ASIA FX: USD/CNH Steady, USD/KRW Still Near 1480, TWD Down This Week Outflows

In North East Asia FX, USD/CNH has edged a little higher, last just above 7.0350. USD/CNY onshore spot remains above 7.0400, which is likely keeping some support in place for USD/CNH. Later on, we get FX settlement data for Nov, which will be eyed, as the market focus remains on conversion back into the local currency as a source of yuan gains as we approach year end and ahead of the China new year in 2026.

- USD/KRW is higher, but hasn't re-captured the1480 yet (last 1478/79). Focus remains on efforts to stabilize/improve the won outlook. South Korean President Lee stating this afternoon that local equity markets are still undervalued and that distrust of local stocks is impacting FX markets as well (presumably through the outflow channel of local funds to overseas stocks). Focus remains on boosting capital inflows (to aid USD liquidity), while meetings have also taken place with top exporters (with greater conversion back into won likely to be encouraged).

- The market may remain wary of fresh USD longs at these levels in USD/KRW, given liquidity will start to reduce ahead of year end.

- Spot USD/TWD is up a little so far today, last close to 31.55. We are short of recent highs but remain above all key EMAs (20-day near 31.335). TWD has been the worst performer in EM Asia FX over the past week, down close to 1.2%. The equity outflow story (-$5.6bn up to Thursday of this week) has been a headwind. Even with potential inflows today (as local stocks recover some ground, Taiex up 0.90%), it has been enough to aid a firmer TWD backdrop.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: 10-Yr Future Nears Key Tech Level on Moderate Gains

Cash did very little in the Asia trading day with yield moves across the curve muted. Bond futures were mostly up with the 10-Yr (TYZ5) up +02 to 112-27+, the 20-day EMA. It opened the day near the 50-day EMA and the modest gains consolidated a move above the 50-day and will now look onto the European open for any follow on.

- The 2-Yr is down -0.4bps to 3.57%.

- The 5-Yr is flat at 3.686%

- The 10-Yr is at 4.115%, flat on the day.

- The 30-Yr yield was up +0.3bps at 4.737%

Tonight for new issuance is 17-week bills and a 20-Yr US$16bn auction. The bid to cover for the last 20-Yr was 2.73x.

Key focus tonight will be the FOMC minutes. Please see here our preview here: https://media.marketnews.com/Fed_Minutes_Preview_Nov2025_2e5fc3ae40.pdf

ASIA STOCKS: Major Bourses Moderate Ahead of Nvidia

Equity markets appeared cautious today with expectations remaining elevated for Nvidia's earnings report out tomorrow. With some of Asia's tech stocks up over 100% since April, Nvidia's results could possibly provide an insight into the next direction for tech stocks. Key stocks in Korea like SK Hynix are up +230% from April lows, Samsung +90% of YTD lows and Taiwan's TSMC +78%. With profit taking suggested as the likely driver for the pull back in recent days for Asia tech stocks, it makes Nvidia's results all that more in focus. Additionally a key tailwind for Asia equities is a US rate cut and with growing uncertainty over the FED's next move, this is feeding into the profit taking. Sentiment has not turned negative, more that the positive momentum has moderated as record highs in some bourses and key stocks were hit.

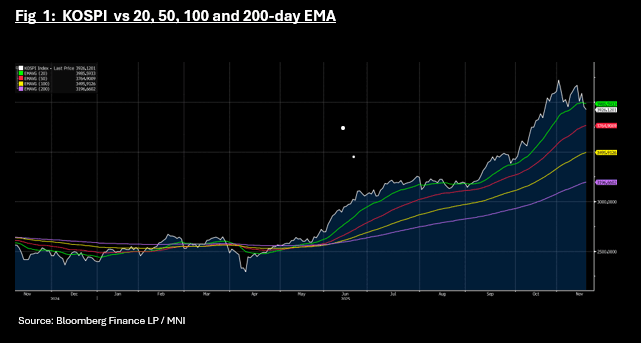

- The NIKKEI and the KOSPI have been at the centre of the tech rally and with the NIKKEI around where it started the day, it was the KOSPI that took centre stage with a fall of -0.65%. The KOSPI has moved below the 20-day EMA for the first time since the beginning of September. At 3,925, the next key technical below is the 50-day EMA of 3,764.

- In China a mixed bag with the CSI 300 up +0.20% whilst the HSI fell -0.45%, Shanghai flat and Shenzhen down -0.84%. The gains in the CSI 300 weren't fueled by tech, rather raw materials, shipping, mining and petrochem which could indicate a re-allocation out of tech into more broader sectors.

- In SE Asia the Jakarta Comp is up +0.63%, the FSTE Malay KLCI is up +0.40% whilst the SE Thai is down moderately.

- India's NIFTY 50 has had a subdued opening with little movement , consistent with its 5-day performance. Like the currency the NIFTY 50's next phase appears to be waiting on the outcome of trade talks with onshore media suggesting an initial agreement close.

OIL: Oil Down Following US Ukraine Peace Plan News, EIA US Inventories Out Later

Oil prices fell following an Axios report that the US has put together a new 28 point Ukraine peace plan after closed US-Russia discussions. It has been presented to the Ukrainians. Crude is now off that low but remains down on the day with WTI -0.3% to $60.57/bbl after falling to $60.39 and Brent -0.3% to $64.66/bbl following a low of $64.51. They have been trading in a narrow range ahead of EIA data out later and Thursday’s September US payrolls. The USD index is slightly higher.

- The Axios report is based on comments from both US and Russian officials and includes plans for peace, security guarantees for Ukraine and Europe, and the prospect for US relations with Russia & Ukraine. However, details have not been revealed including on contentious issues such as territory, international peacekeepers in Ukraine, Zelenskyy-Putin meeting and a ceasefire before negotiations begin. Given failed previous attempts, a deal is still a long way off.

- US/EU sanctions against Russian majors Rosneft and Lukoil come into effect on Friday and there are already signs of refiners looking to alternative sources.

- Bloomberg reported that there was a US crude inventory build of 4.4mn barrels last week after an increase the week before, according to those familiar with the API data. Product stocks were higher too. The official EIA data is out Wednesday and has shown product drawdowns since the start of October.

- Later the Fed’s Logan, Miran, Barkin and Williams speak and the October FOMC minutes are published. Delayed August US trade prints as well as UK October CPI/PPI and euro area October CPI.