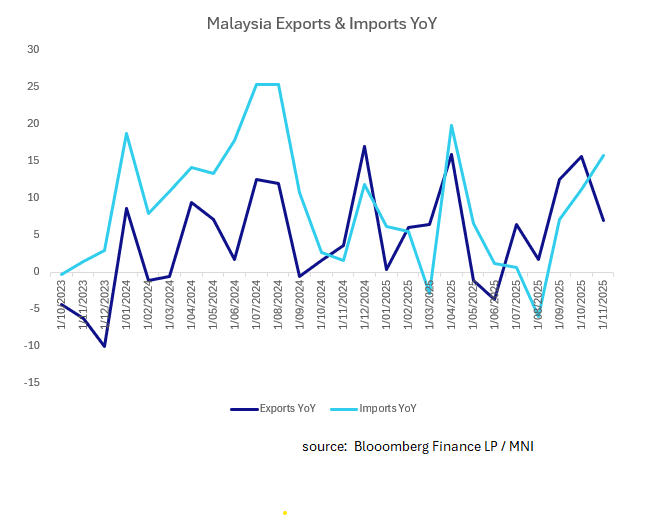

MALAYSIA: Exports Miss Forecasts, Imports Strong

- Despite missing forecasts Malaysia's exports remain strong, supporting the SE Asian nations' growth outlook into 2026.

- Exports rose 7.0% YoY in November, down from 15.7% in October. Against an estimate of +11.6%, the result may look like a miss but they remain firmly above the 3-Yr average for Malaysia goods shipped, underscoring the resilience of the economy.

- Imports were surprisingly strong which for some market commentators suggests a strong domestic demand outlook. Imports rose +15.8% from 10% the month prior.

- The trade surplus narrowed to MYR 6.1bn, missing estimates of MYR17.7bn

- The BNM finished the year with a neutral outlook and is widely expected to stay on hold throughout 2026.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

