MNI EUROPEAN MARKETS ANALYSIS: Aust July Jobs Data Solid

- USD/JPY is weaker following comments from US Tsy Secretary Bessent that the BoJ is behind the inflation curve. In Australia, the July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. The AUD tried to go higher but had no follow through.

- US Tsy yields have been relatively steady, while JGBs are showing a bear-flattener across benchmarks, with yields flat to 5bps higher. The benchmark 5-year yield is 4.2bps higher at 1.106% after yesterday's poor auction.

- Later the Fed’s Musalem (voter) and Barkin speak. July US PPI & jobless claims, UK Q2 GDP & June IP/trade, Q2 euro area/employment & June IP are released.

MARKETS

US TSYS: Asia Wrap - Yields Relatively Unchanged In A Quiet Session

The TYU5 range has been 112-05 to 112-09 during the Asia-Pacific session. It last changed hands at 112-07, up 0-01+ from the previous close.

- The US 2-year yield is trading around 3.672%.

- The US 10-year yield is trading around 4.232%.

- Good demand towards the 10-Year 4.30/35%% pivot saw yields move lower. That area should continue to see demand cap yields, longs will be looking to target the 4.10% area initially.

- "A block of 4,000 contracts in five-year bond September futures traded at a price of 109-02 1/4 on CBOT. A total of 44,981 contracts traded so far in this session." - BBG

- Liz Ann Sonders on X: “Supercore CPI increased by 0.48% m/m in July … one of largest gains this year and a break from prior months’ tame prints.” See Fig.1 Below

- Ben Hunt on X: “They’re gonna run it hot like you can’t even believe.”

- Paulo Macro on X: “Hard to believe Powell is gonna talk up Sept rate cuts at Jackson Hole next week after that core print yesterday but I guess the music is still playing and they wanna dance right up until until the record scratch.”

- Data/Events: PPI, Initial Jobless Claims

Fig 1: Supercore CPI

Source: MNI - Market News/Bloomberg Finance L.P/@LizAnnSonders

JGBS: Sharp Bear Flattener, Q2 GDP Tomorrow

JGB futures are sharply weaker and near session lows, -39 compared to settlement levels.

- “Rakuten Bank, the online banking arm of Rakuten Group, will refrain from actively buying Japanese government bonds (JGBs), Bloomberg News reported on Thursday, citing a top official. CEO Tomotaka Tori said the group will hold its purchase until the Bank of Japan implements further interest rate hikes, citing market volatility and policy uncertainty.” (MTN via BBG)

- "They're behind the curve," Bessent told Bloomberg TV on Wednesday, noting that he discussed Japan's inflation problem with BOJ Governor Kazuo Ueda. "So they're going to be hiking and they need to get their inflation problem under control," he added." BBG

- JGBs are showing a bear-flattener across benchmarks, with yields flat to 5bps higher. The benchmark 5-year yield is 4.2bps higher at 1.106% after yesterday's poor auction.

- Swap rates are 3-5bps higher.

- Tomorrow, the local calendar will see Q2 GDP(P), IP(F), Capacity Utilisation and Weekly International Investment Flow data.

AUSSIE BONDS: Slightly Cheaper After Jobs Report

ACGBs (YM +1.5 & XM +1.0) are slightly weaker after today’s Employment Report.

- The July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. There was also a clear trend to more full-time jobs and hours signalling that demand was robust in the month. While “labour market conditions remain a little tight”, as the RBA said in its August statement, they didn’t appear to ease further in July.

- The unemployment rate dropped 0.1pp to 4.2%. The RBA expects it to peak at 4.3% in H2 and then remain there.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's solid rally.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at -3bps.

- The bills strip is -1 to +2, with a flattening bias.

- RBA-dated OIS pricing is 2-4bps firmer across meetings after the data release. A 25bp rate cut in September is given a 31% probability, with a cumulative 38bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will be empty apart from the AOFM planned sale of A$1000mn of the 2.75% 2 1 November 2029 bond.

AUSTRALIA DATA: July Sees Some Normalisation In Labour Indicators

The July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. There was also a clear trend to more full-time jobs and hours signalling that demand was robust in the month. While “labour market conditions remain a little tight”, as the RBA said in its August statement, they didn’t appear to ease further in July.

Australia employment 3m/3m average annualised %

Source: MNI - Market News/ABS

- Employment rose 24.5k last month with the full-time component (FT) up 60.5k, the largest monthly gain since February 2024, while part-time (PT) fell 35.9k. The data can be volatile but the 3-month sum is consistent with this split at +63.7K and -41.1k respectively.

- Employment growth moderated to 1.8% y/y from 2% but FT rose to 1.9% from 1.7% while PT slowed to 1.8% from 2.7%. FT 3-month momentum picked up to its highest since September.

- Hours worked rose 0.3% m/m after declining 0.9% in June with FT up 0.7% but PT down 1.5%. Growth in total hours was stable at 2.1% y/y, while it picked up to 2.3% for FT but slowed to 1.1% for PT. Consistent with this underemployment fell back to May’s rate.

