MNI EUROPEAN MARKETS ANALYSIS: Equities Up On Trade Deal Hopes

- Risk appetite rose after US Presiden Trump commented that a trade deal would be announced Thursday time in the US. The NYT's reported this deal would be with the UK. US stocks futures are higher, with Eminis back close to 5700.

- US yields have firmed, while safe havens have underperformed in the FX space. GBP is off best levels though.

- Later US Q1 preliminary productivity/ULC, jobless claims and April NY Fed inflation expectations as well as German March IP print. The Bank of England is expected to cut rates 25bp to 4.25%.

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher

TYM5 has traded lower within a tight range of 111-13 to 111-19 during the Asia-Pacific session. It last changed hands at 111-13+, down 0-04 from the previous close.

- The US 2-year yield is a little higher, dealing around 3.80%, up 0.02 from its close.

- The US 10-year yield is a little higher, dealing around 4.289%, up 0.02 from its close.

- Headlines have crossed from the NYT that the first trade announcement from the Trump administration will be with the UK. See this link for more details.

- The BOJ minutes via Bloomberg showed a policy committee member expressing the opinion that "there is a good chance that the strengthening tariffs of the United States will have a significant adverse effect on Japan's real economy."

- “The committee member emphasized that if the possibility of adverse effects from tariffs increases, "it will be necessary to more carefully consider the timing of raising policy interest rates."

- A pretty muted response from US treasuries to the trade deal headlines, stocks had a good pop higher(ESM5 +0.80%) and have held onto these gains for now.

- The 10-year Yield range seems to be 4.10% - 4.45%, price is back to the 4.25/30% support/pivot within that range. Awaiting the next catalyst for some direction

- Data/Events : US Initial Jobless Claims.

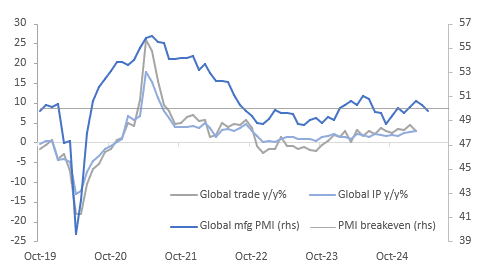

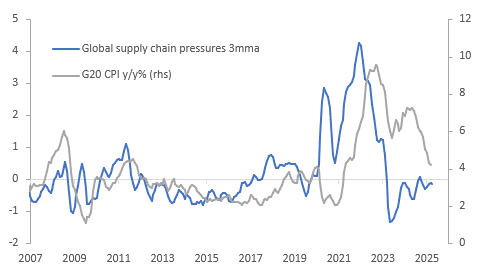

GLOBAL MACRO: April Lead Indicators Signal Weaker Industrial Outlook

The global aggregate of the S&P Global PMI showed a marked deterioration in April as uncertainty soared from US tariff announcements, delay and China’s retaliation. Overall global economic activity remained slightly positive in the month with the composite PMI at 50.8 (March 52.1) but the manufacturing sector shifted slightly into contractionary territory with the PMI down to 49.8 from 50.3 in March and 50.6 in February. This implies that we could see global IP growth turn down in coming months.

Global growth %

- Even if the US and China not just de-escalate trade tensions but come to an agreement, the heightened uncertainty driven by the shift in US trade policy is likely to weigh on global trade flows and industrial production over the coming months. The delay on other reciprocal tariffs expires in early July.

- Global IP rose 0.7% m/m in February to be up 2.9% y/y up from 2.7% in February and the fastest pace since October 2022 and may pick up again in March as firms attempt to beat tariff deadlines. The PMI, metal prices and freight rates in a more difficult global environment all suggest that it is likely to slow over coming months and at best level out.

- The decline in the April S&P Global manufacturing PMI was driven by a one point drop in new orders to 49.8 with new export orders contracting more sharply at 47.2. Only three of the 28 countries reporting said new exports rose. Future output was also lower but remained firmly in expansionary territory at 57.2 but employment is contracting at 49.1. Business confidence was at its lowest since October 2022 due to “gloomier outlooks”.

