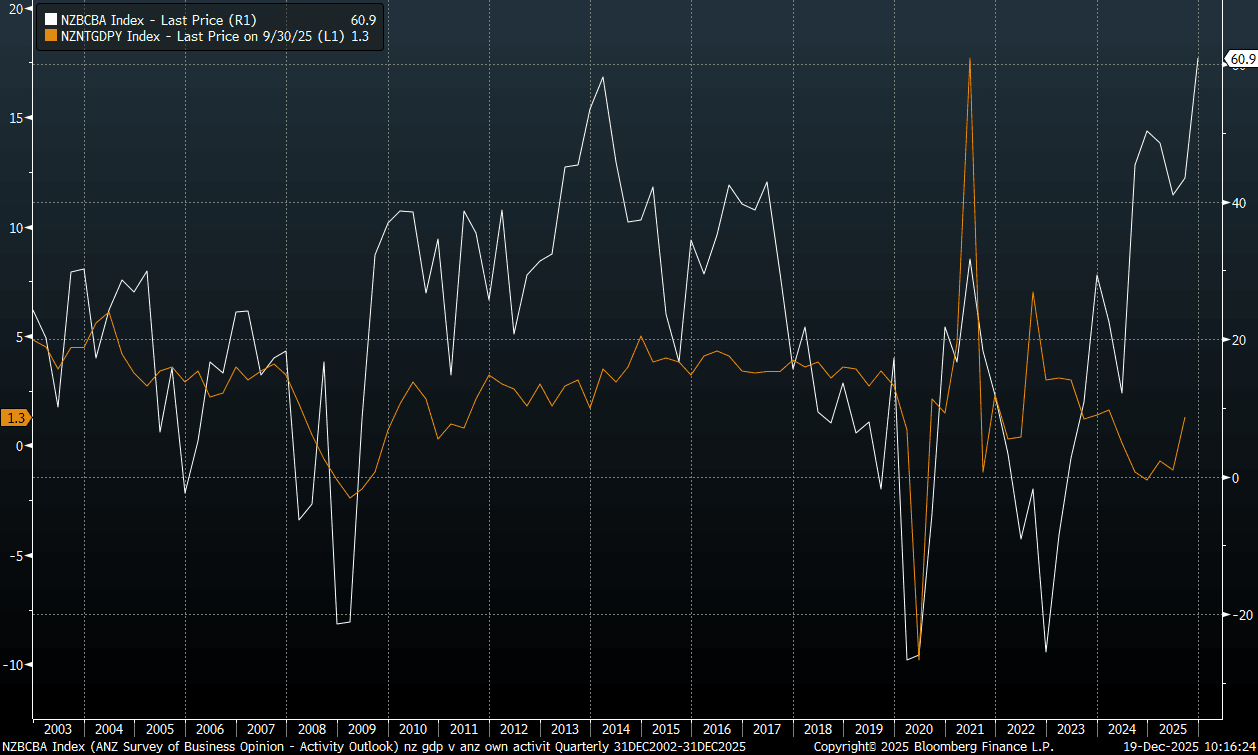

NEW ZEALAND: ANZ Business Confidence & Activity To Fresh Cycle Highs

ANZ's business confidence and activity measures for New Zealand rose strongly in Dec. Activity is at 60.9 from 53.1 prior, while confidence is up to 73.6, from 67.1 in Nov. These are cycle high readings for both indices and points to growing optimism around the economic outlook. The chart below plots the activity measure, the white line, against y/y NZ GDP growth (which only printed for Q3 yesterday). There is by no means a perfect relationship between the two series, but such levels in business activity (and confidence) usually coincide with higher levels of y/y GDP growth or at least upward momentum. Today's ANZ prints (with consumer confidence also up earlier) will reinforce an on hold RBNZ in the first part of 2026. Market reaction has been limited though, NZD/USD holds a touch weaker for the session (last 0.5700/75), while the 2yr swap rate and onshore bond yields are still down for the session (NZGB yields around 2-4bps weaker).

- All the sub components from the survey improved, with residential and commercial construction up noticeably. The employment index rose to 27.5, from 18.5.

- Inflation expectations were unchanged at 2.69%, while via BBG: "while a net 51.7% of firms expect to raise prices, vs 50.5%." The local bank also noted: “The 2024 slowdown was deliberately induced by monetary policy, and now that that has eased, there is not a lot else holding the economy back”: ANZ (via BBG).

