ASIA STOCKS: Tech Rebound Provides Friday Boost

All eyes were on the BOJ today as 10-Yr JGB yields headed north of 2% and the Yen remains pressured. Whilst the hike was expected it was the outlook that investors focused on with the BOJ indicating that it will continue to raise the policy interest rate and adjust the degree of monetary accommodation if the outlook for economic activity and prices presented in the October Outlook Report is realized. It seems that the BOJ may be overlooked and the weaker US CPI overnight the greater influence as equities rallied for many major bourses to finish the week, on hopes that a US rate cut could come sooner than what is currently priced in. Strong guidance from major chipmakers like Micron Technology in the US gave tech stocks a boost today also with some names up over 5% Friday.

- The NIKKEI delivered strong gains today thanks in part to names like SOFTBANK Group up +6.5% as a tech stock rebound supported prices. The NIKKEI has had a volatile week but remains down -2.7% for the week as it nears 50,000 again.

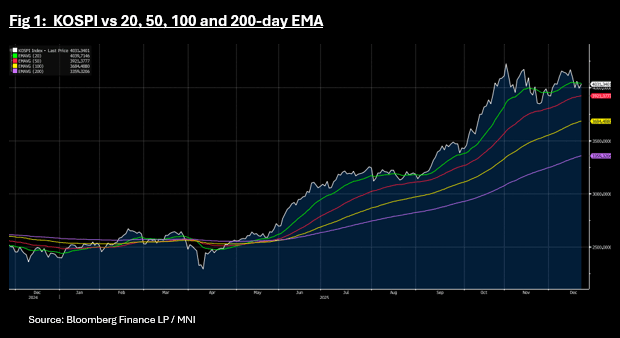

- The KOSPI is up +0.80% today and down -3.3%% despite SK Hynix +2.7% today alone. Today's gains to 4,030 take the KOSPI back near to the 20-day EMA of 4,039.

- China's major bourses are finishing strongly Friday, yet remain on track for weekly falls. The Hang Seng is up +0.65%, whilst down -1.20% for the week. The CSI 300 is up +0.61%, and flat for the week. Shanghai up today +0.59% and down +0.3% for the week and Shenzhen up +1.13% and down -0.15% for the week.

- The NIFTY 50 has fallen for the first four trading days this week as profit takers emerge. Up +0.45% in Friday trade, the NIFTY 50 remains down -0.40% for the week as it attempts to consolidate below 26,000 at 25,940.

- The Jakarta Composite had had a strong week until Friday, with falls of -0.55% and is down over 1% this week.

- The FTSE Malay KLCI is up Friday by +0.72% reaching a new high of 1,658.80 and a weekly gain of 1.2%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Major Bourses Moderate Ahead of Nvidia

Equity markets appeared cautious today with expectations remaining elevated for Nvidia's earnings report out tomorrow. With some of Asia's tech stocks up over 100% since April, Nvidia's results could possibly provide an insight into the next direction for tech stocks. Key stocks in Korea like SK Hynix are up +230% from April lows, Samsung +90% of YTD lows and Taiwan's TSMC +78%. With profit taking suggested as the likely driver for the pull back in recent days for Asia tech stocks, it makes Nvidia's results all that more in focus. Additionally a key tailwind for Asia equities is a US rate cut and with growing uncertainty over the FED's next move, this is feeding into the profit taking. Sentiment has not turned negative, more that the positive momentum has moderated as record highs in some bourses and key stocks were hit.

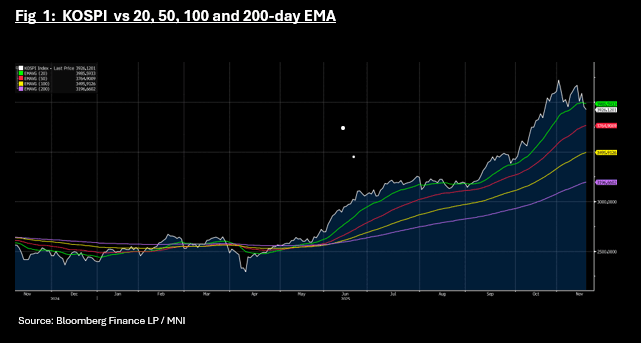

- The NIKKEI and the KOSPI have been at the centre of the tech rally and with the NIKKEI around where it started the day, it was the KOSPI that took centre stage with a fall of -0.65%. The KOSPI has moved below the 20-day EMA for the first time since the beginning of September. At 3,925, the next key technical below is the 50-day EMA of 3,764.

- In China a mixed bag with the CSI 300 up +0.20% whilst the HSI fell -0.45%, Shanghai flat and Shenzhen down -0.84%. The gains in the CSI 300 weren't fueled by tech, rather raw materials, shipping, mining and petrochem which could indicate a re-allocation out of tech into more broader sectors.