Global IP growth vs LME metals prices

Source: MNI - Market News/CPB/LSEG

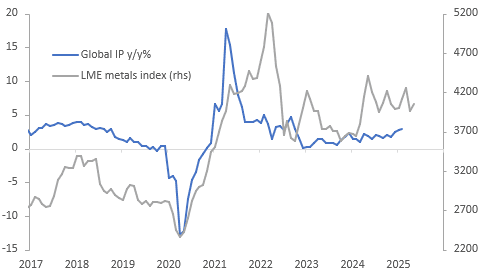

GLOBAL MACRO: April Still Too Early To See If Tariffs Impacting Supply-Chains

Global headline inflation is now less than half its late 2022 peaks, which was boosted by Covid-related supply-chain bottlenecks. There are concerns that recent global trade policy developments will create these issues, especially for the US because of its 145% duty on imports from China. Talks begin this week between the two but de-escalation will be the first step.

- The New York Fed’s measure of supply chain pressures actually eased further in April to -0.29 to its lowest reading since October 2024 but is not far from neutral. It is yet to show any supply-chain problems from tit-for-tat tariffs between the US and China but will be monitored over coming months, especially if an agreement isn’t reached.

Global supply pressures vs inflation

- Supply-chain issues could add to global inflation as was the case during the pandemic. The NY Fed’s index reached a high of +4.44 in December 2021, 9 months before G20 inflation peaked at 9.5%.

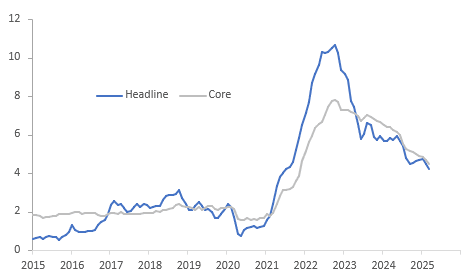

- Currently G20 inflation continues to moderate with it down 0.1pp in March to 4.2% y/y after a high of 9.5% in September 2022.

- OECD headline was 0.3pp lower at 4.2% y/y in March, helped by lower oil prices, but ex food & energy was down 0.2pp to 4.5%. Most countries haven’t yet released April data but preliminary euro area headline was stable, while core rose 0.3pp, and Korea followed the same trend.

OECD CPI y/y%

GLOBAL MACRO: Global Factors Signalling Further Disinflation Ahead

Various global factors are currently pointing towards inflation moderating further as heightened uncertainty related to US tariff announcements has weighed on various commodities and freight rates. Food prices are one of the few items trending upwards but that can vary across countries such as Thailand reporting a decline in vegetable prices in April due to increased supply.

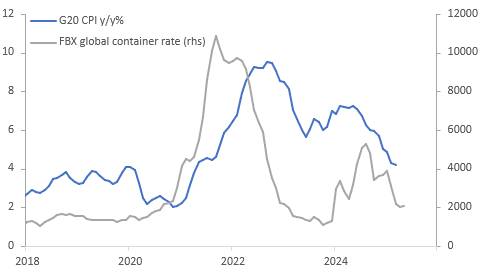

- Global freight rates for bulk goods and containers are down around 30% on a year ago in May but are slightly higher on the April average as hopes increase that trade deals will be made with the US. One is due to be announced on Thursday, likely with the UK according to NY Times.

Global inflation vs container rates

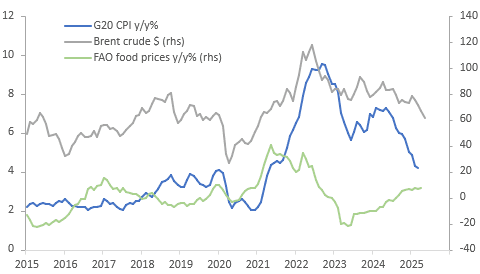

- Oil sold off sharply on concerns that increased protectionism would weigh on global energy demand. May average Brent is down 7.7% m/m after 6.7% in April to be -25.6% y/y. This will impact headline inflation globally and possibly core with a lag if lower transport and input costs feed through to other prices.

- FAO food prices rose 1% m/m in April to be +7.6% y/y up from 6.8% y/y driven by higher prices for cereals, dairy and meat. However, rice has been declining with processed -40.5% y/y in May and rough rice -30.5% y/y, which is important especially for Asia.