Fig 1: ANZ Business Activity & NZ GDP Y/Y

Source: Bloomberg Finance L.P./MNI

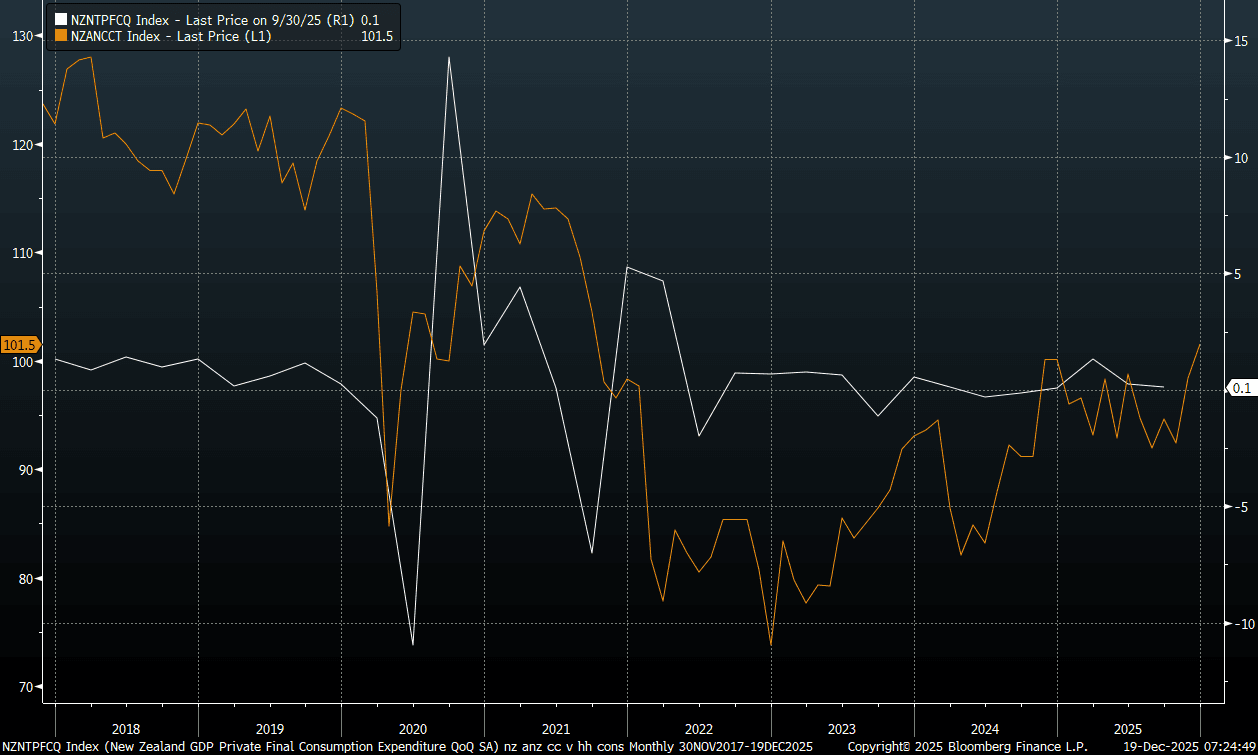

NEW ZEALAND: ANZ Consumer Sentiment Recovers Further, Supporting Spend Outlook

The ANZ New Zealand consumer confidence measure rose to 101.5 in Dec, a 3.2% (after gaining 6.5% in Nov). This puts the index at its highest levels since the second half of 2021. The chart below plots this consumer sentiment index (the orange line in the chart) against private consumption growth (q/q) from the NZ national accounts. The rise in sentiment is pointing to further improvement in the spending backdrop and comes after the rise in the Q4 Westpac consumer sentiment reading earlier this week (although this measure remain sub 100).

- In terms of the detail, all of the sub indices improved, while the buy a major household item printed at -1 versus -9 in Nov. Inflation expectations edged down to 4.6%.

- Via BBG: "Gain reflects falling food prices and “generally improving headlines about the state of the economy and the outlook for the year ahead”: ANZ".