- The unemployment rate dropped 0.1pp to 4.2%, as expected, but it was in the high 4.2s. The RBA expects it to peak at 4.3% in H2 and then remain there. Growth in the number of unemployed moderated to 3.1% y/y from 9.6%.

- YTD labour force numbers are up 162k while job gains are 113.3k and as a result the unemployment rate is slightly higher. While the employment/population and participation rates are off the January highs, they remain elevated signalling that the economy is still able to absorb most people into the jobs market.

Australia unemployment rate %

Source: MNI - Market News/ABS

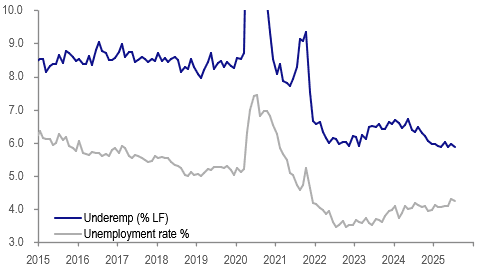

AUSTRALIA: Some Indicators Signal Stabilisation In Labour Market Easing

The RBA eased its language regarding the labour market in its August meeting statement with conditions now “a little tight”. In July, Governor Bullock spoke about the bank’s dual mandate which includes full employment and showed some of the other jobs-related data that it follows. They show that the labour market has eased from the 2022-23 heights but may now be stabilising with some indicators still tighter than average.

- One indicator that hasn’t shown an easing in the labour market is the underemployment rate which in July fell 0.1pp to 5.9% and has been just under the 2022 low on average this year. A pick up in underemployment would signal a weakening in labour demand resulting in people not working as much as they’d like.

Australia underutilisation %

- Growth in hours worked has eased and was up 2.1% y/y in July down from January’s 3.6% but momentum in full-time hours is recovering suggesting solid labour demand. It is easier for firms to adjust hours than change headcount and so the trend could reflect current elevated uncertainty.

- Bullock noted that the “quit rate” had returned to around pre-pandemic rates, also a sign of labour market easing. It tentatively appears to have stabilised around this level.

- The NAB business survey measure of labour shortages remains above the series average but continued to moderate over H1 2025.

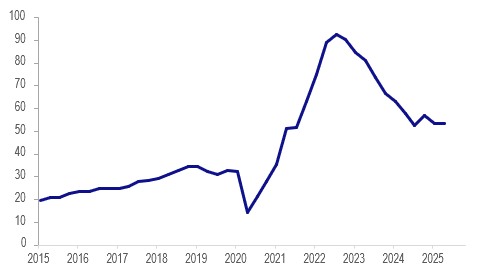

- Vacancies-to-unemployment appears to have troughed in Q3 2024 and has been moving sideways since. It is down almost 40pp since its 2022 high of around 92% but remains about 15pp above the historical average.

Australia vacancies/unemployment %

BONDS: NZGBS: Slight Bull-Steepener On A Data-Light Day

NZGBs closed 1-2bps richer, with the 2/10 curve steeper, on a data-light day.

- The local market did underperform in the $-bloc, with the NZ-US and NZ-AU 10-year yield differentials 5bps and 2bps wider, respectively.

- “New Zealand households' perception of current inflation for the September quarter rose to a mean of 8.1% from 6.9% in the June quarter, but was slightly down from 8.2% a year earlier.” (MTN via BBG)

- Today’s supply saw good demand, with cover ratios ranging from 3.15x (Apr-37) to 4.95x (Apr-29).

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's solid rally. Thursday's US data includes weekly jobless claims and PPI, eyed for both price pressures in their own right and helping hone July PCE estimates (after the CPI data, MNI's survey of estimates points to 0.25% M/M for core PCE). Fed speakers include Musalem and Barkin.

- Swap rates closed 1bp lower.

- RBNZ dated OIS pricing closed slightly softer across meetings. 23bps of easing is priced for August, with a cumulative 42bps by November 2025.

- Tomorrow, the local calendar will see the July BNZ manufacturing PMI Index, Net Migration and July monthly price series.

