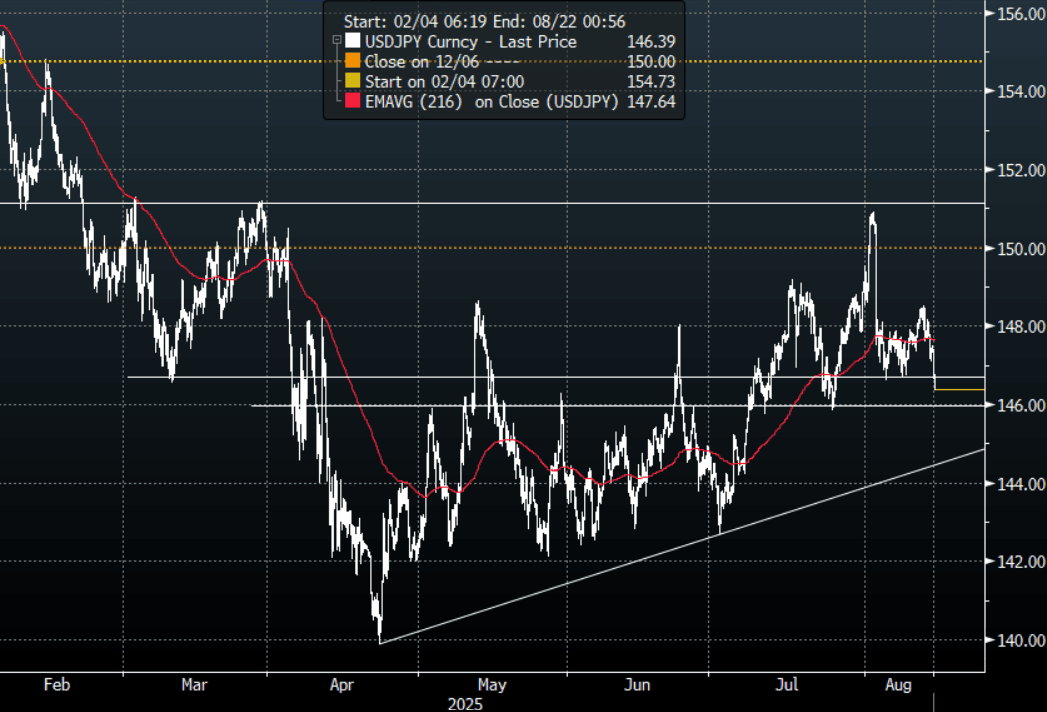

JPY: Asia Wrap - USD/JPY Breaks Below 147.00 On Bessent Comments

The Asia-Pac USD/JPY range has been 146.38-147.42, Asia is currently trading around 146.40, -0.68%. USD/JPY traded heavy for most of the overnight session eventually finding some demand back toward the 147.00 area. Comments from Scott Bessent in a Bloomberg interview then gave it the nudge it needed to break through this demand and extend lower. Price is currently probing the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again.

- “They’re behind the curve,” Bessent told Bloomberg TV on Wednesday, noting that he discussed Japan’s inflation problem with BOJ Governor Kazuo Ueda. “So they’re going to be hiking and they need to get their inflation problem under control,” he added." BBG

- "Hideo Kumano, executive economist at Dai-Ichi Life Research Institute, said "Bessent may be trying to weaken the dollar through his comments on US and Japanese monetary policy," and that by commenting on another country's policy, "he's breaking the rules."

- The most notable underperformer in Asian stocks today are the Japan benchmark indices, with the Topix and the NKY 225 off a little over 1%.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($1.01b), 149.00($1.15b).Upcoming Close Strikes : 145.00($920m Aug 15), 150.00($685m Aug 15), 150.00($846m Aug 19) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

