ASIA STOCKS: Japan Weighed By Stronger Yen, Australia & Indonesia Outperform

Asian stock markets are showing mixed trends in Thursday trade. The most notable underperformer is Japan benchmark indices, with the Topix and the NKY 225 off over 1%. Trends elsewhere are mixed, with aggregate moves under 1% at this stage. In terms of US futures we sit a little weaker, but trends have been relatively steady so far today

- A stronger yen (USD/JPY is down sub 146.50, +0.65% in yen terms) in the aftermath of comments from US Tsy Secretary that the BoJ is behind the curve in addressing inflation, is a headwind for Japan stocks. The Topix transportation index is down close to 1.85%, so slightly underperforming the headline index. This index is often sensitive to exchange rate shifts.

- Australia's ASX 200 is up around 0.55%, outperforming at the margins. Earlier jobs data painted a resilient backdrop, particularly in terms of the surge in full time jobs growth and the slight dip in the unemployment rate.

- South Korea's Kospi is down around 0.20%, HSBC downgraded local stocks to underweight (from neutral) citing valuations in certain sectors (per BBG). Some concerns around potential tax changes reportedly being considered by the government has been a headwind for stocks of late. Taiwan's Taiex is off around 0.40% at this stage, after closing near record highs yesterday.

- In China and Hong Kong, markets are mixed. Hong Kong was higher earlier, but is now down a touch, while the CSI 300 is up a little over 0.50%, last close to 4200.

- In South East Asia, Singapore is down around 0.4%, while Malaysia and Thailand are also down modestly. Indonesia is up, last +0.80%, to put the JCI at fresh record highs. Offshore inflows have returned of late, while a tailwind from likely easier Fed policy settings is another positive.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

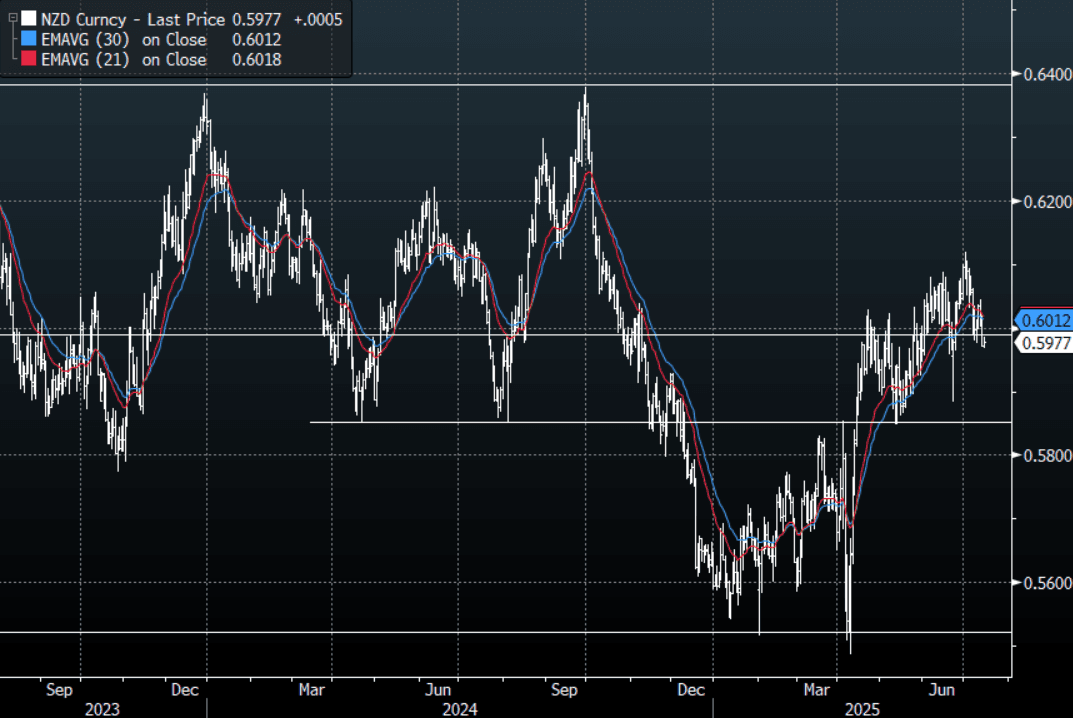

NZD: Asia Wrap - NZD/USD Probing Support Around 0.5980

The NZD/USD had a range of 0.5968 - 0.5986 in the Asia-Pac session, going into the London open trading around 0.5975, +0.08%. Risk got a boost this morning as Nvidia posted on a blog that they had received assurances from the US Government that it would be granted licenses to resume sales of its H20 to China. NZD/USD is again probing its support just below 0.6000, lets see if it can follow through. A break below this support and the market would potentially move back towards the 0.5850/0.5900 area.