Fig 1: NZ ANZ Consumer Sentiment & Private Consumption Growth Q/Q

Source: ANZ/Bloomberg Finance L.P/MNI

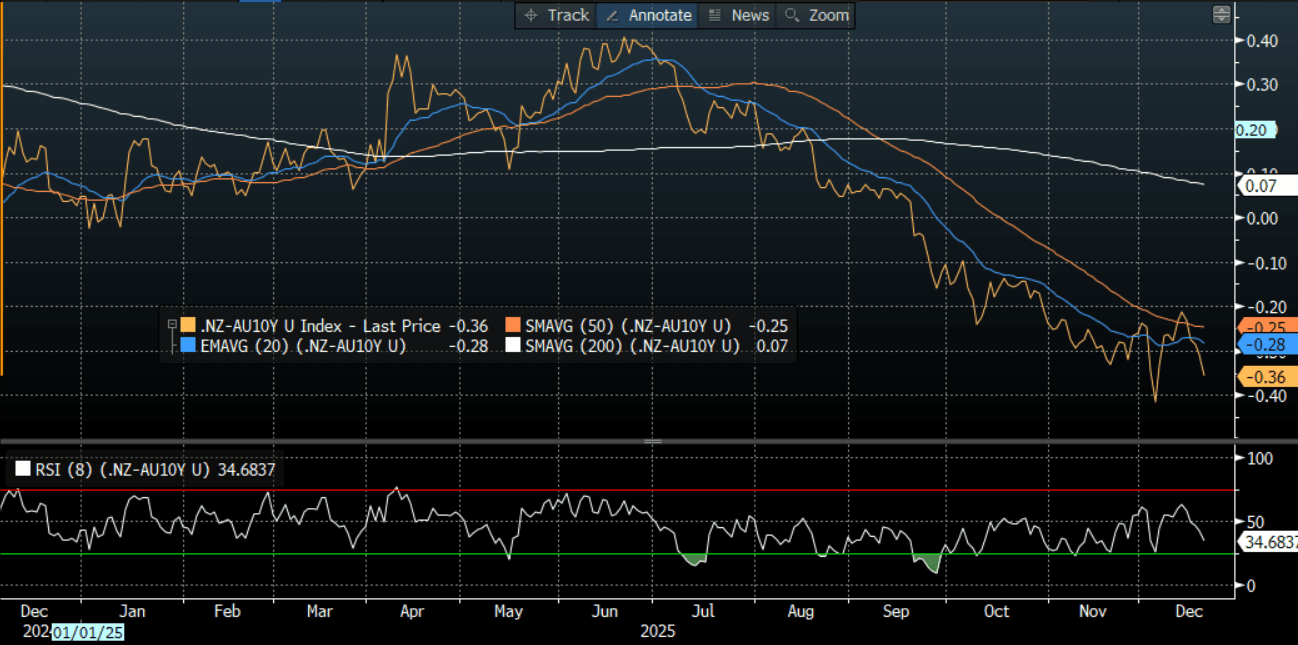

BONDS: NZGBS: Richer, NZ-AU 10Y Diff Back Near Lows

NZGBs closed 1-3bps richer, with the 5-10-year zone leading. The 5-year yield, nevertheless, remains 35bps higher than pre-RBNZ levels.

- The NZ–AU 10-year spread has returned close to cycle lows after briefly rising by around 20bps following the RBNZ’s final policy meeting of the year. The subsequent move back toward the lows was driven by comments this week from RBNZ Governor Anna Breman, who pushed back against market expectations of an interest-rate hike next year, indicating that the OCR is likely to remain unchanged for some time (see chart).

- NZ domestic spending on all cards rises 1.6% m/m, +4.7% y/y.

- NZ business confidence soared to a three-decade high in December and the mood of consumers also surged, adding to signs of further economic expansion. A net 74% of firms expect better business conditions — the most since March 1994, ANZ Bank said. Expectations of own-trading were also at a 31-year high, while a monthly gauge of consumer sentiment rose to 101.5 in December, the highest since September 2021, ANZ said in a second report.

- RBNZ-dated OIS pricing shows no tightening priced for February, while November 2026 assigns 42bps.

- Next week, the local calendar will be empty in the run-up to the Christmas break.

Bloomberg Finance LP

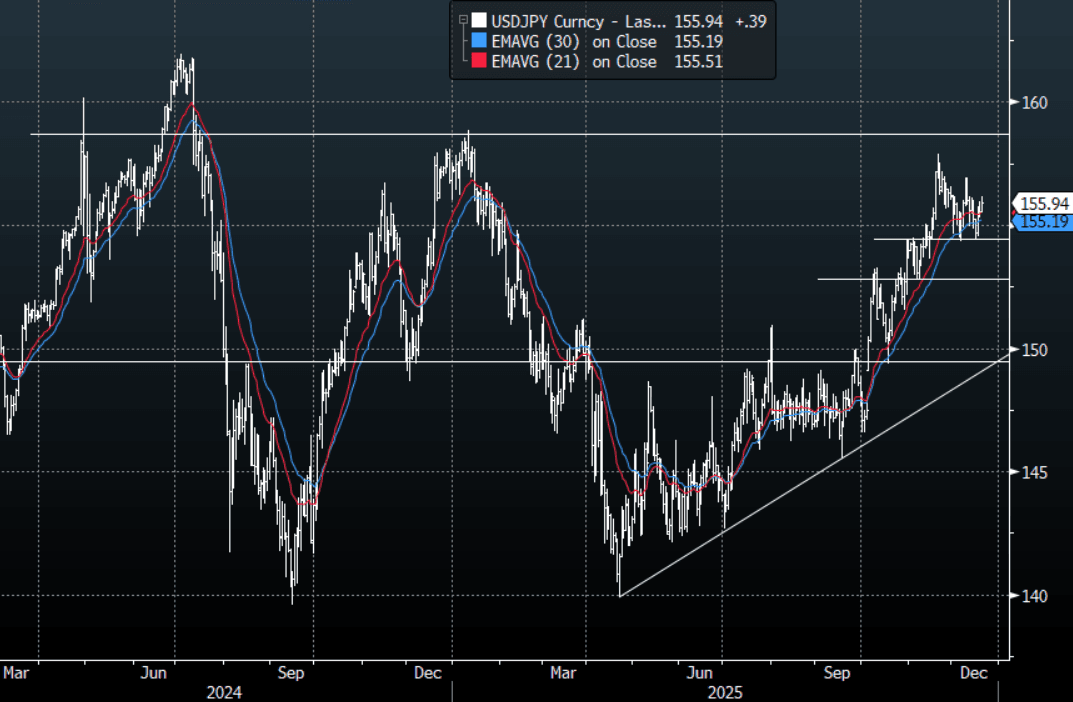

JPY: USD/JPY - Tests 156.00-30 After BOJ, Resistance Holds For Now

The USD/JPY range today has been 155.50 - 156.16 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. USD/JPY first traded a little lower after the BOJ raised rates but it quickly returned to challenge the 156.00-156.30 area which has capped the move in our session. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. On the day, resistance is between the 156.00-156.30 area initially, support is seen back toward 154.50-155.00 where demand has been strong recently. A break above 156.30 would potentially open up a move back toward 157.00.

- MNI AU - Hikes & Retains Tightening Bias, No Hints On Timing: The BoJ hiked rates by 25bps to 0.75%, as widely expected by both sell-side economists and what was priced in by the market. As expected the BoJ kept the bias for further rate hikes intact, by stating it will keep raising rates if the economic and price outlook is realized. Timing on further rate hikes wasn't provided though. Supporting the stance around further rate hikes, the BOJ stated that accommodative conditions will keep supporting the economy and that real rates remain at a significantly low level. This fits with the BoJ still seeing policy rates under neutral levels (with the range being described in the 1-2.5% area for neutral). This is something that is likely to be a focus point at Governor Ueda's press conference later. This is held at 3:30pm local time.

