MNI ASIA OPEN: Yields Rise as Weekly/Continuing Claims Improve

EXECUTIVE SUMMARY

- MNI BOE WATCH: Bank Holds Rates But Pares Scale Of Annual QT

- MNI US DATA: Philly Fed Mfg Shows Jump In Activity, Fading Current Inflation

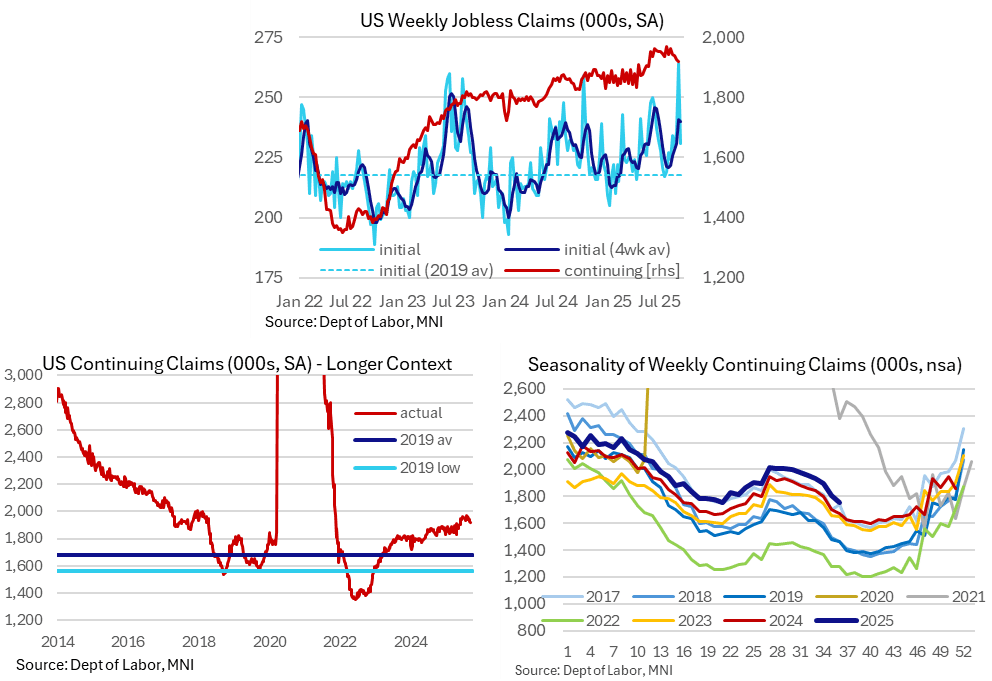

- MNI US DATA: Continuing Claims See A Fourth Consecutive Weekly Decline

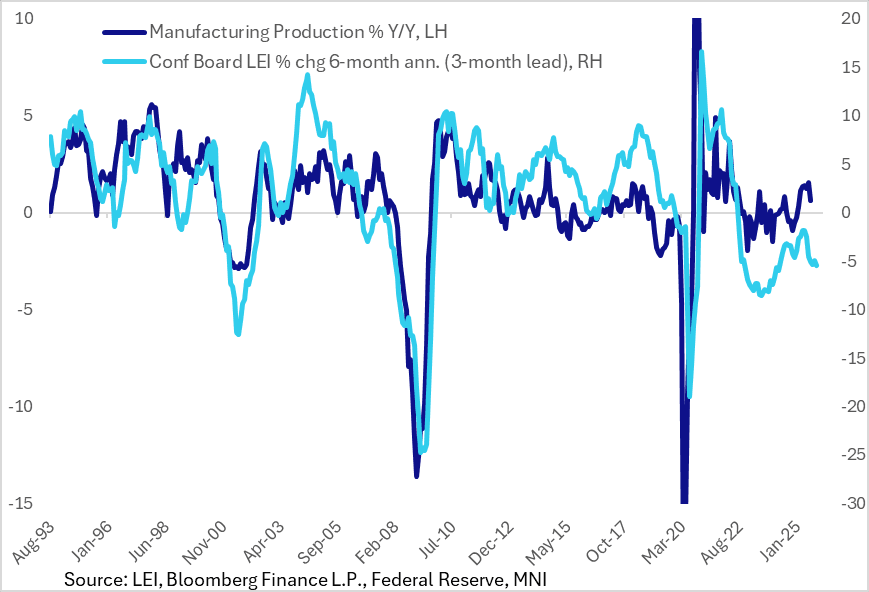

- MNI US DATA: LEI Continues To Stagnate, Pointing To Soft Manufacturing

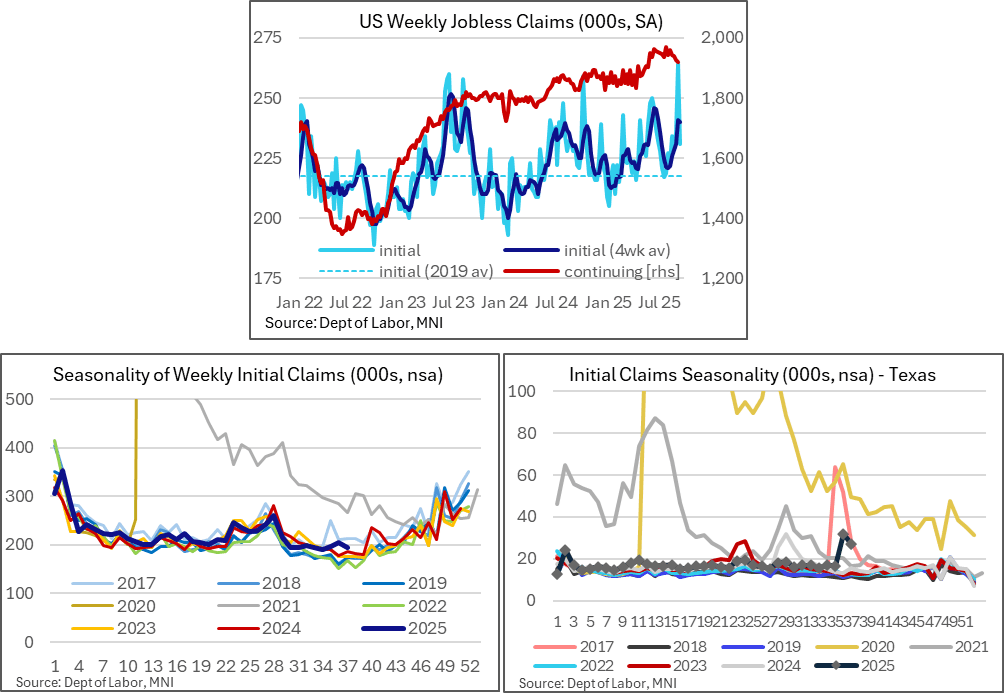

- MNI US DATA: Initial Jobless Claims Surprise Lower, Texas Fraud Still Seems Apparent

US

