GLOBAL MACRO: April Lead Indicators Signal Weaker Industrial Outlook

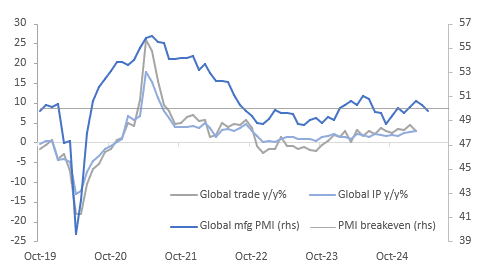

The global aggregate of the S&P Global PMI showed a marked deterioration in April as uncertainty soared from US tariff announcements, delay and China’s retaliation. Overall global economic activity remained slightly positive in the month with the composite PMI at 50.8 (March 52.1) but the manufacturing sector shifted slightly into contractionary territory with the PMI down to 49.8 from 50.3 in March and 50.6 in February. This implies that we could see global IP growth turn down in coming months.

Global growth %

- Even if the US and China not just de-escalate trade tensions but come to an agreement, the heightened uncertainty driven by the shift in US trade policy is likely to weigh on global trade flows and industrial production over the coming months. The delay on other reciprocal tariffs expires in early July.

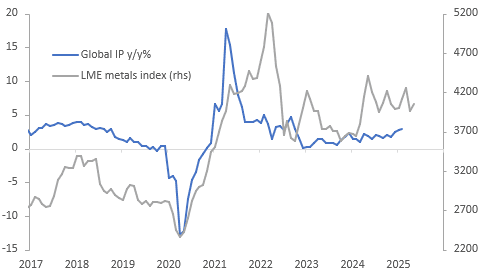

- Global IP rose 0.7% m/m in February to be up 2.9% y/y up from 2.7% in February and the fastest pace since October 2022 and may pick up again in March as firms attempt to beat tariff deadlines. The PMI, metal prices and freight rates in a more difficult global environment all suggest that it is likely to slow over coming months and at best level out.

- The decline in the April S&P Global manufacturing PMI was driven by a one point drop in new orders to 49.8 with new export orders contracting more sharply at 47.2. Only three of the 28 countries reporting said new exports rose. Future output was also lower but remained firmly in expansionary territory at 57.2 but employment is contracting at 49.1. Business confidence was at its lowest since October 2022 due to “gloomier outlooks”.

Global IP growth vs LME metals prices

Source: MNI - Market News/CPB/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Overnight Falls in Gold

- In US trading overnight, gold fell for the third day straight.

- As markets remain uncertain, even gold’s safe haven bid has been challenged with bullion down -1.8% overnight to US$2,983.28.

- Despite reassurances from Trump officials to investors that the tariff plan won’t derail the economy, there remains little appetite for risk in most asset classes.

- Despite the reassurances, Trump then threated with upping the tariffs on China.

- With the arbitrage in pricing between the US and UK over, the flow of physical gold into London resumed in March with an increase for the first time in five months.

- Yesterday, in China’s FX Reserves release, the Central Bank provided details on the growth of gold held by the PBOC, as it rose for a fifth consecutive month.

US TSYS: Cash Bonds Little Changed After Yesterday’s Heavy Close

TYM5 is 111-27+, -0-06+ from closing levels in today's Asia-Pac session.

- Cash US tsys are dealing slightly mixed, with a steepening bias, in today’s Asia-Pac session.

- Markets experienced significant turbulence yesterday, with extreme volatility driven by poor liquidity conditions. The situation was further exacerbated by a flurry of social media activity from President Trump, who threatened an additional 50% tariff on Chinese imports.

- The US 10-year yield, which ranged between 3.85% and 3.95% during yesterday’s Asia-Pac session, moved sharply higher as European markets opened. It reached an intraday high of 4.21% before finishing at 4.18%, +19bps. It is currently trading at 4.1740%, 0.95bp lower.

- Economic data remains light ahead of key releases later this week. Markets are looking ahead to Wednesday's release of the March FOMC minutes, followed by CPI data on Thursday and PPI on Friday.

LNG: Less Demand From China Should Help Europe’s Refilling

European natural gas prices fell early in the session but then trended higher. After falling to EUR 33.51 they reached a peak of EUR 38.62 before moderating to EUR 35.87 to be down 1.5%. The recovery was helped by EU President von der Leyen saying that the bloc will negotiate with the US on a trade deal.

- Tariffs on China’s imports from the US should help with Europe’s refilling over the summer, which has been a material concern, as cargoes are redirected. European storage was at around 34% full last week, below the 5-year seasonal average of 45%, according to Bloomberg, and it needs to be at 90% by November 1. Contract prices trend higher until October 2025, still discouraging refilling but the spread has narrowed significantly from earlier in the year.

- Unplanned outages remain a risk to markets. Norway’s Gassco has just announced 5.1mcm/d from today will be unexpectedly unavailable.

- Bloomberg notes that European gas is in oversold territory based on the 14-day RSI.

- US gas rose to a high of $4.03 before trending lower to finish down 5.6% to $3.73. Concerns that US tariffs and subsequent trade war will weigh on growth and thus energy demand have pressured prices and they are now down 12.5% in April.

- Forecasts by Vaisala for cooler weather across the eastern US and Great Lakes in mid-April as well as lower temperatures in the Pacific and Northwest regions could see an increase in power demand though.

- US lower-48 gas production rose 5.1% y/y on Monday and demand +10% y/y.