- MNI AU - Nov CPI Around 3%y/y, Services Inflation Unchanged At 1.6%y/y: Japan Nationwide CPI for Nov was in line with market forecasts and suggested little shift in y/y momentum relative to Oct. The headline was 2.9%y/y (prior 3.0%), while the core ex fresh food was 3.0% (unchanged versus Oct), core ex fresh food, energy was 3.0%y/y (against 3.1y/y for Oct). Services inflation, a key BoJ watch point, remained unchanged in y/y terms at 1.6%.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($2.66b), 158.00($1.85b). Upcoming Close Strikes : 155.00($853m Dec 22), 156.00($1.29b Dec 23) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 98 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

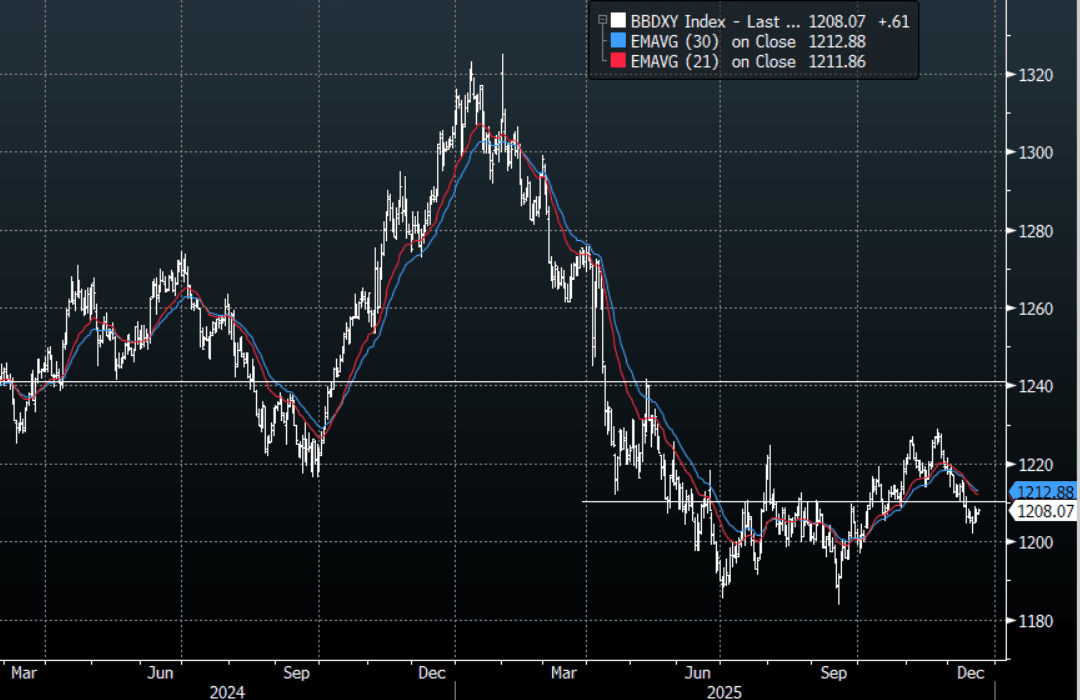

FOREX: USD - BBDXY Treading Water

The BBDXY has had a range today of 1206.94 - 1208.33 in the Asia-Pac session; it is currently trading around {BBDXY Index}. The USD continues to chop around without really going anywhere, trading a little higher after the BOJ hiked rates. On the day I still have very little conviction on direction, look for initial resistance again back towards the 1209-1210 area and above here the more important 1213-1216 area where sellers should remerge initially. Can this 1204 area continue to provide support if not a move below here would target 1198-1200.

- EUR/USD - Asian range 1.1717-1.1729, Asia is currently trading {EURUSD Curncy}. The pair continues to consolidate above 1.1700. On the day, support remains toward 1.1675-1700 initially, a break below here could potentially signal a deeper pullback. While this support hold it is skewed towards testing higher

- GBP/USD - Asian range 1.3374-1.3387, Asia is currently dealing around {GBPUSD Curncy}. The pair has once again rejected a move toward 1.3450 and is potentially starting to show the first signs of exhaustion. On the day, continue to watch for selling pressure above 1.3400, if this area continues to hold, look for a pullback to the more important 1.3250/1.3300 area. I continue to watch for signs of GBP potentially topping out, are we seeing the first signs ?.

- Cross asset : SPX +0.10%, Gold $4320, US 10-Year 4.14%, BBDXY 1208, Crude Oil $56.00

- Data/Events : EZ ECB Current Account/Consumer Confidence, France PPI/Retail Sales SA, Germany PPI/GfK Consumer Confidence, Italy Current Account Balance/Industrial Sales