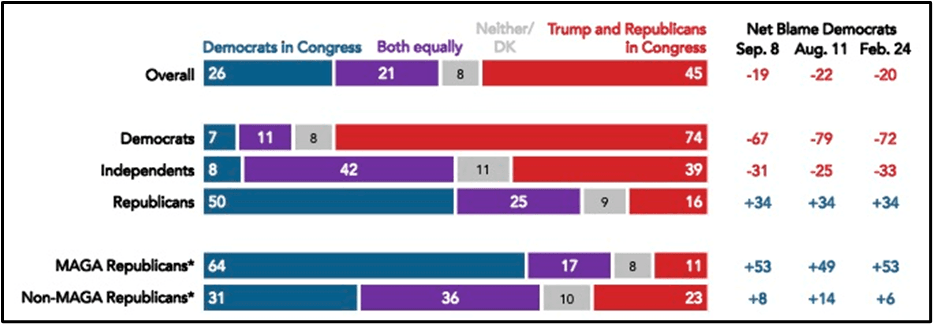

MNI US: Progressive Pollster Indicates GOP Will Take Government Shutdown Blame

Progressive polling outfit Navigator Research is out with new survey data suggesting that Republicans would be held accountable for a government shutdown. Navigator writes, “If the government were to shut down in October, Americans say they would be more likely to blame President Trump and Republicans in Congress than Democrats. 45 percent say they would blame Trump and Republicans, while 26 percent say they would blame Democrats in Congress. Another 21 percent would blame both sides equally.