- Bloomberg - “Nvidia Corp. plans to resume sales of its H20 artificial intelligence accelerator to China, after it received assurances from the US government that it would be granted licenses, the company said in a blog post.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5932(NZD317m July18).

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654.

- AUD/NZD range for the session has been 1.0945 - 1.0967, currently trading 1.0950. The cross has broken out of its recent range and is now trying to push through the more pivotal 1.0950 area. Dips back to 1.0850/1.0900 should now be supported as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

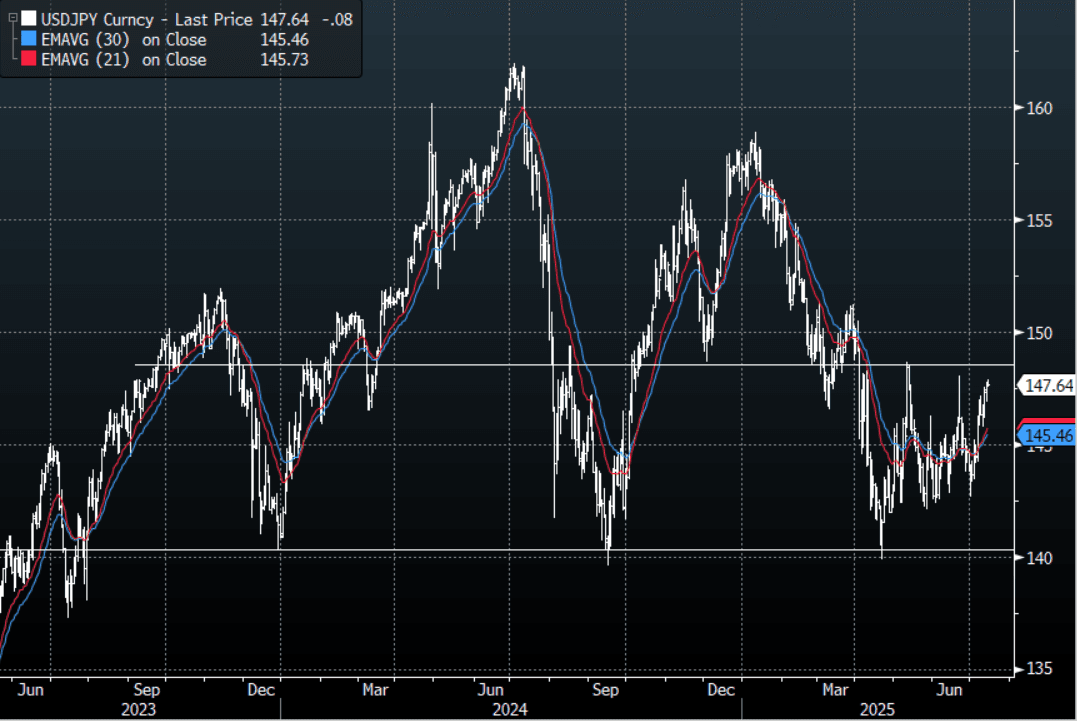

JPY: Asia Wrap - USD/JPY Consolidates Ahead Of US CPI

The Asia-Pac USD/JPY range has been 147.56 - 147.89, Asia is currently trading around 147.65, -0.05%. The pair has traded sideways with little direction, consolidating its recent move higher. The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. Price is now consolidating some of those recent gains, dips back towards 146.00 should now find support first up. The US CPI tonight will be closely watched by the bond market and consequently will also be important for USD/JPY.

- JAPAN Long Dated Yield Surge Continues, With Election Driving Uncertain Outlook: As Japan's upper house elections approach (held July 20), focus remains on the relentless rise in longer-dated JGB yields. The 30yr is up a further +4bps today, last around 3.21%. Concerns around fiscal slippage is a factor in the JGB sell-off.

- Reuters : "Barclays calculates that the rise in 30yr yields currently factors in about a three percentage-point cut to Japan's 10% consumption tax rate. "Even if the ruling parties retain their majority in the upper house, they would still be unable to pass budget bills, including the upcoming supplementary budget, without the cooperation of the opposition parties."