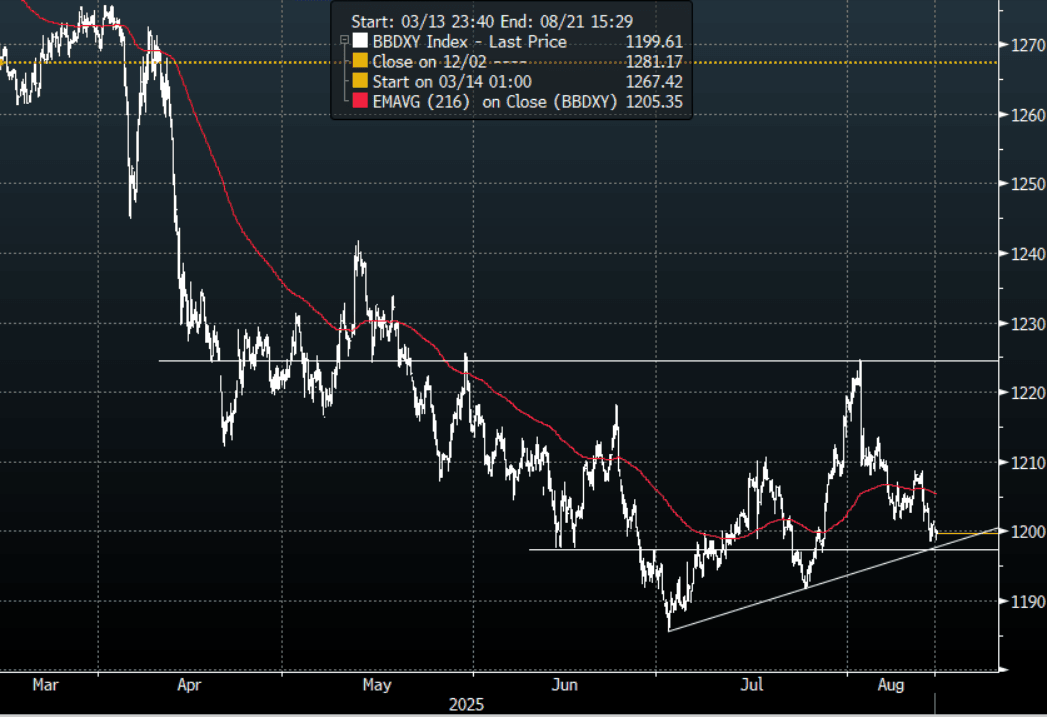

FOREX: Asia FX Wrap - BBDXY Is Probing Below 1200

The BBDXY has had a range of 1198.65 - 1200.56 in the Asia-Pac session, it is currently trading around 1199, -0.12%. The USD had another leg lower but found some demand again towards its support just below 1200. This is clearly the side the market is more comfortable trading and a sustained break below 1197/1195 could see the move lower regain momentum and a retest of the year's lows.

- EUR/USD - Asian range 1.1699 - 1.1715, Asia is currently trading 1.1705. The market moved very quickly back to 1.1700 where it stalled on its first attempt to challenge this area. Will this second attempt have the impetus to break through.

- GBP/USD - Asian range 1.3571 - 1.3592, Asia is currently dealing around 1.3575. The pair bounced nicely off the 1.3100/1.3200 support area. GBP extended above 1.3500 overnight and should continue to find support on dips while the USD remains under pressure. First support seen now back towards 1.3450.

- USD/CNH - Asian range 7.1681-7.1817, the USD/CNY fix printed 7.1337, Asia is currently dealing around 7.1740. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.05%, Gold $3360, US 10-Year 4.235%, BBDXY 1199, Crude Oil $62.90

- Data/Events : France CPI, Ital General Government Debt, EZ Industrial Production/Employment