- Other commodities are generally lower with the LME metal price index down 5.8% y/y in May but currently up 2.2% m/m after a 6.9% decline in April. Iron ore is -0.7% in May, the third consecutive monthly fall, to be down 15.9% y/y, as lower expected activity and already implemented US steel tariffs are likely to weigh on demand. Wool prices turned higher in Q4, an important textiles input, but is down 3.8% m/m in May, the first monthly fall since September.

Global inflation vs oil & food prices

Source: MNI - Market News/LSEG

JGBS: Market Reverses Direction, US Tsys & Poor 10Y Auction Weigh

JGB futures are weaker, -17 compared to the settlement levels, after reversing direction following today’s poor 10-year auction.

- The 10-year JGB auction delivered weak results, with the low price falling short of expectations, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 2.5440x from 3.1475x, and the tail lengthened to 0.18 from 0.11.

- This performance came with an outright yield 10-15bps lower than last month and approximately 30bps below the recent cyclical high of 1.596% reached in late March, just before President Trump's announcement on reciprocal tariffs.

- “Governor Ueda says the bank can't ignore the potential downside risks to prices stemming from US tariff measures.” (per BBG).

- Cash US tsys are ~3bps cheaper in today's Asia-Pac session after headlines from the NYT that the first trade deal announcement from the US administration would be with the UK (slated for 10am US time on Thursday).

- Cash JGBs are mixed across benchmarks, with the 20-30-year zone as the outperformer (~1bp richer). The benchmark 10-year yield is 1.4bps higher at 1.321% after being as low as 1.2780 pre-auction.

- Swap rates are flat to 2bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will see Real & Labor Cash Earnings, Household Spending and Coincident/Leading Index data.

AUSSIE BONDS: Modestly Cheaper But Off Bests After Trade Deal HLs

ACGBs (YM flat & XM +2.5) are modestly stronger but at session cheaps.

- Cash US tsys are 2-3bps cheaper, with a slight flattening bias, in today's Asia-Pac session after President Donald Trump has announced an upcoming news conference to reveal a "major trade deal" with an unnamed but "highly respected" country, calling it "the first of many" such agreements to come. Subsequently, the NYT stated that the first trade deal announcement from the US administration would be with the UK (slated for 10am US time on Thursday).

- "ANZ bank's net profit increased over the latest half year to $3.64bn, up 7 per cent compared to the same time last year, with big bank bosses tipping further rises in home prices." (per ABC)

- Cash ACGBs are flat to 3bps richer with the AU-US 10-year yield differential at -5bps.

- Swap rates are lower by around the same amount, with the 3s10s curve flatter.

- The bills strip pricing is flat to -2.

- RBA-dated OIS pricing has changed little across meetings today. A 50bp rate cut in May is given a 4% probability, with a cumulative 105bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$700mn of the 2.75% 21 November 2029 bond.

BONDS: NZGBS: Bull-Flattener Pared By Trade-Deal Induced Risk-On

NZGBs closed showing a bull-flattener. Benchmark yields finished 1-3bps lower after being 3-4bps lower early.

- While the NZ Treasury published financial statements for the nine months ended March 31, the key driver for the local market was US tsys. After a positive lead-in from a post-FOMC rally, US tsys cheapened 2-3bps in today’s Asia-Pac session after headlines from the NYT that the first trade deal announcement from the US administration would be with the UK (slated for 10am US time on Thursday).

- Today’s supply showed solid demand metrics, with cover ratios ranging from 3.90x (May-36) to 3.44x (May-51).

- “New Zealand Minister of Finance Nicola Willis asked the central bank to explain why it planned to keep interest rates at a restrictive level before Governor Adrian Orr's resignation. Willis also sought advice from the Treasury Department on the frequency of Monetary Policy Committee meetings and requested a meeting with Orr to discuss bank capital settings.” (per BBG)

- Swap rates closed 1-4bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed little changed across meetings. 26bps of easing is priced for May, with a cumulative 78bps by November 2025.

- The local calendar will be empty until Card Spending data next Wednesday.

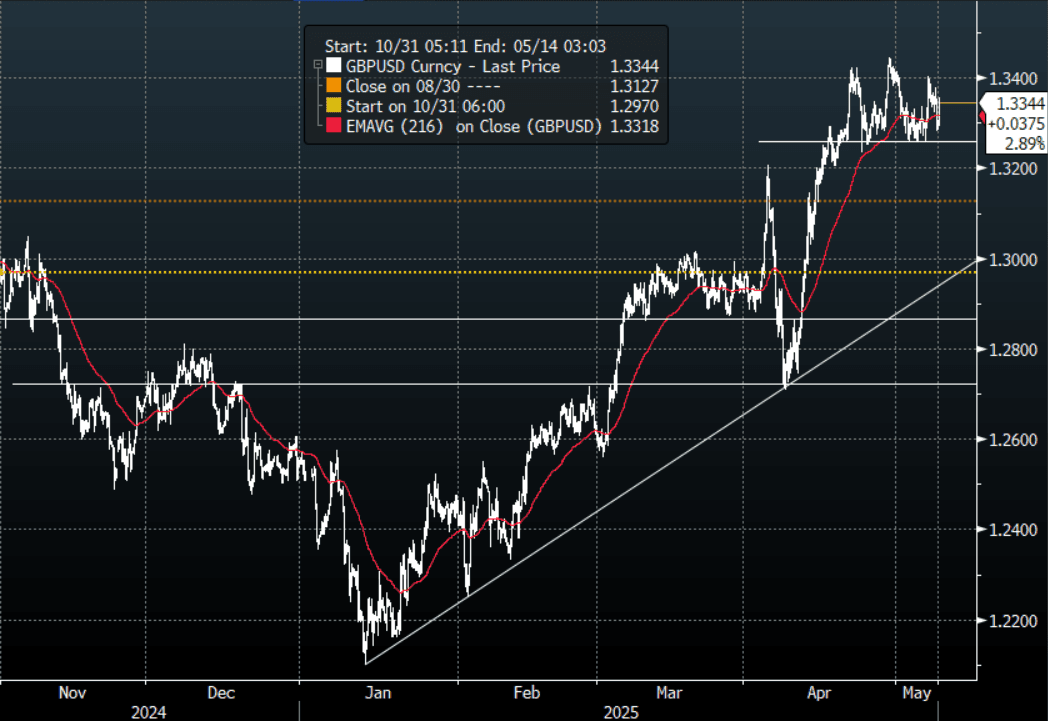

FOREX: G10 Wrap - USD Struggling To Hold Onto Gains

The BBDXY has had an Asian range of 1220.34 - 1223.25, Asia is currently trading around 1221. The USD continues to struggle on any rallies, Asia has seen it give back all of its FOMC gains to a trade deal reportedly with the UK as per the NYT. MNI BOE Decision - Consensus is for a 25bp cut with a question mark over how many members will vote for a 50bp cut. Since the last meeting, most MPC speakers have stuck to the script of tariffs being negative for growth but that the impact on inflation was unclear. The forecasts in the MPR may give them more to base updated communications on. However, with uncertainty so high, we think there is a good chance that some of the structure of the existing guidance remains.

- EUR/USD - Asian range 1.1300 - 1.1336, Asia is currently trading 1.1325. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3286 - 1.3356, Asia is currently dealing around 1.3345, having benefited from the trade deal announcement. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 143.45 - 143.96, pretty muted price action in the Asia session. Sellers should be lining up back towards 146.00/147.00

- USD/CNH - Asian range 7.2167 - 7.2369, the USD/CNY fix printed 7.2073. Asia is currently dealing around 7.2340, sellers should return back towards 7.2500.

- Cross asset : SPX +0.8%, Gold $3390, US 10-Year 4.29%, BBDXY 1220, Crude oil $58.62.

Data/Events : Ger Industrial Production, Spain Industrial Production, US Initial Jobless Claims

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

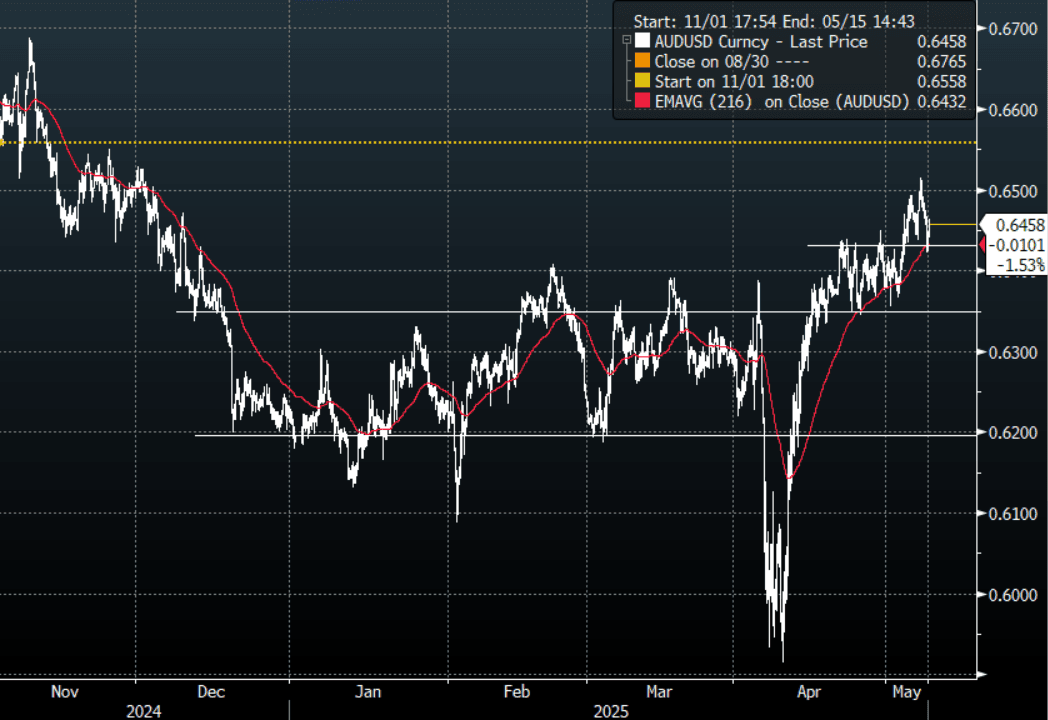

FOREX: Antipodean Wrap - AUD & NZD Regain Losses From FOMC On Trade Deal

The Asian session was just digesting the implications of a patient Fed when headlines from Trump announcing a trade deal tomorrow were posted. The NYT later confirmed that the first trade announcement from the Trump administration will be with the UK. Stocks and risk have reacted positively and look to be holding onto their gains going into the London session. The AUD & NZD have both benefited from this, clawing back all their FOMC losses. The real question will be if London will continue with this or was a trade deal with the UK not already in the price ?

- AUD/USD - Asian range 0.6424 - 0.6464, the AUD is currently dealing around 0.6460. Support should be seen back towards 0.6400 and a break below 0.6300 needed to reverse direction.

- AUD/JPY - Asian range 92.34 - 92.81, price goes into London trading around 92.70. Price continues to stall back towards the resistance seen around 94.00. Support seen back towards the 91.50/92.00 area.

- NZDUSD - Asian range 0.5937 - 0.5975, going into London trading around 0.5970. The NZD continues to hold up well, buyers should return back towards 0.5900 again and then the bigger support is towards 0.5800/50.

- AUD/NZD - Asian range 1.0801 - 1.0836, the Asian session is currently trading 1.0815. Sellers have returned back towards the 1.0850 area.

Fig 1 : AUD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: US China Trade Talks Give Stocks a Boost

As news filters through of a US China trade discussion this weekend and the first trade deal under the Trump administration about to be announced. The US is set to announce a UK trade deal in what could be the start of several.

Flows into Asia equity from foreign investors have turned strongly as the steam comes out of the USD. Major markets in Asia have experienced over US$5bn of inflows over the last five trading days with Taiwan gaining the most, followed by India and South Korea.

- Despite the various stimulus measures announced yesterday the China bourses rise was modest with the Hang Seng up just 0.13% before jumping over 1% today in signs investors are welcoming the stimulus. The CSI 300 had a better day yesterday up +0.61% and backed that up with 0.75% gain today.

- As the government announced an increase in bond issuance to support the economy the KOSPI reacted rising +0.55% mirroring yesterday’s gains.

- The FTSE Bursa Malaysia KLCI was treading water ahead of the Central Bank decision later this afternoon, falling -0.20% after yesterday’s gains of +0.85%.

- The Jakarta Composite has had a very strong period and after eight successive days of gains, fell today by -0.45%.

- Singapore’s FTSE Straits Times is up +0.20% and Philippines PSEi down -0.17%.

- Despite the escalation of tensions between India and Pakistan, the NIFTY 50 eked out +0.14% gains but is trending lower in today’s trading by -0.08%

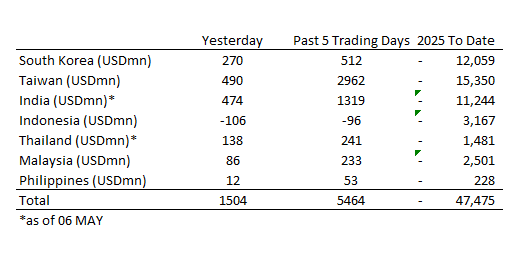

ASIA STOCKS: Strong Inflows Across Major Markets

As the steam comes out of the USD and trade war risks abate for now, major markets in Asia have experienced over US$5bn of inflows over the last five trading days with Taiwan gaining the most, followed by India and South Korea.

- South Korea: Recorded inflows of +$270m as of yesterday, bringing the 5-day total to +$512m. 2025 to date flows are -$12,059m. The 5-day average is +$102m, the 20-day average is -$176m and the 100-day average of -$138m.

- Taiwan: Had inflows of +$490m as of yesterday, with total inflows of +$2,962m over the past 5 days. YTD flows are negative at -$15,350. The 5-day average is +$592m, the 20-day average of +$125m and the 100-day average of -$152m.

- India: Had inflows of +$474m as of the 6th, with total inflows of +$1,319m over the past 5 days. YTD flows are negative -$11,244m. The 5-day average is +$264m, the 20-day average of +$121m and the 100-day average of -$115m.

- Indonesia: Had outflows of -$106m as of yesterday, with total outflows of -$96m over the prior five days. YTD flows are negative -$3,167m. The 5-day average is -$19m, the 20-day average -$67m and the 100-day average -$37m

- Thailand: Recorded inflows of +$138m as of yesterday, inflows totaling +$241m over the past 5 days. YTD flows are negative at -$1,481m. The 5-day average is +$48m, the 20-day average of -$20m the 100-day average of -$18m.

- Malaysia: Recorded inflows of +$86m as of yesterday, totaling +$233m over the past 5 days. YTD flows are negative at -$2,501m. The 5-day average is +$47m, the 20-day average of +$8m and the 100-day average of -$30m.

- Philippines: Saw inflows of +$12m as of yesterday, with net inflows of +$53m over the past 5 days. YTD flows are negative at -$228m. The 5-day average is +$11m, the 20-day average of -$1m the 100-day average of -$3m.

OIL: Rally Following Trade Deal News Leaves Crude Higher On The Week

Global oil markets have been concerned that increased protectionism would reduce global energy demand and so today’s news that the US will announce a trade deal Thursday morning US time has boosted prices today. The NY Times reported that the agreement is with the UK. WTI is up 0.8% to $58.55/bbl, close to the intraday high, and now up 0.6% this week. Brent is 0.8% higher at $61.60 after falling to $61.00 early in the session and is currently +0.5% on the week. The USD index is down 0.1%.

- The news of the first US trade deal will possibly add to optimism of a resolution to the current situation, which is particularly important ahead of the difficult US-China talks taking place this week. US President Trump said that he won’t reduce tariffs on China to smooth the start of negotiations, which are likely to focus on de-escalation rather than a deal.

- Supply remains in focus with OPEC announcing a +400kbd increase in output from June after +400kbd in April but the EIA cutting its 2025 US production forecast due to low prices driving less shale output. Talks continue with Iran and a deal there may allow an easing of sanctions on its oil exports. A truce in Ukraine still seems no closer and thus also a lifting of restrictions on Russia.

- Later US Q1 preliminary productivity/ULC, jobless claims and April NY Fed inflation expectations as well as German March IP print. The Bank of England is expected to cut rates 25bp to 4.25%.

Gold Erases Some of Overnight Losses.

- Despite positive signs on trade talks between the US and China, Gold rallied back again today shrugging off some of yesterday’s losses.

- Gold is up +0.85% in today’s Asia trading session reaching US$3,392.32.

- As the Federal Reserve remained on hold overnight markets focused on Chairman’s Powell’s comments on the trade war and the uncertainty it creates.