- In SE Asia the Jakarta Comp is up +0.63%, the FSTE Malay KLCI is up +0.40% whilst the SE Thai is down moderately.

- India's NIFTY 50 has had a subdued opening with little movement , consistent with its 5-day performance. Like the currency the NIFTY 50's next phase appears to be waiting on the outcome of trade talks with onshore media suggesting an initial agreement close.

OIL: Oil Down Following US Ukraine Peace Plan News, EIA US Inventories Out Later

Oil prices fell following an Axios report that the US has put together a new 28 point Ukraine peace plan after closed US-Russia discussions. It has been presented to the Ukrainians. Crude is now off that low but remains down on the day with WTI -0.3% to $60.57/bbl after falling to $60.39 and Brent -0.3% to $64.66/bbl following a low of $64.51. They have been trading in a narrow range ahead of EIA data out later and Thursday’s September US payrolls. The USD index is slightly higher.

- The Axios report is based on comments from both US and Russian officials and includes plans for peace, security guarantees for Ukraine and Europe, and the prospect for US relations with Russia & Ukraine. However, details have not been revealed including on contentious issues such as territory, international peacekeepers in Ukraine, Zelenskyy-Putin meeting and a ceasefire before negotiations begin. Given failed previous attempts, a deal is still a long way off.

- US/EU sanctions against Russian majors Rosneft and Lukoil come into effect on Friday and there are already signs of refiners looking to alternative sources.

- Bloomberg reported that there was a US crude inventory build of 4.4mn barrels last week after an increase the week before, according to those familiar with the API data. Product stocks were higher too. The official EIA data is out Wednesday and has shown product drawdowns since the start of October.

- Later the Fed’s Logan, Miran, Barkin and Williams speak and the October FOMC minutes are published. Delayed August US trade prints as well as UK October CPI/PPI and euro area October CPI.

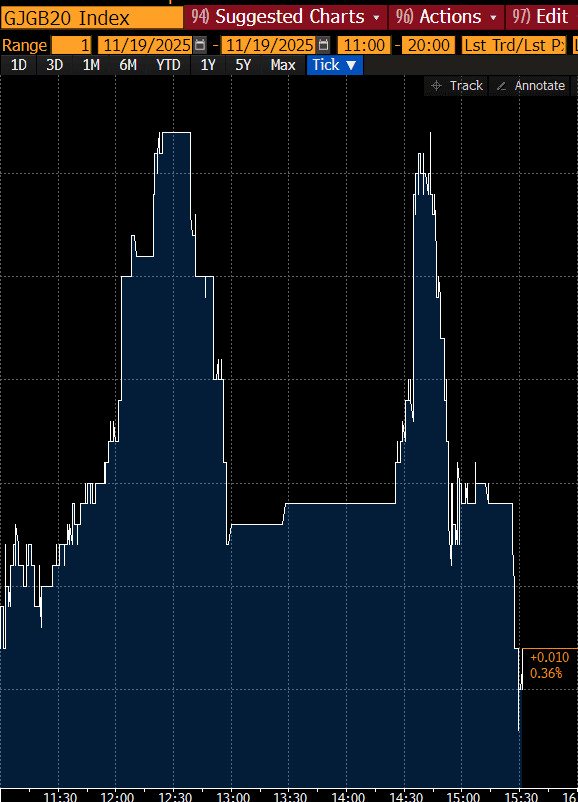

JGBS: Yields Highs Reversed Despite Lacklustre Demand At 20Y Auction

JGB futures are weaker, -10 compared to settlement levels, but well above the morning’s low.

- This came despite today’s 20-year JGB auction delivering weak results across key metrics. The low-price underperformed dealer forecasts, which were set at 98.60 according to a Bloomberg poll. Moreover, the cover ratio dropped to 3.2825x from 3.5599x in the previous outing, and the auction tail lengthened sharply to 0.31 from 0.10.

- BoJ Governor Ueda will meet with Japan FinMin Katayama and Economy Minister Kiuchi later today. The meeting is expected to take place at 6:10pm Tokyo time. This meeting also comes amid renewed speculation around Japan's fiscal outlook. The Kyodo news agency reported on Wednesday that Japan's stimulus package could exceed 20 trillion yen.

- Cash US tsys are little changed in today's Asia-Pac session ahead of Nvidia's earnings, which are due after the market close on Wednesday.

- Cash JGBs are flat to 1bp cheaper across benchmarks. The benchmark 20-year yield is 1.0bp higher at 2.797% after setting a fresh cycle high of 2.822% today. (see chart)

- Swap rates are 1bp higher to 3bps lower, with a flattening bias.

- Tomorrow, the local calendar will see Weekly International Investment Flow and Tokyo Condominiums for Sale data alongside a speech in Niigata from BOJ Board Koeda.

Source: Bloomberg Finance LP