Fig 1: BBDXY 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

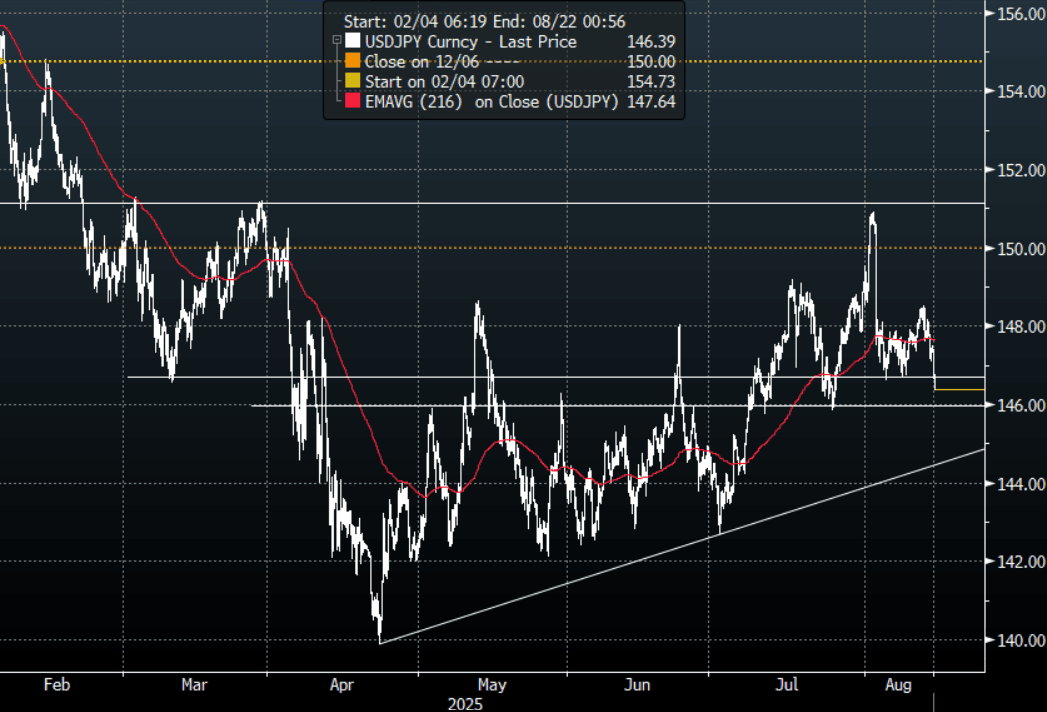

JPY: Asia Wrap - USD/JPY Breaks Below 147.00 On Bessent Comments

The Asia-Pac USD/JPY range has been 146.38-147.42, Asia is currently trading around 146.40, -0.68%. USD/JPY traded heavy for most of the overnight session eventually finding some demand back toward the 147.00 area. Comments from Scott Bessent in a Bloomberg interview then gave it the nudge it needed to break through this demand and extend lower. Price is currently probing the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again.

- “They’re behind the curve,” Bessent told Bloomberg TV on Wednesday, noting that he discussed Japan’s inflation problem with BOJ Governor Kazuo Ueda. “So they’re going to be hiking and they need to get their inflation problem under control,” he added." BBG

- "Hideo Kumano, executive economist at Dai-Ichi Life Research Institute, said "Bessent may be trying to weaken the dollar through his comments on US and Japanese monetary policy," and that by commenting on another country's policy, "he's breaking the rules."

- The most notable underperformer in Asian stocks today are the Japan benchmark indices, with the Topix and the NKY 225 off a little over 1%.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.01b), 149.00($1.15b).Upcoming Close Strikes : 145.00($920m Aug 15), 150.00($685m Aug 15), 150.00($846m Aug 19) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Tries Higher On Employment, No Follow Through

The AUD/USD has had a range of 0.6543 - 0.6569 in the Asia- Pac session, it is currently trading around 0.6550, +0.10%. US equities continue to grind higher making new all-time highs. The more US cuts get priced in, the more pressure it puts on an already bearish USD market. I felt the bounce back towards 0.6550 offered a good risk/reward to fade initially but if the US starts pricing in more aggressive cuts can the AUD ignore it? The Price remains firmly in the 0.6350-0.6650 range, a sustained break back above 0.6650 is needed to potentially regain upward momentum. The AUD attempted to move higher on the employment data but could not hold onto those gains and has quickly settled back to where it started prior to the print.

- AUSTRALIA DATA: July Sees Some Normalisation In Labour Indicators. The July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. There was also a clear trend to more full-time jobs and hours signalling that demand was robust in the month. While “labour market conditions remain a little tight”, as the RBA said in its August statement, they didn’t appear to ease further in July.

- CBA Expects One More Cut As More Optimistic On Growth. The RBA unanimously cut rates 25bp to 3.6% on Tuesday as was widely expected bringing total easing this cycle to 75bp. CBA expects one more rate cut in November and notes that its growth forecasts are more optimistic than the RBA’s. However, the risks are skewed that there will be more in 2026 depending on the data.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD1.33bm), 0.6690(AUD583m). Upcoming Close Strikes : 0.6523(AUD562m Aug 15), 0.6515(AUD673m Aug 19) - BBG

- CFTC Data shows Asset managers added to their shorts -60729(Last -49183), the Leveraged community added very slightly to their own shorts -13997(Last -13823).

- AUD/JPY - Asia-Pac range 95.96 - 96.51, Asia is trading around 96.00. The pair has bounced and tested its first resistance around the 96.50/97.00 area where momentum stalled. The sellers have capped the move for now, price is firmly back into the 94.50-97.50 range.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