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

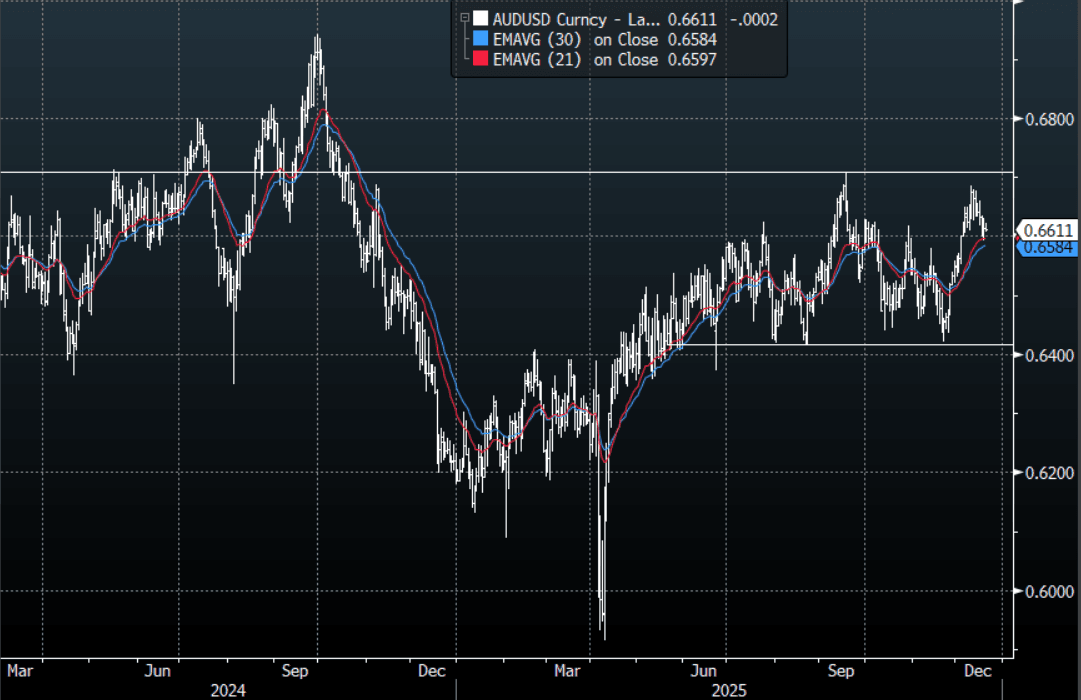

AUD/USD - Continues To Hold Above 0.6600

The AUD/USD has had a range today of 0.6608 - 0.6622 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The AUD continues to consolidate above 0.6600. The AUD price action for the moment remains consolidative, but I do remain wary of what seems to be happening in US stocks, let's see if this bounce can extend from here. Technically while the AUD remains above 0.6500-0.6550 dips should continue to be supported. In the Asian session, watch to see if this 0.6590-0.6600 area can continue to hold, if not we could see a deeper pullback towards the 0.6500-50 support. On the day I suspect a break back above 0.6635 area could see the AUD target the 0.6660-80 resistance.

- MNI AU - The AU-US 10yr spread is around +60bps, so holding the bulk of its gains since late Nov, when this spread broke higher. The bias is likely to remain for higher spreads in AU's favor given the relative central bank outlooks into the first part of 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6675(AUD1.31b), 0.6700(AUD1.57b). Upcoming Close Strikes : 0.6475(AUD599m Dec 23), 0.6550(AUD629m Dec 22), 0.6600(AUD557m Dec 23) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

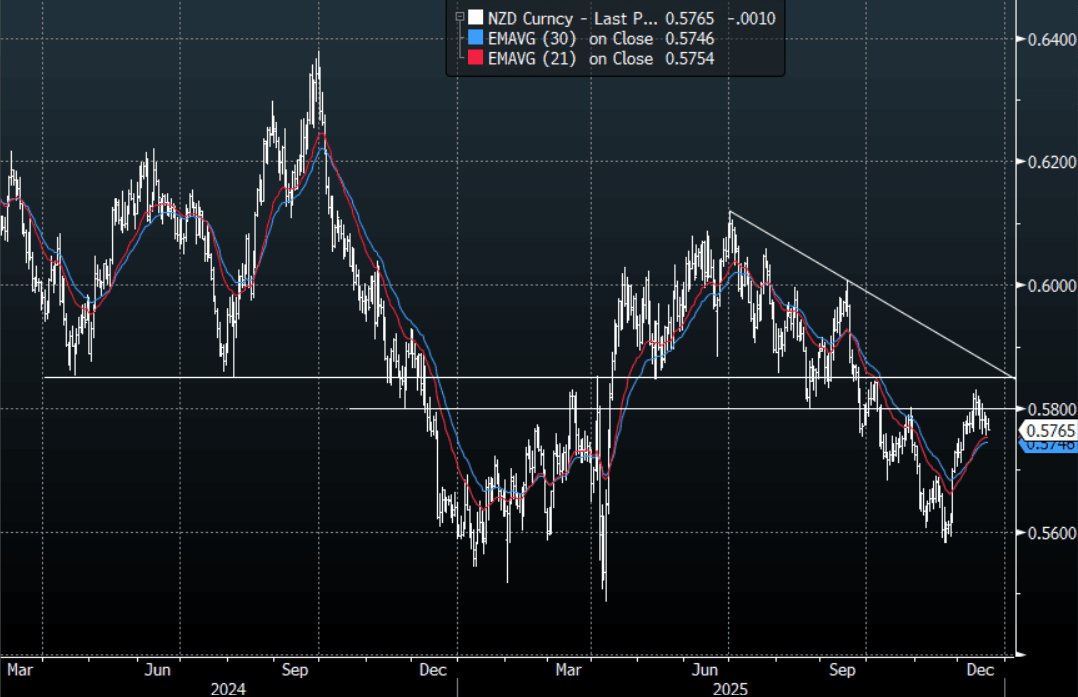

NZD/USD - A Little Softer Within Its Range

The NZD/USD had a range today of 0.5763-0.5783 in the Asia-Pac session, it is currently trading around {NZD Curncy}. The NZD is trading a little lower within its recent range. The NZD is consolidating its gains above 0.5700-0.5750 and for the most part has been left unscathed by the choppy price action seen elsewhere. On the day, I suspect more of the same, support is back toward 0.5740-0.5760 and resistance is around 0.5810-30.