Source: Navigator Research

NEWS

MNI BOE WATCH: Bank Holds Rates But Pares Scale Of Annual QT

The Bank of England voted to keep Bank Rate at 4% on Thursday, though the Monetary Policy Committee split seven-two, with Swati Dhingrha and Alan Taylor both favouring a further 25-basis-point cut. The MPC also voted to reduce the scale of bonds held for monetary policy purposes by GBP70 billion, which like the rates decision was largely in line with market expectations. The overall annual reduction in the Asset Purchase Facility was cut from the previous year's GBP100 billion, even as active sales are set to increase to GBP21 billion from GBP13 billion.

MNI BRIEF: DOJ Appeals Fed's Cook Firing Case To Supreme Court

The Trump administration Thursday asked the Supreme Court to pause a federal appeals court ruling that allowed Federal Reserve Governor Lisa Cook to continue to serve on the Fed Board, despite President Trump's attempt to fire her. The government argued the district court lacked authority to order Lisa Cook's reinstatement to the Fed and said that so long as the president identifies a cause, the determination of "some cause relating to the conduct, ability, fitness, or competence of the officer" is within the president’s unreviewable discretion.

MNI US-CHINA: Trump-Xi Call To Take Place At 09:00 ET Friday Sept. 19

MNI London: Wires reporting that a call between President Donald Trump and Chinese President Xi Jinping will take place at 09:00 ET 14:00 BST on Friday, Sept. 19. The call is expected to formalise an agreement to keep the video-sharing app TikTok operational in the US by transferring the app to majority US ownership. Beijing is expected to maintain control of the TikTok algorithm, an arrangement that is likely to rankle with China hawks in the Republican Party.

MNI UK: US-Trump/Starmer Presser Talks On Russia, Energy, & Immigration

In the presser between US President Donald Trump and UK PM Sir Keir Starmer, numerous issues raised in the presser: On immigration, Trump says his advice to Starmer would be to 'stop the situation immediately' and 'use the military if necessary'. Starmer says 'there is no silver bullet' on returning illegal immigrants amid legal challenges to deportation exchange flights leaving the UK.

MNI ISRAEL: Spain & German Leaders Meet Amid Divergence Over Possible EU Sanctions

German Chancellor Friedrich Merz travels this evening to Madrid for talks with PM Pedro Sanchez followed be a presser. It marks Merz's first visit to Spain since forming a gov't in May. The trip comes at a time of political tensions within the European Union concerning the prospect of sanctions on members of the Israeli gov't, and the suspension of certain trade-related provisions of the Association Agreement between the EU and Israel as proposed by the European Commission in response to the conflict in Gaza.

US TSYS

MNI US TSYS: Treasury Yields Rising As Weekly Jobless/Continuing Claims Improve

- Treasuries look to finish weaker but off early Thursday lows. Rates traded firmer overnight - paring Wednesday's post-FOMC sell-off - but reversed course/extended lows after better than expected weekly & continuing claims.

- Initial jobless claims were lower than expected at 231k (sa, cons 240k) in the week to Sep 13, a payrolls reference week. It follows a marginally upward revised 264k (initial 263k) in what was a much higher than expected print at the time after a spike in Texas initial claims in what has since been revealed as linked to ID fraud that has increased since Labor Day.

- Continuing claims meanwhile also offer a relatively encouraging report, easing to 1920k (sa, cons 1950k) in the week to Sep 6 after yet another downward revision to 1927k (initial 1939k).