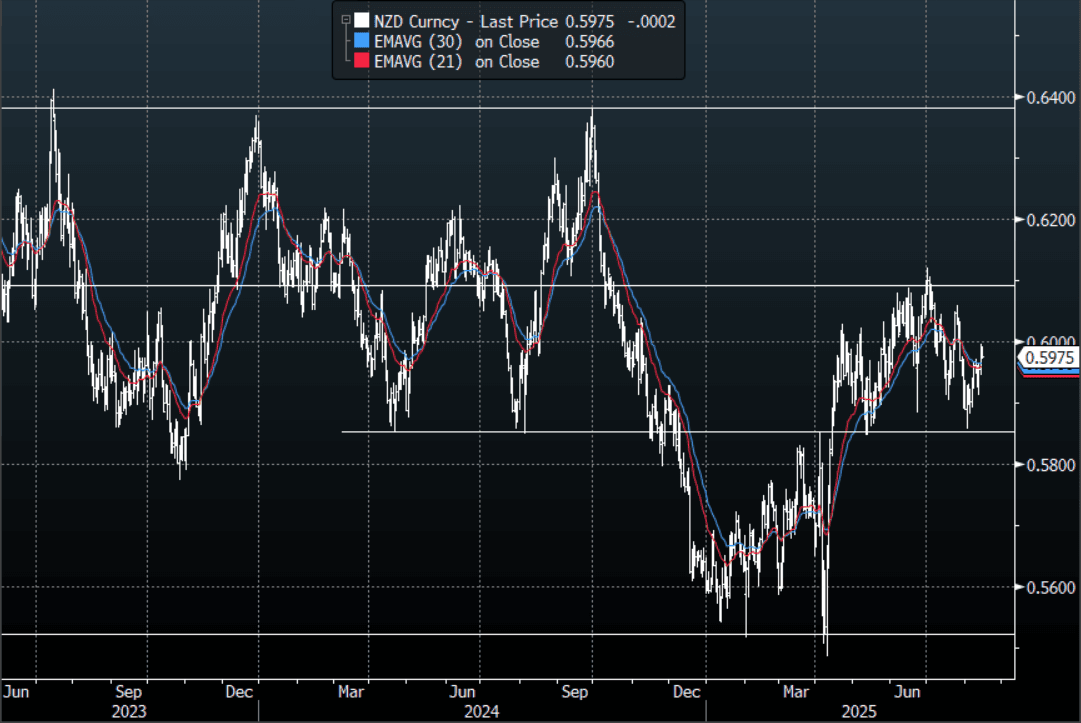

NZD: Asia Wrap - NZD/USD Drifting On A 0.59 Handle

The NZD/USD had a range of 0.5972 - 0.5991 in the Asia-Pac session, going into the London open trading around 0.5980, +0.04%. US equities continue to grind higher making new all-time highs. The more US cuts get priced in, the more pressure it puts on an already bearish USD market. Risk has opened a little lower this morning, E-minis -0.10%, NQU5 -0.10%. The NZD/USD is still firmly within its 0.5850-0.6150 range, the USD will need to break lower to test the top-end.

- "NZ Mean Household 2-Year Inflation Expectation 4.6%: RBNZ Survey. RBNZ publishes 3q Tara-ā-Whare Household expectations survey results, on website. Mean expected inflation in two years is 4.6% down from 4.7% in 2q. Median expected inflation rate in two years is 3%. Unchanged for sixth straight quarter.Mean expected inflation in one year is 6% up from 5.6% in 2q" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6000(NZD340m), 0.5825(NZD300m). Upcoming Close Strikes : 0.5500(NZD300m Aug 19). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0943 - 1.0970, currently trading 1.0955. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Weighed By Stronger Yen, Australia & Indonesia Outperform

Asian stock markets are showing mixed trends in Thursday trade. The most notable underperformer is Japan benchmark indices, with the Topix and the NKY 225 off over 1%. Trends elsewhere are mixed, with aggregate moves under 1% at this stage. In terms of US futures we sit a little weaker, but trends have been relatively steady so far today

- A stronger yen (USD/JPY is down sub 146.50, +0.65% in yen terms) in the aftermath of comments from US Tsy Secretary that the BoJ is behind the curve in addressing inflation, is a headwind for Japan stocks. The Topix transportation index is down close to 1.85%, so slightly underperforming the headline index. This index is often sensitive to exchange rate shifts.

- Australia's ASX 200 is up around 0.55%, outperforming at the margins. Earlier jobs data painted a resilient backdrop, particularly in terms of the surge in full time jobs growth and the slight dip in the unemployment rate.

- South Korea's Kospi is down around 0.20%, HSBC downgraded local stocks to underweight (from neutral) citing valuations in certain sectors (per BBG). Some concerns around potential tax changes reportedly being considered by the government has been a headwind for stocks of late. Taiwan's Taiex is off around 0.40% at this stage, after closing near record highs yesterday.

- In China and Hong Kong, markets are mixed. Hong Kong was higher earlier, but is now down a touch, while the CSI 300 is up a little over 0.50%, last close to 4200.

- In South East Asia, Singapore is down around 0.4%, while Malaysia and Thailand are also down modestly. Indonesia is up, last +0.80%, to put the JCI at fresh record highs. Offshore inflows have returned of late, while a tailwind from likely easier Fed policy settings is another positive.

ASIA STOCKS: South Korea & Taiwan See Firm Inflows, Thailand Sees Strong Outflow

Inflows were positive into tech bellwethers South Korea and Taiwan yesterday. This followed generally positive tech sentiment in Tuesday US trade, as Fed easing expectations firmed after the US CPI print. Such sentiment continued in Wednesday trade, although tech equity trends were less positive. For South Korea, yesterday's inflow was the strongest daily inflow since July 24, while for Taiwan it ended a two day run of outflows. Taiwan's Taiex index closed yesterday just short of record highs.

- In South East Asia, outflows of just over $200mn for Thailand were notable yesterday. This was the largest outflow day since the start of June this year. The BoT cut rates yesterday and signaled scope for an additional cut. The SET index closed 1.46% higher. We had seen a strong run of offshore inflows since the start of July (nearly $700mn), so yesterday's outflow may have reflected some profit taking.