- MNI AU - ANZ Business Confidence & Activity To Fresh Cycle Highs : ANZ's business confidence and activity measures for New Zealand rose strongly in Dec. Activity is at 60.9 from 53.1 prior, while confidence is up to 73.6, from 67.1 in Nov. These are cycle high readings for both indices and points to growing optimism around the economic outlook.

- MNI AU - ANZ Consumer Sentiment Recovers Further, Supporting Spend Outlook: The ANZ New Zealand consumer confidence measure rose to 101.5 in Dec, a 3.2% (after gaining 6.5% in Nov). This puts the index at its highest levels since the second half of 2021.The rise in sentiment is pointing to further improvement in the spending backdrop and comes after the rise in the Q4 Westpac consumer sentiment reading earlier this week (although this measure remains sub 100).

- "ANZ BANK NOW SEES FONTERRA 2025-26 MILK PRICE AT NZ$8.90/KG" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5630(NZD594m), 0.5750(NZD459m), 0.5875(NZD410m). Upcoming Close Strikes : 0.5530(NZD475m Dec 23), 0.5780(NZD324m Dec 22) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 38 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

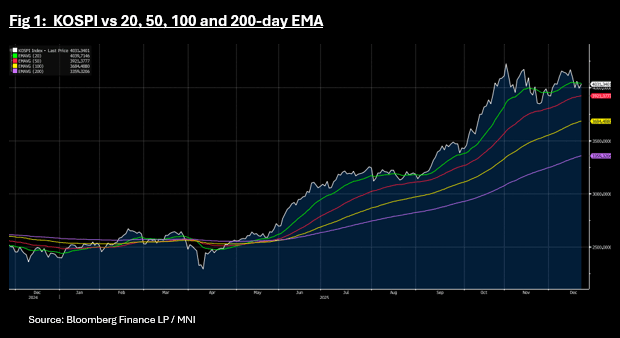

ASIA STOCKS: Tech Rebound Provides Friday Boost

All eyes were on the BOJ today as 10-Yr JGB yields headed north of 2% and the Yen remains pressured. Whilst the hike was expected it was the outlook that investors focused on with the BOJ indicating that it will continue to raise the policy interest rate and adjust the degree of monetary accommodation if the outlook for economic activity and prices presented in the October Outlook Report is realized. It seems that the BOJ may be overlooked and the weaker US CPI overnight the greater influence as equities rallied for many major bourses to finish the week, on hopes that a US rate cut could come sooner than what is currently priced in. Strong guidance from major chipmakers like Micron Technology in the US gave tech stocks a boost today also with some names up over 5% Friday.

- The NIKKEI delivered strong gains today thanks in part to names like SOFTBANK Group up +6.5% as a tech stock rebound supported prices. The NIKKEI has had a volatile week but remains down -2.7% for the week as it nears 50,000 again.

- The KOSPI is up +0.80% today and down -3.3%% despite SK Hynix +2.7% today alone. Today's gains to 4,030 take the KOSPI back near to the 20-day EMA of 4,039.

- China's major bourses are finishing strongly Friday, yet remain on track for weekly falls. The Hang Seng is up +0.65%, whilst down -1.20% for the week. The CSI 300 is up +0.61%, and flat for the week. Shanghai up today +0.59% and down +0.3% for the week and Shenzhen up +1.13% and down -0.15% for the week.

- The NIFTY 50 has fallen for the first four trading days this week as profit takers emerge. Up +0.45% in Friday trade, the NIFTY 50 remains down -0.40% for the week as it attempts to consolidate below 26,000 at 25,940.

- The Jakarta Composite had had a strong week until Friday, with falls of -0.55% and is down over 1% this week.

- The FTSE Malay KLCI is up Friday by +0.72% reaching a new high of 1,658.80 and a weekly gain of 1.2%.

OIL: Supply Concerns Override Geopolitical Tensions

- Oil prices rose again in Asia today, only days after the US upped the ante on Venezuela and the US President threatening them.

- WTI is up +0.23% in the Asia trading day to US$56.03 bbl yet remains down over 2.6% for the week.

- Brent is flat today at US$59.73 as it attempts to hold below US$60 bbl, a key technical resistance. For the week, Brent is down over -2.4% and near to oversold on the 14 day relative strength index.

- WTI remains below all major moving averages, where it has been for most of December as ongoing concerns of a 2026 supply glut, drag prices lower.

- OPEC+ production increases this year and into next have been greater than expected, whilst global demand has been tepid. The overall trend remains lower and geopolitical impacts for now appear short lived in their impact.

- Oil major Chevron Corp. is preparing to export 1 million barrels of crude from Venezuela, a day after President Donald Trump accused the nation of using oil proceeds to finance drug trafficking and terrorism. Chevron, which holds a US license to drill and export oil from the country ships are not subject to sanctions

- The UK government imposed sanctions on three smaller Russian oil producers, as a US-brokered peace deal between Moscow and Kyiv remains elusive. (per BBG)

- The European Council imposes restrictive measures on additional 41 vessels, which it says are part of Russia's 'shadow fleet' of oil tankers, according to a statement.