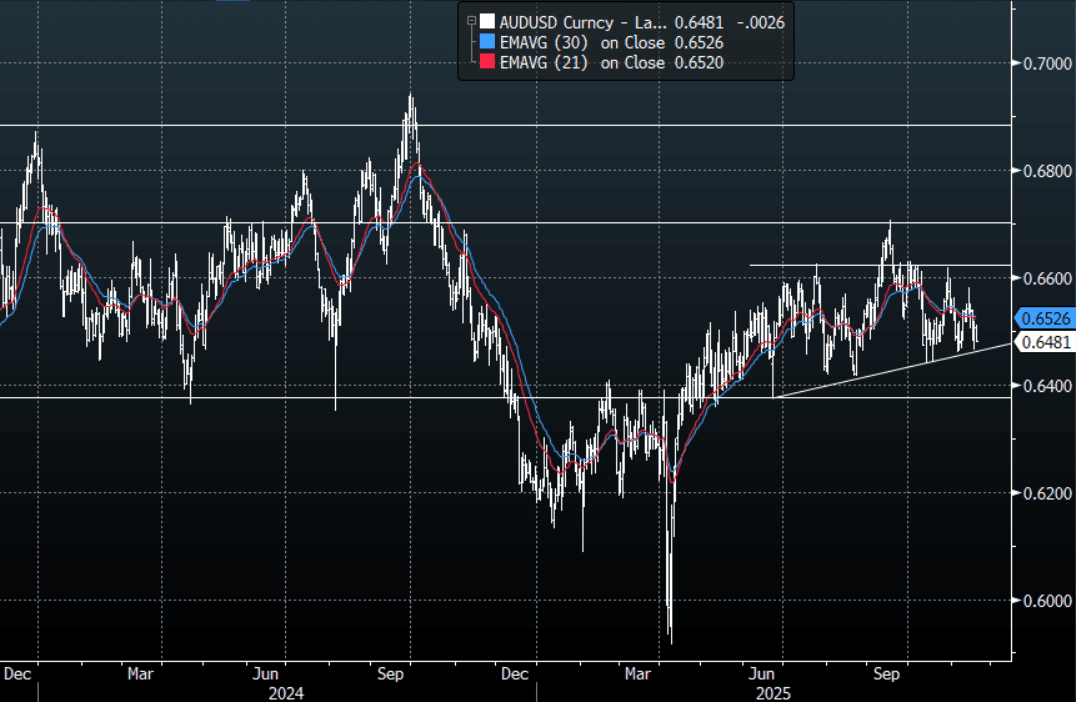

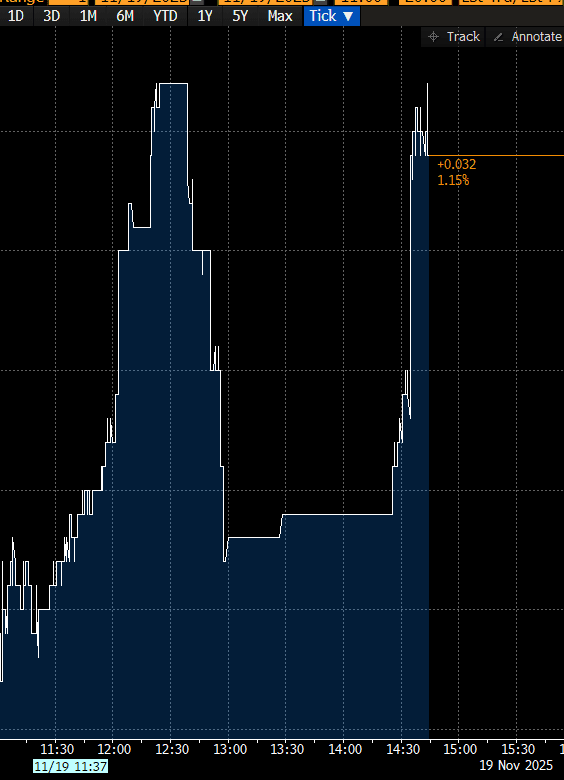

AUD: Asia-Pac: AUD/USD Gives Back Most Of Its Overnight Gains

The AUD/USD has had a range today of 0.6477 - 0.6512 in the Asia- Pac session, it is currently trading around 0.6480, -0.40%. The AUD/USD has drifted lower in our session giving back a lot of its overnight gains. The markets focus for risk will now turn toward the Nvidia results which come out in the US session. The AUD/USD continues to chop around within its wider 0.6350-0.6650 range, first support back toward 0.6440-0.6460 which has been pretty solid the last couple of months, then 0.6350 below that. It would need this move lower in risk to accelerate and become something more significant to challenge down there I would think.

- MNI AU - Westpac Lead Indicator Consistent With Ongoing Recovery: The Westpac leading index rose 0.11% in October up from -0.01% bringing the 6-month annualised rate to 0.35% from 0.1%. The increase was due to stronger consumer confidence. The 6-month rate leads trended growth by 3-9 months and so is consistent with the recovery gaining into H1 2026. The index had been around neutral since April, when the US announced reciprocal tariffs.

- MNI AU - Wages Stabilise But Private Sector Rises Moderating: Q3 wages rose 0.8% q/q to be 3.4% higher on a year ago, in line with Q2 and Bloomberg consensus, signalling a stabilisation consistent with SEEK advertised salary data. In November, the RBA forecast 3.4% y/y for Q4 2025 before moderating to 3% by end 2026. Thus, the Q3 WPI data doesn’t change the outlook for monetary policy with rates likely on hold towards at least mid-2026 as it monitors price and capacity pressures.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD640m), 0.6300 (AUD445m). Upcoming Close Strikes : 0.6550(AUD2.28b Nov 21) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 48 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

INDONESIA: Q4 Activity Data Better But Still Soft Spots

Bank Indonesia’s decision is announced today and 29/35 analysts on Bloomberg expect rates held at 4.75% (see MNI BI Preview). However, recently it has gone against consensus. In October, it held when it was forecast to ease. With inflation firmly within its band, BI is likely to focus on broad-based rupiah weakening but also the limited pass through of 2025’s 125bp of easing to lending rates. Its three consecutive cuts in Q3 and statements that it would support government policy, which is expansionary, signalled a shift to a pro-growth stance.

- Trade and survey data since the October meeting have signalled stronger Q4 growth to date but the details show some weakness such as soft imports, wages and foreign orders.

- Q3 GDP slowed slightly to 5.0% y/y from 5.1% driven by weaker investment but was supported by a pickup in government spending. BI expects 2026 GDP to rise to 5.3% and said that it will continue to support the government’s pro-growth measures.

- Q3 consumption slowed marginally to 4.9% y/y from 5.0% but consumer sentiment fell 1.9% q/q. It rebounded in October to 121.2 from 115.0 despite Q3 manufacturing wages rising only 0.7% y/y after Q1’s 2.1%.

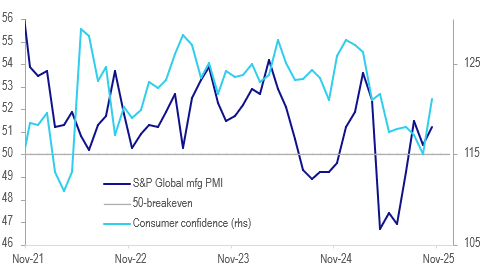

- October S&P Global manufacturing PMI rose to 51.2 after averaging 50.4 in Q3 driven by stronger domestic orders and associated increase in hiring. However, it underperformed ASEAN.

Indonesia activity outlook

Source: MNI - Market News/LSEG/Bloomberg Finance L.P.

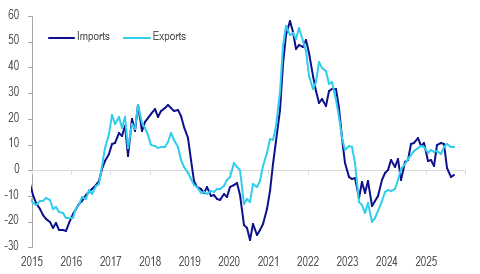

- Robust merchandise export growth at 11.4% y/y drove the September 3-month average trade surplus to its highest since December 2022. Shipments to China, US, Europe, Singapore and Thailand have been strong but weak to Japan, India and Australia.

- However, 3-month average import growth fell 1.7% y/y, a sign of soft domestic demand.

- Tourist arrivals are also slowing but still rose 9.6% y/y 3-month average in September but down from 20.7% a year ago.

Indonesia merchandise exports vs imports y/y% 3-mth moving average

Source: MNI - Market News/LSEG

JGBS AUCTION: Poor Demand Metrics For 20Y Auction

The 20-year JGB auction delivered weak results across key metrics. The low-price underperformed dealer forecasts, which were set at 98.60 according to a Bloomberg poll. Moreover, the cover ratio dropped to 3.2825x from 3.5599x in the previous outing, and the auction tail lengthened sharply to 0.31 from 0.10.

- As noted in the auction preview, today’s offering featured an outright yield at its cycle high, 10-15bps above last month’s level.

- Moreover, the 10/20 yield curve remained near its recent high, its steepest since 1999.

- Accordingly, this result aligns with the lacklustre performance observed in the 30-year JGB auction earlier this month.

- Post-auction, the 20-year JGB is ~1bp cheaper.

Source: Bloomberg Finance LP