- After the bell the Tsy Dec'25 10Y contract trades -6.5 at 112-29.5 (yld 4.1140% +.0269) vs. 112-23.5 low (113-12 o/n high) - initial technical support at 112-15.5 (High Aug 5 and 14). Curves steeper: 2s10s +.833 at 54.026, 5s30s +2.156 at 105.571.

- Information Technology sector shares led equity indexes run to new highs - namely semiconductor makers after Intel surged nearly 30% to new 52-wk highs of 32.37 after Nvidia (+3.31% - recovering from Wednesday's decline) announced a $5B investment and AI infrastructure collaboration.

- Both the Bank of England vote split and APF reduction were in line with expectations provided little fresh impetus for GBP (-0.51%) on Thursday, allowing cable to suffer from broader dynamics.

OVERNIGHT DATA

MNI US DATA: Initial Jobless Claims Surprise Lower, Texas Fraud Still Seems Apparent

- Initial jobless claims were lower than expected at 231k (sa, cons 240k) in the week to Sep 13, a payrolls reference week. It follows a marginally upward revised 264k (initial 263k) in what was a much higher than expected print at the time after a spike in Texas initial claims in what has since been revealed as linked to ID fraud that has increased since Labor Day.

- There was only partial payback this week from Texas and with no revisions, suggesting there could still be an undue upward bias to the data, although that isn’t hugely surprising as it took a couple weeks for the data to be corrected and revised when Massachusetts reported fraud back in May 2023 (more on that here).

- Specifically, Texas initial claims were most recently reported at 26.9k (-5.0k on the week) having spiked 15.3k to 31.95k (initially reported as 31.91k) the previous week compared to a recent trend in the 16-18k mark. Taking that prior trend as a counterfactual, it very crudely implies about 10-15k of impact from fraud.

MNI US DATA: Continuing Claims See A Fourth Consecutive Weekly Decline

- Continuing claims meanwhile also offer a relatively encouraging report, easing to 1920k (sa, cons 1950k) in the week to Sep 6 after yet another downward revision to 1927k (initial 1939k). It marks a fourth consecutive weekly decline for continuing claims from 1961k in the week to Aug 9, taking it further away from the recent high of 1968k in late July.

- That recent high had pushed just above the 1964k seen back in mid-June after continuing claims pushed notably higher through May-June. Indeed, claims are now at their lowest since May.

MNI US DATA: LEI Continues To Stagnate, Pointing To Soft Manufacturing

The Conference Board's US Leading Economic Index (LEI) fell 0.5% M/M in August, worse than the -0.2% expected but offset by an upward revision to July to +0.1% from -0.1%.

- The upward July revision marked the first positive reading in the index since November 2024 (and prior to that, February 2024). That compares to positive GDP growth throughout the period (with the exception of the trade/inventory related volatility of H1 2025), underlining that the LEI hasn't been particularly useful in recent years in tracking let alone predicting economic activity.

- As we continue to note, the LEI's composition makes it more of an index of manufacturing and, to a lesser extent, financial conditions. As such they captured the contraction in manufacturing construction fairly well for most of 2022-24, and peaked around the same time as manufacturing activity seems to have rebounded (amid tariff-front-running).

- The latest LEI contraction was the biggest since April, largely due to a fall in average weekly hours, weaker ISM new orders, softer consumer expectations, and weaker building permits.

- The lack of upside impetus suggests that there is little upside momentum for industrial growth over the rest of the year.

