AUSTRALIA DATA: July Sees Some Normalisation In Labour Indicators

The July labour market data printed in line with consensus but also showed some normalisation in key data after June’s deterioration. There was also a clear trend to more full-time jobs and hours signalling that demand was robust in the month. While “labour market conditions remain a little tight”, as the RBA said in its August statement, they didn’t appear to ease further in July.

Australia employment 3m/3m average annualised %

Source: MNI - Market News/ABS

- Employment rose 24.5k last month with the full-time component (FT) up 60.5k, the largest monthly gain since February 2024, while part-time (PT) fell 35.9k. The data can be volatile but the 3-month sum is consistent with this split at +63.7K and -41.1k respectively.

- Employment growth moderated to 1.8% y/y from 2% but FT rose to 1.9% from 1.7% while PT slowed to 1.8% from 2.7%. FT 3-month momentum picked up to its highest since September.

- Hours worked rose 0.3% m/m after declining 0.9% in June with FT up 0.7% but PT down 1.5%. Growth in total hours was stable at 2.1% y/y, while it picked up to 2.3% for FT but slowed to 1.1% for PT. Consistent with this underemployment fell back to May’s rate.

- The unemployment rate dropped 0.1pp to 4.2%, as expected, but it was in the high 4.2s. The RBA expects it to peak at 4.3% in H2 and then remain there. Growth in the number of unemployed moderated to 3.1% y/y from 9.6%.

- YTD labour force numbers are up 162k while job gains are 113.3k and as a result the unemployment rate is slightly higher. While the employment/population and participation rates are off the January highs, they remain elevated signalling that the economy is still able to absorb most people into the jobs market.

Australia unemployment rate %

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA STOCKS: Tech Rallies On Nvidia News, Property Stocks Weaken Though

China tech related stocks are rallying in the first part of Tuesday trade, albeit sit away from session highs in latest dealings. Headlines crossed a little while ago, that US AI/chip bellwether Nvidia would sell its H20 chip to China again. BBG noted: " Nvidia Corp. plans to resume sales of its H20 artificial intelligence accelerator to China, after it received assurances from the US government that it would be granted licenses, the company said in a blog post." (see this link).

- The headline CSI 300 index was up around 0.60%, but is now back to flat, while the HSI is up close to 0.65% in latest dealings. The HSTECH sub index is +1.2%. The ChiNext index is up close to +2%.

- US equity futures are also higher, with the Nasdaq outperforming, last near +0.40%.

- China data releases today have been mixed, house price momentum faltered, while GDP growth was a touch above expectations (y/y holding above 5%).

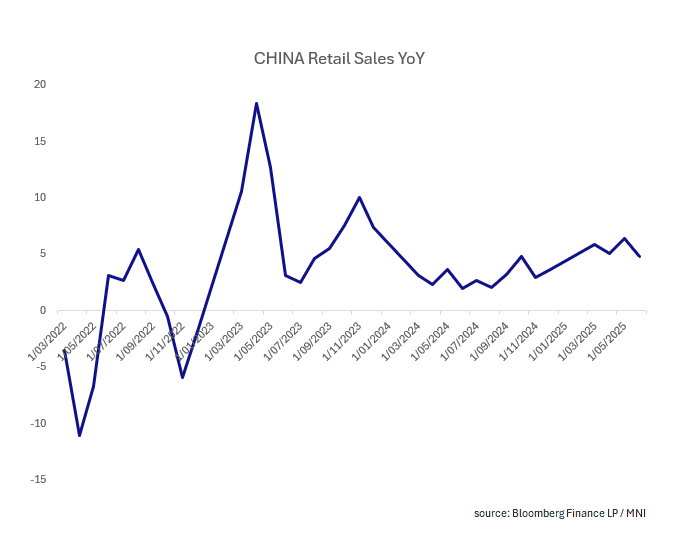

- Retail sales was below expectations for June though, while IP was better than forecast. Fixed asset investment cooled, with property investment slowing further (along with property sales).

- The CSI 300 real estate index is down around 0.85%, taking some gloss off the tech related rally.

CHINA PRESS: China Should Front Load Quotas For Resolving Implicit Debt

China should allow local governments to tap into future bond quotas to proactively address off-balance sheet debt, analysts told Yicai.com. In the first half of the year, approximately 81% of the 2025 quota for resolving implicit debt, equivalent to CNY2.26 trillion in government bonds, was utilised, the outlet reported. With only CNY539 billion remaining under this year’s quota, analysts suggest leveraging future quotas, which stand at CNY2.8 trillion in 2026, and CNY800 billion each in 2027 and 2028.

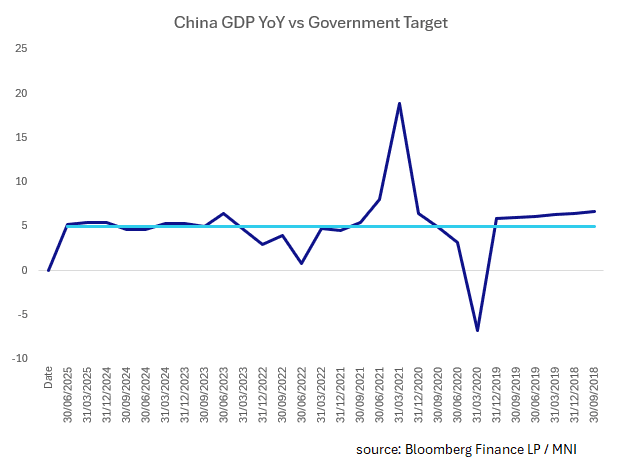

CHINA: GDP in Line with Targets

- China's second quarter GDP YoY printed slightly above estimates at +5.2%, but down from first quarter result of +5.4%.

- The second quarter result keeps GDP on track with the recently announced growth target of "around 5 percent" for 2025, the same as their 2024 target.

- The seasonally adjusted quarter on quarter result was also higher than expected, rising +1.1%, from +1.2% in Q1.

- Retail sales for June were softer at +4.8% (from +6.4% in May) but remain firmly above the 3-year average of 3.5%

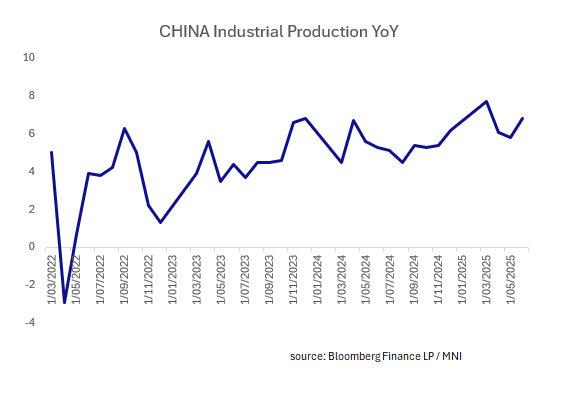

- Industrial production jumped by +6.8% from +5.8%, potentially pointing to benefits from the agreement with the US on tariffs with Manufacturing seeing the biggest rise, up +7.4%, having declined in May.