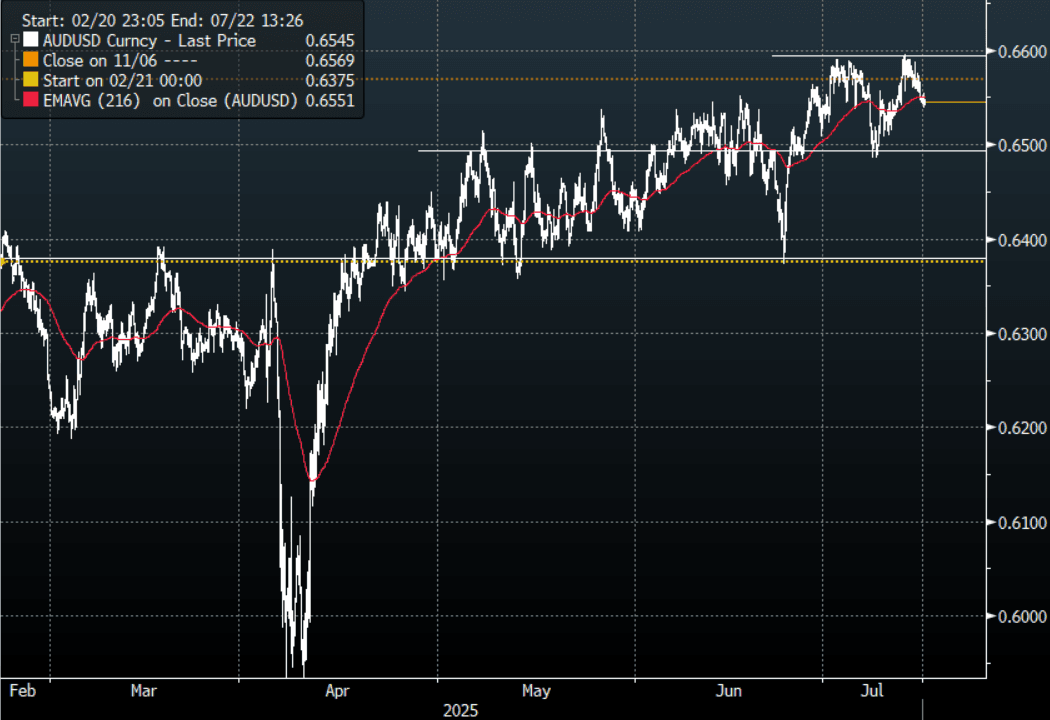

AUD: Asia Wrap - AUD/USD Middle Of The Range, Awaits US CPI

The AUD/USD has had a range of 0.6539 - 0.6555 in the Asia- Pac session, it is currently trading around 0.6545, +0.01%. Risk got a boost this morning as Nvidia posted on a blog that they had received assurances from the US Government that it would be granted licenses to resume sales of its H20 to China. AUD/USD initially tried to bounce on this but has not followed through, it trades in the middle of its recent 0.6500 - 0.6600 range awaiting US CPI tonight.

- Ronald Mizez(AFR) on LinkedIn: The Commonwealth Bank has urged Jim Chalmers to consider major tax reform to revive productivity, including slashing income taxes, overhauling the GST, capping superannuation concessions and introducing wealth taxes.

- The July Westpac consumer confidence index rose 0.6%m/m, putting the index at 93.1 (from 92.6 in June). The edge higher comes despite last week's surprise RBA on hold decision. Sentiment is up from recent lows, but still below recent highs, leaving us within recent ranges.

- The AUD/USD continues to hold above its support around 0.6500, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the market can build on this outperformance and break above 0.6600.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6560(AUD631m), 0.6495(AUD611m),. Upcoming Close Strikes : 0.6575(AUD609m July 16), 0.6480(AUD586m July18), 0.6700(AUD611m July 16).

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

- AUD/JPY - Today's range 96.55 - 96.86, it is trading currently around 96.65, -0.20%. The pair has had a good move above 96.00 and this time looks to be building momentum to extend higher. The market has been caught wrong-footed in both legs of this pair and price action suggests a potential move back to 99.00/100.00. Dips back to 95.50/96.00 should now be supported.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Asia Wrap - Quiet Session Looking Toward CPI

The TYU5 range has been 110-20+ to 110-25 during the Asia-Pacific session. It last changed hands at 110-23, down 0-01 from the previous close.

- The US 2-year yield is trading around 3.898%.

- The US 10-year yield is trading around 4.433%.

- The 10-year yield is again testing the 4.40/45% pivot within its wider 4.10% - 4.65% range. The market is clearly worried about inflation and the CPI this week will be a critical input into the market's thinking. A sustained close back above the 4.45% area could see more longs pared back, above here and the focus will turn back to the 4.65% area.