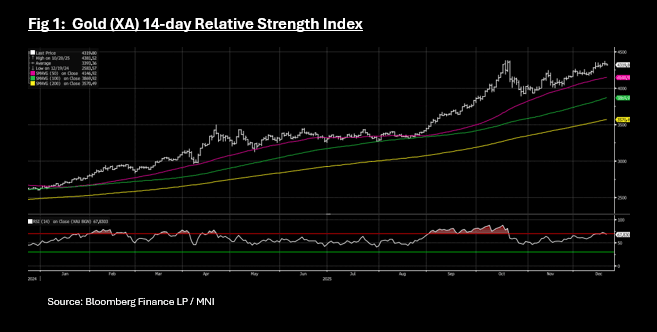

Gold Set for Weekly Gains, Back Below Overbought on RSI

- Gold had one eye on the key US data release Thursday as its next catalyst. The US Consumer Price Index (CPI) and core CPI for November both eased more than forecasted, strengthening market expectations that the Federal Reserve will begin cutting interest rates sooner, potentially as early as January or April 2026. Lower interest rates reduce the opportunity cost of holding non-interest-bearing assets like gold, increasing its appeal. Gold had jumped higher on the CPI release, yet moderated into the close of the US trading day Thursday and that weakness continued on today as profit takers took over.

- Gold is down -0.3% today at US$4,318.95 but up +0.45% for the week.

- Ongoing global instability, including heightened tensions between the US and Venezuela and the war in Ukraine, should keep gold well bid as a safe-haven asset, strong structural demand from central banks looking to diversify their reserves away from the US dollar, combined with robust inflows into gold-backed Exchange Traded Funds (ETFs), provided a solid floor for prices and absorbed selling pressure

- Gold has moderated just below overbought on the 14-day relative strength index with today's falls and with the momentum clearly weak, could moderate further.

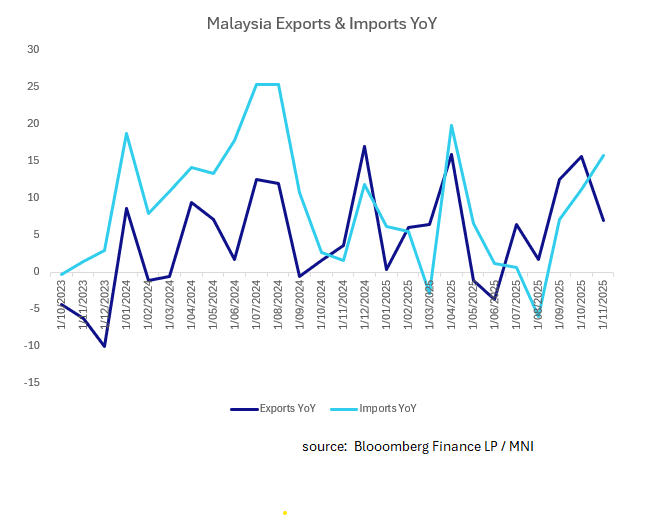

MALAYSIA: Exports Miss Forecasts, Imports Strong

- Despite missing forecasts Malaysia's exports remain strong, supporting the SE Asian nations' growth outlook into 2026.

- Exports rose 7.0% YoY in November, down from 15.7% in October. Against an estimate of +11.6%, the result may look like a miss but they remain firmly above the 3-Yr average for Malaysia goods shipped, underscoring the resilience of the economy.

- Imports were surprisingly strong which for some market commentators suggests a strong domestic demand outlook. Imports rose +15.8% from 10% the month prior.

- The trade surplus narrowed to MYR 6.1bn, missing estimates of MYR17.7bn

- The BNM finished the year with a neutral outlook and is widely expected to stay on hold throughout 2026.

