OIL: Supply Concerns Override Geopolitical Tensions

- Oil prices rose again in Asia today, only days after the US upped the ante on Venezuela and the US President threatening them.

- WTI is up +0.23% in the Asia trading day to US$56.03 bbl yet remains down over 2.6% for the week.

- Brent is flat today at US$59.73 as it attempts to hold below US$60 bbl, a key technical resistance. For the week, Brent is down over -2.4% and near to oversold on the 14 day relative strength index.

- WTI remains below all major moving averages, where it has been for most of December as ongoing concerns of a 2026 supply glut, drag prices lower.

- OPEC+ production increases this year and into next have been greater than expected, whilst global demand has been tepid. The overall trend remains lower and geopolitical impacts for now appear short lived in their impact.

- Oil major Chevron Corp. is preparing to export 1 million barrels of crude from Venezuela, a day after President Donald Trump accused the nation of using oil proceeds to finance drug trafficking and terrorism. Chevron, which holds a US license to drill and export oil from the country ships are not subject to sanctions

- The UK government imposed sanctions on three smaller Russian oil producers, as a US-brokered peace deal between Moscow and Kyiv remains elusive. (per BBG)

- The European Council imposes restrictive measures on additional 41 vessels, which it says are part of Russia's 'shadow fleet' of oil tankers, according to a statement.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

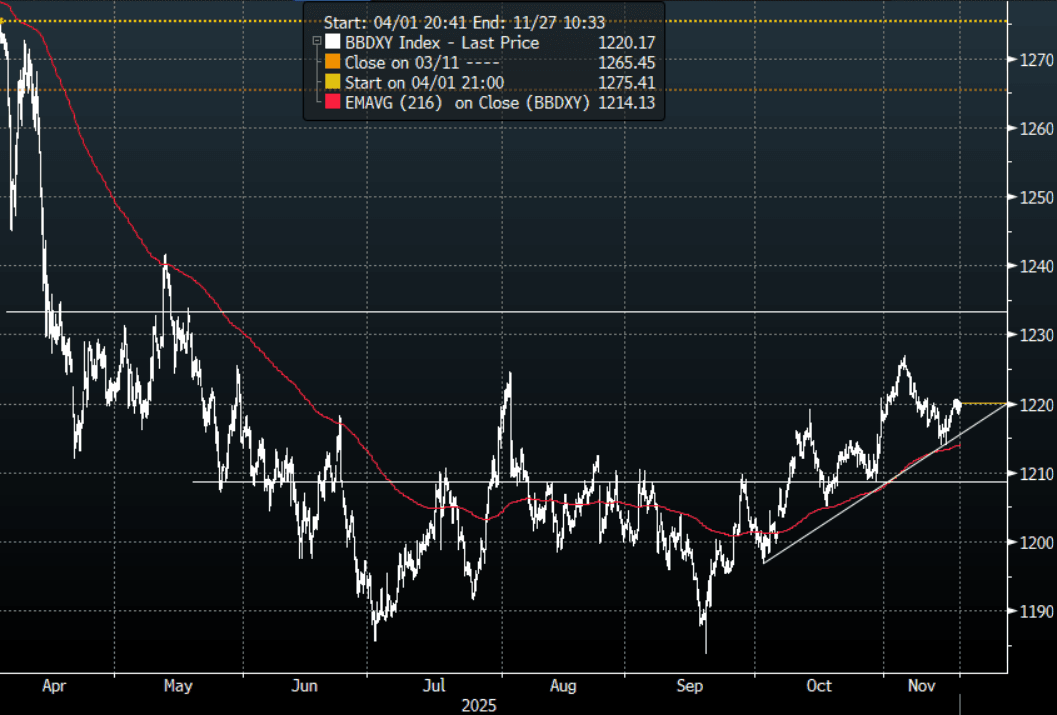

FOREX: Asia-Pac USD: BBDXY Edges Higher

The BBDXY has had a range today of 1219.30 - 1220.37 in the Asia-Pac session; it is currently trading around 1220, +0.10%. The USD trades sideways after consolidating its recent gains as risk tries to steady itself ahead of the Nvidia results. I continue to watch for signs of a base forming from which to move higher again if risk stays under pressure. On the day it looks like the short-term range is 1217-1222, above 1222 and it could look to rebuild momentum for a test of the 1230-35 area. Support remains in the 1210-1215 area.

- EUR/USD - Asian range 1.1573 - 1.1585, Asia is currently trading 1.1580. The pair stalled and moved lower after finding some decent resistance toward the 1.1650-1.1700 area. This has been the pivot within the larger 1.1400-1.1900 range over the past few months. On the day while the 1.1615-30 area continues to cap I would be skewed to fade bounces, above there and we could again challenge the pivot toward 1.1700.

- GBP/USD - Asian range 1.3129 - 1.3153, Asia is currently dealing around 1.3135. I continue to favor fading rallies, as GBP looks to have put in a medium term top. A sustained move back below 1.3080-1.3100 support would see the momentum lower reinstated and focus turn back toward the 1.3000 area. Suspect rallies back toward the 1.3250-1.3300 will be sold into if we see a bounce.