- "JAPAN, EU TO ISSUE JOINT STATEMENT ON ECONOMIC ALLIANCE:YOMIURI" - BBG

- "JAPAN RULING BLOC MAY STRUGGLE FOR MAJORITY: MAINICHI ANALYSIS" - BBG

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 146.50($1.4b July 16).

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

- Data/Event : US CPI

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

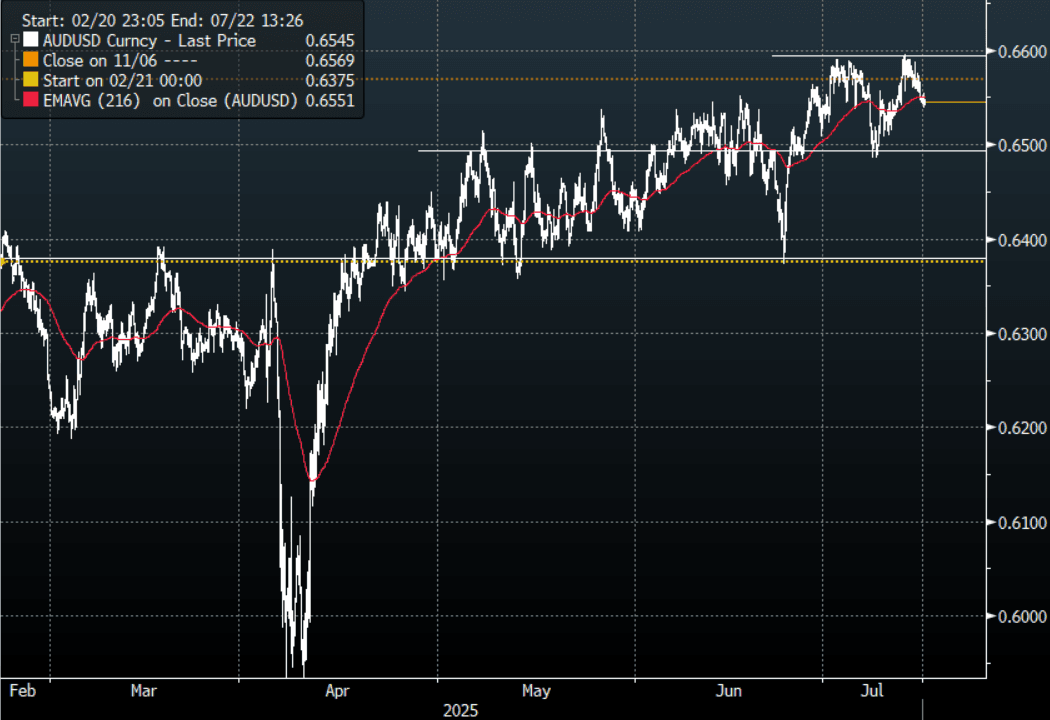

AUD: Asia Wrap - AUD/USD Middle Of The Range, Awaits US CPI

The AUD/USD has had a range of 0.6539 - 0.6555 in the Asia- Pac session, it is currently trading around 0.6545, +0.01%. Risk got a boost this morning as Nvidia posted on a blog that they had received assurances from the US Government that it would be granted licenses to resume sales of its H20 to China. AUD/USD initially tried to bounce on this but has not followed through, it trades in the middle of its recent 0.6500 - 0.6600 range awaiting US CPI tonight.

- Ronald Mizez(AFR) on LinkedIn: The Commonwealth Bank has urged Jim Chalmers to consider major tax reform to revive productivity, including slashing income taxes, overhauling the GST, capping superannuation concessions and introducing wealth taxes.

- The July Westpac consumer confidence index rose 0.6%m/m, putting the index at 93.1 (from 92.6 in June). The edge higher comes despite last week's surprise RBA on hold decision. Sentiment is up from recent lows, but still below recent highs, leaving us within recent ranges.

- The AUD/USD continues to hold above its support around 0.6500, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the market can build on this outperformance and break above 0.6600.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6560(AUD631m), 0.6495(AUD611m),. Upcoming Close Strikes : 0.6575(AUD609m July 16), 0.6480(AUD586m July18), 0.6700(AUD611m July 16).

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

- AUD/JPY - Today's range 96.55 - 96.86, it is trading currently around 96.65, -0.20%. The pair has had a good move above 96.00 and this time looks to be building momentum to extend higher. The market has been caught wrong-footed in both legs of this pair and price action suggests a potential move back to 99.00/100.00. Dips back to 95.50/96.00 should now be supported.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P