- Elsewhere, Indonesian inflow momentum remained strong, with the last 3 days bringing in $280mn in net inflows. Malaysian outflows continued at a consistent pace, bringing to days of consecutive outflows to 14.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 467 | 484 | -4441 |

| Taiwan (USDmn) | 327 | 1553 | 4612 |

| India (USDmn)* | -302 | -1221 | -12441 |

| Indonesia (USDmn) | 92 | 290 | -3465 |

| Thailand (USDmn) | -206 | -212 | -1902 |

| Malaysia (USDmn) | -22 | -173 | -3290 |

| Philippines (USDmn) | 17 | 32 | -596 |

| Total (USDmn) | 373 | 753 | -21522 |

| * Data Up To Aug 12 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Stabilises Thursday Ahead Of US-Russia Meeting

Oil prices have stabilised during today’s APAC session. They have trended down for almost all of August on excess supply worries. On Wednesday US crude inventories rose more than expected and the IEA forecast a record market surplus for 2026. WTI is up 0.4% to $62.90/bbl but off its intraday peak of $63.00, while Brent is 0.4% higher at $65.90/bbl after reaching $65.98. The USD index is down 0.1%.

- The market is watching Ukraine developments closely with Presidents Trump and Putin meeting in Alaska on Friday.

- While Trump appears to see this event as the start of a process, any indication that a ceasefire is possible may weigh on oil prices as it increases the chance of an easing of sanctions on Russia. However, Trump has warned that there could be “very severe consequences” if Putin doesn’t agree to a truce. An extra 25% tariff will be imposed on India if there is no peace deal and India continues to buy Russian oil.

- Later the Fed’s Musalem (voter) and Barkin speak. July US PPI & jobless claims, UK Q2 GDP & June IP/trade, Q2 euro area/employment & June IP are released.

GOLD: Bullion Range Trading Ahead Of Friday's Ukraine Meeting, Fed Speak Later

Gold prices have been in a narrow range again reaching an intraday high of $3374.78/oz and then falling to $3355.67 but still 0.2% up on the day at $3361.7. US yields are little changed and the BBDXY USD index is down 0.1%. Gold has been supported by growing expectations of a September Fed 25bp rate cut, which is now more than priced in. It will also be watching Friday’s Trump-Putin talks for any change in geopolitical risks.

- US Treasury Secretary Bessent has called for the Fed to cut rates 50bp in September and noted that they should be around 1.5pp lower than the current level. Also, there is yet to be official confirmation that gold imports will be exempt from duties after President Trump posted that they would be.

- Silver reached $38.739 earlier but has moderated since and is now up 0.2% to $38.587. It has been unable to break initial resistance at $39.655.

- Equities are mixed with the S&P e-mini down 0.1% and Nikkei -1.4% but CSI 300 up 0.5% and ASX +0.6%. Oil prices are higher with WTI +0.4% to $62.88/bbl. Copper is up 0.1%.

- Later the Fed’s Musalem (voter) and Barkin speak. July US PPI & jobless claims, UK Q2 GDP & June IP/trade, Q2 euro area/employment & June IP are released.

CHINA: Could the CGB Curve be Steeper by Year End (Part 1)

- The announcement that VAT will be resume for coupons on government bond has the potential to re-shape asset allocation and the direction for bond yields for the rest of the year and into 2026.

- Bond yields have been in a downward trend since 2018, trading in a 30-40bps range over that period. Since the announcement of tariffs in April, that 30-40bps range has collapsed to 10bps potentially pointing to measures put in place to stem volatility.

- It has been difficult to envisage a point at which bond yields could move to the top end of the the prior (30-40bps) range until the announcement of the VAT.

- According to MNI China Onshore Policy team, domestic banks are facing an added CNY20-40bn of additional tax costs a year and are likely to shift focus to lending and equities, resulting in a structural shift in the investment environment. The VAT changes do not impact retail investors at this stage though the possibility remains for that to be changed in time. There is a weight of money argument here in that with institutions altering their asset allocation it may influence the recommendations made to retail clients going forward.

- This comes at a time when equity markets are not overly expensive and sit only marginally above the 10-year Price to Earnings average.

Fig 1: CSI 300 P/E vs 10-year Average.

Growth may be breaking out of the first quarter undershoot also with BBG's GDPNowcast indicator suggesting that a modest upward momentum may be building.

Fig 2: Bloomberg Economics China GDP Nowcast Current Quarter YoY

CHINA: Could the CGB Curve be Steeper by Year End (Part 2)

- A potential upside for growth comes from the policy announcement this week for subsidy plans on loan interest for individuals and businesses aimed at improving consumption. According to estimates from the CEIC, consumption represents about 40% of the broader economy and has been dragged downwards by the decline in property markets. Consumption patterns for investment products show that risk aversion remains with bond fund growth robust and term deposit levels high. The new policy focuses on subsidies on interest for qualifying personal loans and eligible business loans located within the service sector. Official data shows that retail sales of consumer goods increased 5 percent year on year in the first half of 2025, and retail sales of services rose 5.3 percent, providing strong support for the sustained growth of the Chinese economy and this plan is aimed to boost it further.

- 2025 is a pivotal year in China’s policy cycle, marking the close of the 14th Five-Year Plan and the lead-up to the 15th, which will chart the country’s course from 2026 to 2030.

- A potential headwind for growth comes from lending data showing that New Loans in July contracted for the first time in twenty years. Households repaid over CNY300bn of short-term loans this year, including consumer credit. Yet there is some seasonality to consider here as July is the start of a new quarter and typically when holidays interrupt. A further measure, Aggregate Financing, did increase in July yet the boost was underpinned by government bond issuance.

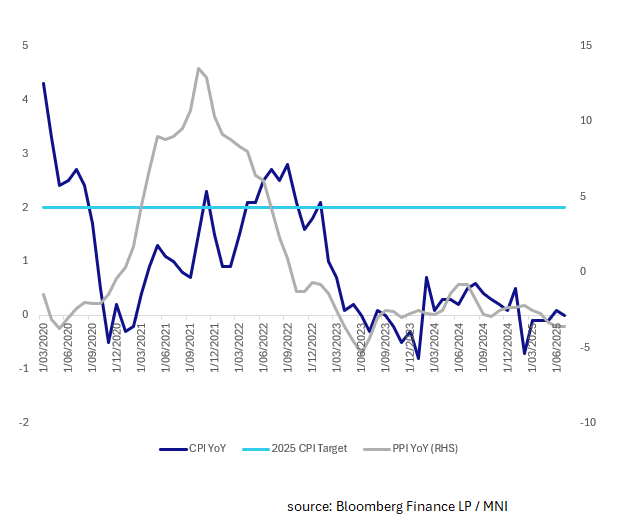

- At the heart of it is the ongoing deflationary pressures as witnessed by the July CPI and PPI remaining firmly in contraction, well below 2025 targets.

Fig 1: China YoY CPI vs PBOC Target & PPI YoY (rhs)

- A recent domestic poll of analysts / strategists expect the PBOC ease monetary policy further, with favored time frame being the fourth quarter. This will be the follow up to the May policy action where interest rates and bank's reserve requirement ratio were cut, both of which challenge the profitability of bond ownership also.

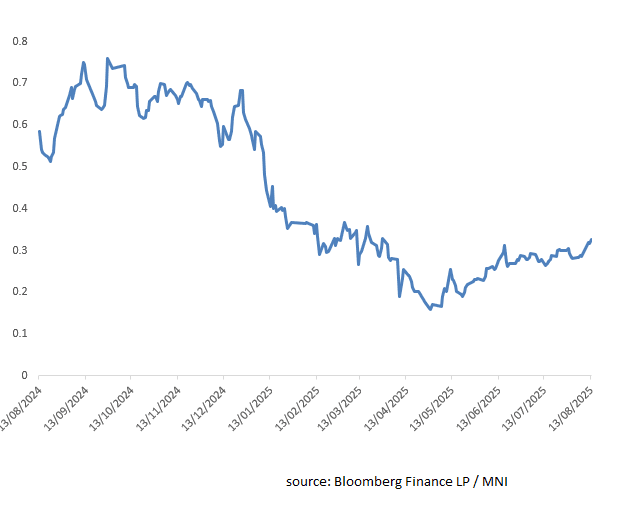

The 2s10s CGB curve remains flat relative to recent trends. The potential for monetary policy changes later in the year, and the subsequent 15th Five-Year Plan may bring about positive changes in the market and the potential for curve steepening.

Fig 2: China CGB 2s10s Curve

- China has allocated 188 billion yuan ($25.9 billion) from its 2025 ultra-long special treasury bond funds to support equipment upgrades across major economic sectors, the National Development and Reform Commission (NDRC) advised. The funds will support about 8,400 projects in industry, energy equipment, power, transportation, logistics, environmental infrastructure, education, culture and tourism, healthcare, elevators in aging residential buildings, electronics, agriculture, grain and oil processing, workplace safety and recycling, leveraging more than 1 trillion yuan in total investment. (source Global Times)

- The overall credit supply is sufficient to effectively meet the financing needs of the real economy. Data released by the People's Bank of China on August 13 showed that at the end of July, the scale of social financing and the growth rate of broad money (M2) both remained at a high level, providing a suitable monetary and financial environment for the real economy and reflecting a moderately loose monetary policy orientation. Experts say that in the first half of the year, the People's Bank of China introduced a package of monetary policies, which effectively supported the recovery of the real economy. The effects of these policies will become more apparent and continue to be released, providing strong support for achieving the annual economic and social development goals and tasks. (source China Securities Journal)

- Equity markets are mixed. Hong Kong was higher earlier, but is now down a touch, while the CSI 300 is up a little over 0.50%, last close to 4200.