- Cross asset : SPX -0.15%, Gold $4070, US 10-Year 4.115%, BBDXY 1220, Crude Oil $60.60

- Data/Events : EZ ECB Current Account SA/CPI, Germany Current Account Balance, Italy Current Account Balance

Fig 1: BBDXY Spot 4H Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Gold Range Trading As Watching & Waiting, US Trade & FOMC Minutes Later

Gold has range traded today as the market waits for further US data releases to gauge the outlook for the economy and therefore Fed policy. The focus will be on Thursday’s September payroll report. Bullion is 0.2% higher at $4075.0/oz after a low of $4055.68 followed by a peak of $4080.71, below resistance at $4106.7, with the US dollar slightly higher and yields steady. Risk appetite is weaker though with equities down and nerves ahead of today’s Nvidia’s earnings report. Risk off moves can be either positive or negative for gold.

- With limited data, Fed speakers have been cautious regarding their thoughts for the 10 December meeting. As a result, the market has around a 50% chance of a cut priced in but that could easily change as more delayed data are released. In addition, the October 29 minutes may give some clarity on Fed thinking. It cut rates 25bp at this meeting.

- Silver is up 0.4% to $50.90 off the intraday high of $51.279 and holding between support at $49.363 and resistance/bull trigger at $54.480.

- Equities are mixed with the S&P e-mini down 0.1% and Hang Seng -0.5% but CSI 300 up 0.2% and Topix +0.1%. Oil prices are lower with WTI -0.3% to $60.55/bbl. Copper is flat.

- Later the Fed’s Logan, Miran, Barkin and Williams speak and the October FOMC minutes are published. Delayed August US trade prints as well as UK October CPI/PPI and euro area October CPI.

AUSSIE BONDS: Modestly Richer, WPI Unlikely To Change rates Outlook

ACGBs (YM +1.0 & XM +2.5) are slightly richer after the release of Q3 Wage Price data.

- Q3 wages rose 0.8% q/q to be 3.4% higher on a year ago, in line with Q2 and Bloomberg consensus, signalling a stabilisation consistent with SEEK advertised salary data. In November, the RBA forecast 3.4% y/y for Q4 2025 before moderating to 3% by end 2026. Thus, the Q3 WPI data don’t change the outlook for monetary policy, with rates likely on hold towards at least mid-2026 as it monitors price and capacity pressures.

- Cash US tsys are little changed in today's Asia-Pac session ahead of Nvidia's earnings, which are due after the market close on Wednesday.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +30bps.

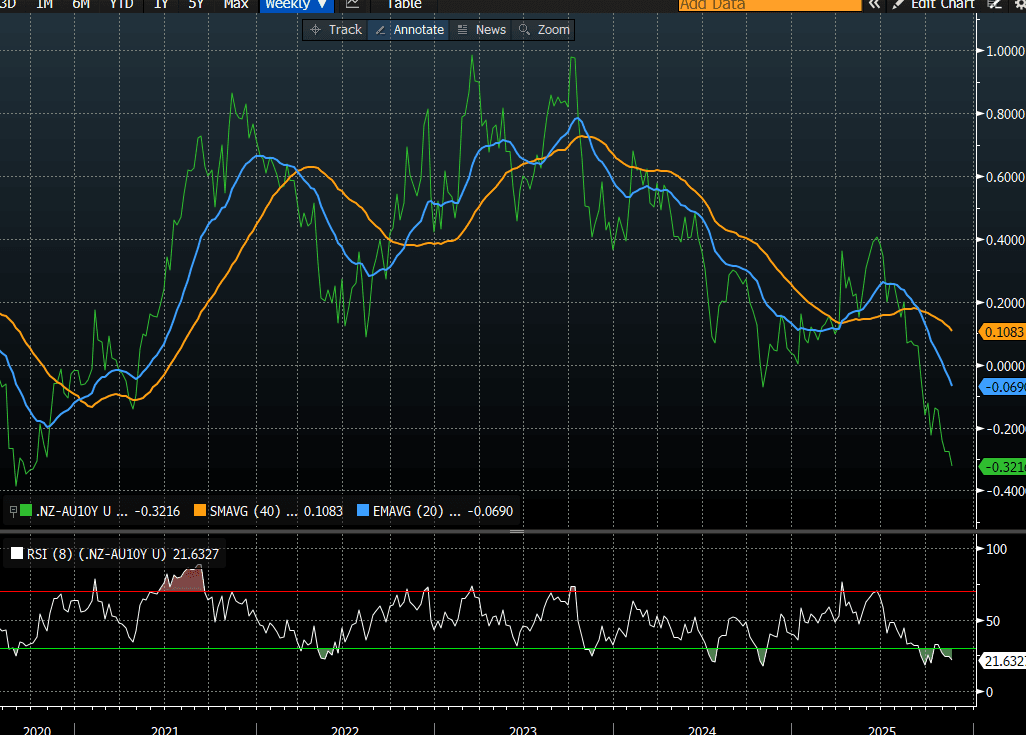

- The NZ-AU 10-year yield differential is 4bp narrower at -32bps, the lowest since 2020. (see chart)

- The bills strip is little changed.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 14bps of easing priced by mid-2026.

Bloomberg Finance LP