- MNI: US TSY TICS NET FLOWS IN JUL +$2.1B

- US TSY TICS NET L-T FLOWS IN JUL +$49.2B

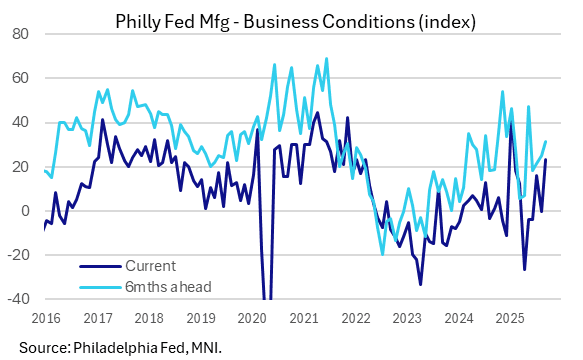

MNI US DATA: Philly Fed Mfg Shows Jump In Activity, Fading Current Inflation

The Philadelphia Fed's regional Manufacturing Business Outlook Survey was much stronger than expected in September, with a rise in the headline General Business Conditions index to 23.2 (-0.3 prior, 1.7 expected) marking the highest level since January. The 6-month ahead outlook rose to 31.5 from 25.0, for a 4-month high, with shipments up to 26.1 (7-month high) from 4.5 and new orders to 12.4 (2-month high) from -1.9. The employment index was little changed at 5.6 (5.9 prior).

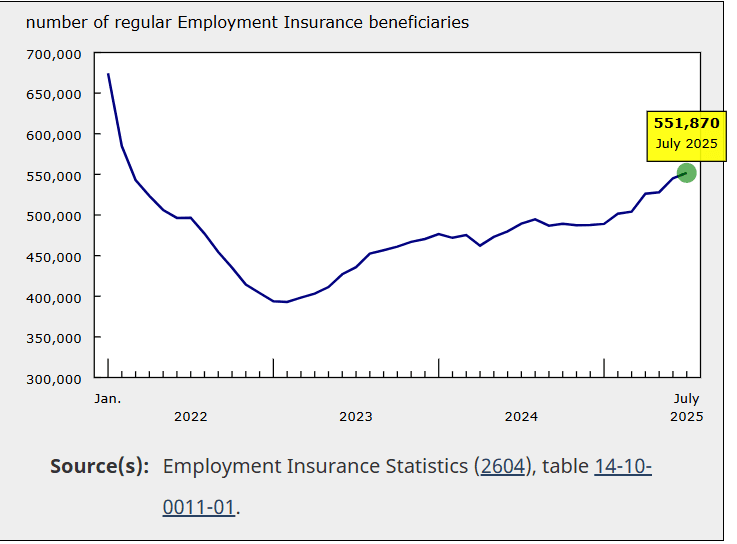

MNI CANADA: Highest Jobless Claims In More Than Three Years

- Regular Employment Insurance beneficiaries +6.6K (+1.2%) to 552K in July, continuing upward trend that began at the start of 2025. From December 2024 to July 2025, beneficiaries increased +64K (+13%).

- BOC cited labor market weakness as it cut interest rate Wed.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 124.1 points (0.27%) at 46142.42

S&P E-Mini Future up 36.5 points (0.55%) at 6695.25

Nasdaq up 209.4 points (0.9%) at 22470.72

US 10-Yr yield is up 2.7 bps at 4.114%

US Dec 10-Yr futures are down 7.5/32 at 112-28.5

EURUSD down 0.003 (-0.25%) at 1.1783

USDJPY up 0.99 (0.67%) at 147.99

WTI Crude Oil (front-month) down $0.38 (-0.59%) at $63.67

Gold is down $14.18 (-0.39%) at $3645.75

European bourses closing levels:

EuroStoxx 50 up 86.97 points (1.62%) at 5456.67

FTSE 100 up 19.74 points (0.21%) at 9228.11

German DAX up 315.35 points (1.35%) at 23674.53

French CAC 40 up 67.63 points (0.87%) at 7854.61

US TREASURY FUTURES CLOSE

3M10Y +2.471, 13.385 (L: 5.582 / H: 15.503)

2Y10Y +0.607, 53.8 (L: 51.355 / H: 54.872)

2Y30Y +1.82, 115.31 (L: 111.216 / H: 116.67)

5Y30Y +1.884, 105.299 (L: 102.066 / H: 106.399)

Current futures levels:

Dec 2-Yr futures down 1.75/32 at 104-10.125 (L: 104-09.25 / H: 104-13.75)