- Lance Roberts(RIA) - “Tuesday’s CPI and Wednesday’s PPI reports will be very helpful in appreciating how tariffs are impacting inflation. Thus far, there has been a negligible effect. However, the June reports will fully capture a period when the tariffs were being enforced. If data continues to be on the weak side, we suspect the Fed will become more dovish. However, higher-than-expected inflation data may allow them to continue to postpone rate cuts.”

- MNI US OUTLOOK/OPINION: Analysts See Core CPI On Cusp Of 0.2% or 0.3% M/M In June. Ahead of tomorrow’s US CPI release, we note that the broad Bloomberg consensus looks for both core and headline CPI inflation at 0.3% M/M in June although unrounded estimates suggest a risk of rounding lower.

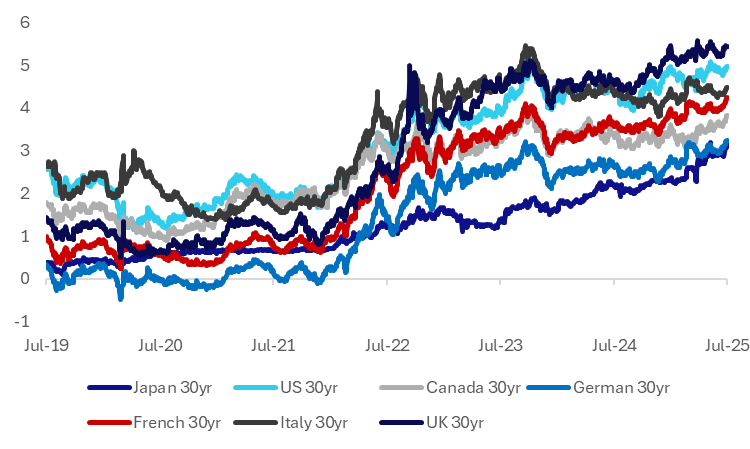

JAPAN: 30yr JGB Yield Correlation With Other G7 Yields Elevated

Fiscal spending concerns are not just present in Japan, but in much of the G7 markets. Pressure points come from the recently passed US tax bill, whilst the UK government is grappling with how to balance spending priorities amid revenue constraints. Germany is also moving away from fiscal restraint, whilst broader EU trends are looking at increased defense spending as well.

- The chart below plots the 30yr government bond yields for these economies. We have mostly been trending higher over the past 6-12 months. Japan, an historical laggard in this space, has now caught up with the level of German 30yr yield levels.

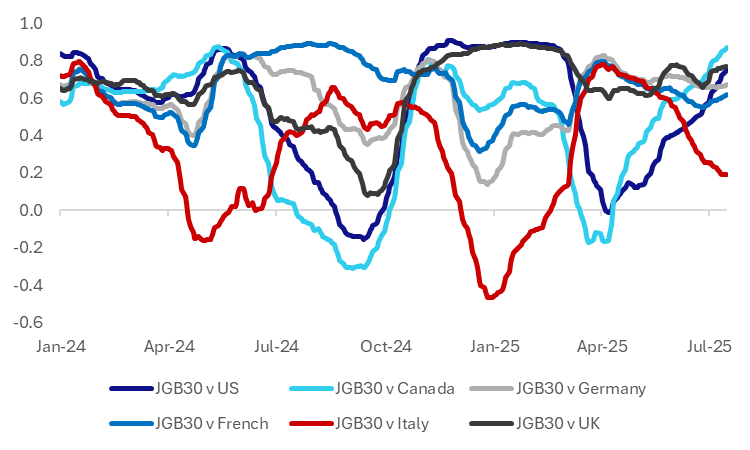

- The second chart presents the correlations between the 30yr JGB yield and those of the rest of the G7. The correlations are presented as a rolling 6 month window.

- Outside of JGB and Italian yields, the correlations have been trending higher of late and sit close to cyclical highs. This provides scope for spill over from high JGB yields and vice versa to Japan from other G7 markets.

Fig 1: G7 30yr Government Bond Yields

Source: Bloomberg Finance L.P./MNI

Fig 2: JGB 30yr Yield Correlations With Other 30yr G7 Yields

Fig 2: JGB 30yr Yield Correlations With Other 30yr G7 Yields