- Yuan Reference Rate at 7.1337 Per USD; Estimate 7.1753

- Bonds are steady with the CGB10yr at 1.73% (from yesterday's close of 1.72%)

SOUTH KOREA: Country Wrap: Fuel Tax Cut to be Extended

- Korea will extend its fuel tax cut for an additional two months through the end of October in a bid to ease the financial burden on consumers amid ongoing volatility in global oil prices, the finance ministry said Thursday. Under the latest extension, the current fuel tax reductions — a 10 percent cut on gasoline and a 15 percent cut on diesel and liquefied petroleum gas (LPG) — will remain in place for an additional two months through Oct. 31, according to the Ministry of Economy and Finance. (source Korea Times)

- South Korea's fiscal deficit reached over 94 trillion won (US$68.2 billion) in the first six months of the year, the finance ministry said Thursday. The managed fiscal balance, a key gauge of fiscal health calculated on stricter terms, posted a deficit of 94.3 trillion won in the cited period, according to data from the Ministry of Economy and Finance. While the reading represents an improvement from the over 100 trillion-won shortfall recorded during the same period last year, it marks the fourth-largest on record, according to the Ministry of Economy and Finance. (source Yonhap)

- South Korea's Kospi is down around 0.20%, HSBC downgraded local stocks to underweight (from neutral) citing valuations in certain sectors (per BBG). Some concerns around potential tax changes reportedly being considered by the government has been a headwind for stocks of late.

- The Won is the worst regional performer today falling -0.32% as regional peers all delivered gains.

- Bonds have had a decent rally with intermediates in 2-3bps. KTB 10 at 2.82%

ASIA FX: USD/IDR Tests Under 16100, KRW Underperforms

In Asia FX markets, trends have been mixed in North Asia. USD/CNH tested sub 7.1700, but has seen no follow through. Spot USD/KRW has edged higher. In South East Asia, IDR has rallied strongly, while MYR also remains on the front foot. There have been steadier trends elsewhere.

- USD/CNH got to lows of 7.1681, but sits back around 7.1730/35 in latest dealings. USD/JPY weakness has been a feature of the G10 space, following Bessent comments around the need for the BoJ to hike, which has likely aided CNH at the margins. Still, yen is up around 0.65% at this stage, while CNH is only around +0.1% higher. The USD/CNY fix was set at a fresh low for 2025.

- Spot USD/KRW has risen, up around 0.30% to 1383/84 in latest dealings. There doesn't appear to be a fresh direct catalyst for the move higher, although we remain in recent ranges. Equity sentiment is struggling somewhat, with modest outflows from offshore investors so far today. Spot USD/TWD is down a touch to 29.93, while USD/HKD sits close to 7.8480, away from the top end of the peg band, as HKMA intervened two days in a row.

- In SEA, USD/IDR is testing sub 16100, up around 0.60% in IDR terms. As we noted yesterday, the cross asset backdrop was in favor of further IDR gains. Portfolio have been stronger across the equity and debt space. Local stocks are at a record high, while debt inflows are already +$278mn in the first two days this week. Positive spill over from Fed easing expectations are clearly in play. Local government bond yields continue to track lower, while 5yr CDS is back to mid Feb lows.

- The Ringgit is delivering gains for a fourth day in this morning's session. Gains of +0.25% have seen it trade through the 4.20 technical to be at 4.1970. The gains this week has seen MYR trade below all major moving averages, with the nearest the 20-day EMA at 4.2320.

- Spot USD/THB is a little higher in the first part of Thursday trade, last near 32.29. This keeps us firmly within recent ranges, with late July lows near 32.11. On the topside, we have the 20-day EMA close to 32.42, while the 50-day at 32.58 is likely of more significance, as we have spent little time above this resistance level since mid April of this year. Yesterday's dovish 25bps hike is likely not helping at the margins.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/08/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0600/0700 | ** | Trade Balance | |

| 14/08/2025 | 0600/0700 | ** | Index of Services | |

| 14/08/2025 | 0600/0700 | ** | Index of Production | |

| 14/08/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 14/08/2025 | 0600/0700 | *** | GDP First Estimate | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0645/0845 | *** | HICP (f) | |

| 14/08/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 14/08/2025 | 0900/1100 | ** | Industrial Production | |

| 14/08/2025 | 0900/1100 | *** | GDP (p) | |

| 14/08/2025 | 0900/1100 | * | Employment | |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin | ||

| 15/08/2025 | 2350/0850 | *** | GDP | |

| 15/08/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/08/2025 | 0200/1000 | *** | Retail Sales | |

| 15/08/2025 | 0200/1000 | *** | Industrial Output | |

| 15/08/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/08/2025 | 0430/1330 | ** | Industrial Production | |

| 15/08/2025 | 0700/0900 | * | CH Flash GDP | |

| 15/08/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/08/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/08/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/08/2025 | 1230/0830 | *** | Retail Sales | |

| 15/08/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/08/2025 | 1315/0915 | *** | Industrial Production |