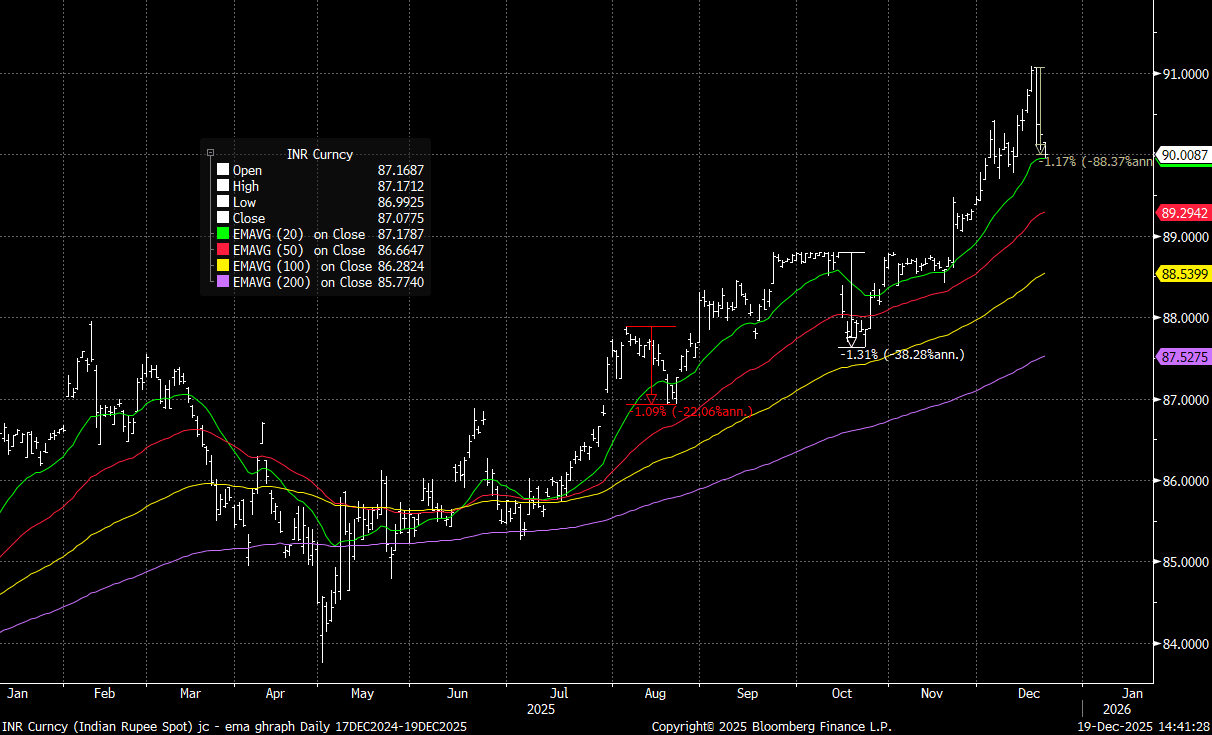

INR: USD/INR Challenging 20-day EMA Support, As Pullback Continues

The USD/INR spot pull back has extended, with earlier lows of 89.95 in the first part of Friday dealings. This is around the 20-day EMA support point. We haven't been able to break lower yet, with the pair last around 90.00. A clean break lower could see the 50-day EMA support at 89.29 targeted. The rupee is still up around 0.45% so far this week (the third best performer in EM Asia FX after PHP and THB), as the RBI drew a short term line in the sand around the 91.00 region.

- This pull back is broadly in line with what we saw in both Aug and Oct earlier this year (in terms of peak to trough moves). These episodes are highlighted on the chart below.

- We could see some USD demand emerge, but given the more elevated levels of USD/INR and greater effective exchange rate adjustment that has taken place since then, the market still may be wary of RBI intervention.

- Despite stabilization in spot, 1 mth NDF points remain elevated last near +40, which is fresh highs back to the first part of 2022. The 1month USD/INR NDF outright was last near 90.40/45. 1 month implied vols are edging higher but at 4.49%, remain well within 2025 ranges, the risk reversal is tracking lower, but is still above positive territory at this stage.

- We have seen modestly positive net equity inflows so far this week, with some FX stability likely helping at the margins. Local equity indices have also stabilized remain off recent cycle highs.

- Later we get FX reserves for the week ending Dec 12.

Fig 1: USD/INR Spot Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

ASIA FX: USD/CNH Steady, USD/KRW Still Near 1480, TWD Down This Week Outflows

In North East Asia FX, USD/CNH has edged a little higher, last just above 7.0350. USD/CNY onshore spot remains above 7.0400, which is likely keeping some support in place for USD/CNH. Later on, we get FX settlement data for Nov, which will be eyed, as the market focus remains on conversion back into the local currency as a source of yuan gains as we approach year end and ahead of the China new year in 2026.

- USD/KRW is higher, but hasn't re-captured the1480 yet (last 1478/79). Focus remains on efforts to stabilize/improve the won outlook. South Korean President Lee stating this afternoon that local equity markets are still undervalued and that distrust of local stocks is impacting FX markets as well (presumably through the outflow channel of local funds to overseas stocks). Focus remains on boosting capital inflows (to aid USD liquidity), while meetings have also taken place with top exporters (with greater conversion back into won likely to be encouraged).

- The market may remain wary of fresh USD longs at these levels in USD/KRW, given liquidity will start to reduce ahead of year end.

- Spot USD/TWD is up a little so far today, last close to 31.55. We are short of recent highs but remain above all key EMAs (20-day near 31.335). TWD has been the worst performer in EM Asia FX over the past week, down close to 1.2%. The equity outflow story (-$5.6bn up to Thursday of this week) has been a headwind. Even with potential inflows today (as local stocks recover some ground, Taiex up 0.90%), it has been enough to aid a firmer TWD backdrop.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 19/12/2025 | 0700/0700 | *** | Public Sector Finances | |

| 19/12/2025 | 0700/0800 | ** | PPI | |

| 19/12/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 19/12/2025 | 0700/0800 | ** | Retail Sales | |

| 19/12/2025 | 0700/0700 | *** | Retail Sales | |

| 19/12/2025 | 0745/0845 | ** | PPI | |

| 19/12/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 19/12/2025 | 0830/0930 | ECB Wage Tracker | ||

| 19/12/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/12/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 19/12/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 19/12/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 19/12/2025 | 1200/1300 | ECB Cipollone Remarks, Roundtable at Aspen Institute | ||

| 19/12/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 19/12/2025 | 1330/0830 | ** | Retail Trade | |

| 19/12/2025 | 1400/1500 | ** | BNB Business Confidence | |

| 19/12/2025 | 1500/1000 | *** | NAR existing home sales | |

| 19/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 19/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 19/12/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 19/12/2025 | 1510/1610 | ECB Lane Lecture at Central Bank of Ireland | ||

| 19/12/2025 | 1630/1630 | BOE to announce APF Q4 Sales Schedule | ||

| 19/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly |