GLOBAL MACRO: April Still Too Early To See If Tariffs Impacting Supply-Chains

Global headline inflation is now less than half its late 2022 peaks, which was boosted by Covid-related supply-chain bottlenecks. There are concerns that recent global trade policy developments will create these issues, especially for the US because of its 145% duty on imports from China. Talks begin this week between the two but de-escalation will be the first step.

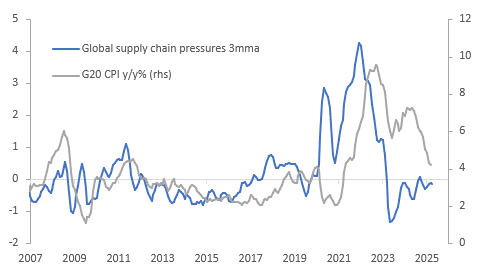

- The New York Fed’s measure of supply chain pressures actually eased further in April to -0.29 to its lowest reading since October 2024 but is not far from neutral. It is yet to show any supply-chain problems from tit-for-tat tariffs between the US and China but will be monitored over coming months, especially if an agreement isn’t reached.

Global supply pressures vs inflation

- Supply-chain issues could add to global inflation as was the case during the pandemic. The NY Fed’s index reached a high of +4.44 in December 2021, 9 months before G20 inflation peaked at 9.5%.

- Currently G20 inflation continues to moderate with it down 0.1pp in March to 4.2% y/y after a high of 9.5% in September 2022.

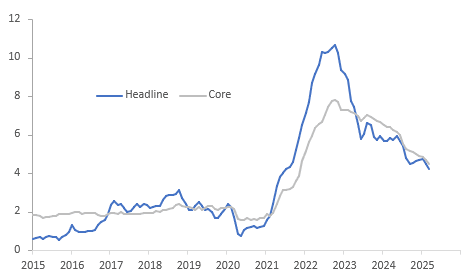

- OECD headline was 0.3pp lower at 4.2% y/y in March, helped by lower oil prices, but ex food & energy was down 0.2pp to 4.5%. Most countries haven’t yet released April data but preliminary euro area headline was stable, while core rose 0.3pp, and Korea followed the same trend.

OECD CPI y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper But At Bests, Tracking US Tsys, CC Down, BC Unch

ACGBs (YM -12.0 & XM -16.5) are significantly cheaper but at session highs after today’s domestic confidence data.

- Westpac’s measure of consumer confidence sank 6% m/m in April to 90.1 down from 95.9 in March, which had been boosted by February’s rate cut. Both current conditions and expectations were lower.

- NAB’s March business survey was little changed from February with confidence down 1 point to -3 and conditions up 1 point to +4. The result is in line with moderate growth. The survey results don’t suggest any worry about a global trade war before US reciprocal tariffs were announced, which were higher than expected.

- However, the key driver of today’s intra-session move is likely to be US tsys. Cash US tsys are showing a bull-steepener, with benchmark yields flat to 3bps lower, in today's Asia-Pac session after yesterday’s extremely heavy session.

- Cash ACGBs are 11-16bps cheaper with the AU-US 10-year yield differential at +10bps.

- Swap rates are 8-13bps higher, with the 3s10s curve steeper.

- The bills strip has cheapened dramatically, with pricing -5 to -12.

- RBA-dated OIS pricing is 4-14bps firmer across meetings today. A 50bp rate cut in May is given a 44% probability, with a cumulative 110bps of easing priced by year-end.

AUSTRALIA DATA: NAB Business Survey Little Changed Ahead Of US Tariffs

NAB’s March business survey was little changed from February with confidence down 1 point to -3 and conditions up 1 point to +4. The result is in line with moderate growth but doesn’t signal any pickup in the pace of the recovery, likely given heightened uncertainty. The survey results don’t suggest any worry about a global trade war before US reciprocal tariffs were announced, which were higher than expected.

- On the inflation side, labour costs remained elevated at 1.5% 3m/3m after 1.6% and purchase costs were steady at 1.4%. However, the rise in final product prices held at a subdued 0.4%

- The pickup in conditions was driven by a 2 point increase in profitability to +1, while employment was steady at +4 and trading fell 1 point to +6. Capex rose 1 point to +7.

- Forward looking orders rose 1 point to -2, while stocks increased 2 points to +5, which may be indicating preparation for stronger demand as capacity utilisation rose almost 1pp to 82.9%.

- On the external front, exports were flat at 0 and sales rose 1 point to +1.

AUSSIE BONDS: ACGB Jun-34 (Green) Auction Result

The AOFM sells A$400mn of the 4.25% 21 June 2034 Green Bond:

- Average Yield (%): 4.1725 (prev. 4.4693)

- High Yield (%): 4.1750 (prev. 4.4725)

- Bid/Cover: 4.8875x (prev. 5.1833x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): 51 (prev. 39.5)

- Bidders: 41 (prev. 38), 13 (prev. 12) successful, 6 (prev. 6) allocated in full