- Warning that Trump’s policies could lead to higher inflation and slowing growth re-ignited gold’s safe haven bid after losses overnight.

- Data released shows that the Chinese Central Bank continues to add to its gold reserves, adding 70,000 ounces in April, representing sixth consecutive months that the PBOC has increased gold holdings.

MALAYSIA: Strong March Data Release Ahead of BNM

- Malaysia's Industrial Production beat expectations significantly in March, rising +3.2% up from +1.5% in February and the strongest result in 2025.

- The mining sector drove the increase, rising +1.9% having contracted in February.

- Manufacturing remains robust up +4.0% (from +4.8%)

- Manufacturing sales rose 3.7% y/y versus +4.7% in February

- The BNM meets later today to decide on interest rates with only 5/22 economists predicting a rate cut.

PHILIPPINES: GDP Resilience on Show

- 1Q GDP YoY printed at +5.4%, up from +5.3% in 4Q last year.

- 1Q GDP MoM came in at +1.2% from +1.5% in 4Q.

- Manufacturing rose to +4.1% from +3.3% in 4Q

- Agricultural sector rose to +2.2% from contracting in 4Q

- The service sector moderated to +6.3% from +6.7%.

- Government spending rose by +18.7% from +9.0%

- The consumer continued to drive the economy up +5.3% from +4.7%

- Investments rose +4% from +5.5%

- Exports contribution rose +6.2% from +3.2%

- Imports contribution rose +9.9% from +2.7%

SOUTH KOREA: Country Wrap: Govt Bond Issuance Raised

- South Korea revises 2025 government bond issuance plan to KRW207tn vs initial plan of KRW197.6tn, reflecting extra budget, finance ministry advised yesterday. Of the total, 55-60% will be issued in 1H and ratio of bonds of 20-year or longer vs initial plan has increased. Ratio of bonds with 2-3 year tenures to account for 27-33% of total issuance in 2025, same with initial plan; those with 5-10 year tenures will make up 27-33% of the total vs initial plan of 32-38%. Ratio of bonds of 20-years or longer will consist of 35%-45% of issuance vs 30-40%. Korea’s 10YR government bond yield began the year at 2.87% and sits at 2.59% delivering strong returns for investors.

- South Korea to hold weekly meeting to review macroeconomy and financial issues as major countries’ trade negotiations and geopolitical tensions pose uncertainties, Acting Finance Minister Kim Beom-seok says in a meeting. (source BBG)

- As the government announced an increase in bond issuance to support the economy the KOSPI reacted rising +0.55% mirroring yesterday's gains.

- The Won lost ground today, down -0.44% to 1,397.40

- Bonds move higher in yield across the curve upon the issuance announcement. KTB 10YR 2.63% (+3bps)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 08/05/2025 | 0600/0800 | ** | Trade Balance | |

| 08/05/2025 | 0600/0800 | ** | Industrial Production | |

| 08/05/2025 | 0700/0900 | ** | Industrial Production | |

| 08/05/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 08/05/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data | ||

| 08/05/2025 | 1400/1000 | BOC Financial Stability Report and Financial System Survey | ||

| 08/05/2025 | 1400/1000 | ** | Wholesale Trade | |

| 08/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 08/05/2025 | 1500/1100 | BOC Governor Macklem press conference on Financial System Review | ||

| 08/05/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/05/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 08/05/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 09/05/2025 | 2330/0830 | ** | average wages (p) | |

| 09/05/2025 | 2330/0830 | ** | Household spending | |

| 09/05/2025 | 0600/0800 | *** | CPI Norway | |

| 09/05/2025 | 0800/1000 | * | Industrial Production | |

| 09/05/2025 | 0840/0940 | BOE Bailey Keynote Address at Reykjavik Economic Conference | ||

| 09/05/2025 | 0955/0555 | Fed Governor Michael Barr | ||

| 09/05/2025 | 1045/0645 | Fed Governor Adriana Kugler | ||

| 09/05/2025 | 1115/1215 | BOE's Pill At National MPC Agency Briefing | ||

| 09/05/2025 | - | *** | Trade | |

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | New York Fed's John Williams | ||

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 09/05/2025 | 1235/0835 | New York Fed's Roberto Perli |