Dec 5-Yr futures down 3.5/32 at 109-15.5 (L: 109-12.5 / H: 109-24.5)

Dec 10-Yr futures down 7.5/32 at 112-28.5 (L: 112-23.5 / H: 113-12)

Dec 30-Yr futures down 25/32 at 116-22 (L: 116-12 / H: 117-30)

Dec Ultra futures down 1-04/32 at 120-4 (L: 119-23 / H: 121-29)

MNI US 10YR FUTURE TECHS: (Z5) Corrective Pullback

- RES 4: 114-16+ 1.0% 10-dma envelope

- RES 3: 114-10 High Apr 7 (cont.)

- RES 2: 114-00 Round number resistance

- RES 1: 113-29 High Sep 11

- PRICE: 113-00 @ 19:51 BST Sep 18

- SUP 1: 112-23+/112-15+ Intraday low / High Aug 5 and 14

- SUP 2: 112-07 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures have traded lower today as the corrective pullback extends, but is off its intraday lows. Price has moved through the 20-day EMA, at 112-28+. The break signals scope for a deeper retracement and attention turns to the 50-day EMA, at 112-07 and the next key support. Moving average studies remain in a bull mode position, highlighting a dominant uptrend. The bull trigger has been defined at 113-29, the Sep 11 high.

US SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.010 at 96.350

Mar 26 -0.020 at 96.580

Jun 26 -0.025 at 96.810

Sep 26 -0.040 at 96.940

Red Pack (Dec 26-Sep 27) -0.045 to -0.04

Green Pack (Dec 27-Sep 28) -0.035 to -0.03

Blue Pack (Dec 28-Sep 29) -0.03 to -0.025

Gold Pack (Dec 29-Sep 30) -0.03 to -0.025

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.38% (-0.01), volume: $2.853T

- Broad General Collateral Rate (BGCR): 4.35% (-0.01), volume: $1.149T

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.01), volume: $1.125T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $96B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $192B

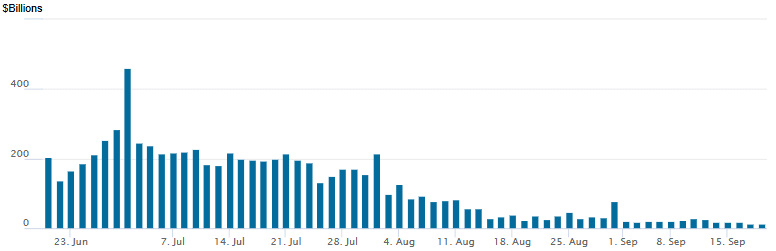

FED Reverse Repo Operation

RRP usage slips to new low of $13.707B with 13 counterparties this afternoon from $13.963B Wednesday, usage at lowest levels since early April 2021. Compared to this year's high usage of $460.731B occurred on June 30.

MNI PIPELINE: Corporate Bond Update: $5B AT&T 4Pt Launched, $5B UBS 5Pt to Follow

- Date $MM Issuer (Priced *, Launch #)

- 09/18 $5B #AT&T $1.15B 7Y +70, $1.25B 10Y +82, $1.1B 20Y +87.5, $1.5B 29Y +100

- 09/18 $5B UBS $1.25B 4.25NC3.25 +60, $700M 4.25NC3.25 SOFR+84, $1B 6NC5 +73, $300M 6NC5 SOFR+106, $1.75B 11.5NC10.5 +90

- 09/18 $1.5B #Credit Agricole 8NC7 +97

- 09/18 $750M #BAT Capital +7Y +85

- 09/18 $750M #Ferguson +5Y +70

- 09/18 $600M #Turk Eximbank 5Y 6.5%

- 09/18 $600M #Atmos Energy 30Y +77

- 09/18 $500M #Wisconsin Energy 5Y +50

MNI BONDS: EGBs-GILTS CASH CLOSE: Bear Steeper As BOE Delivers Expected Hold

European curves bear steepened Thursday.

- Early trade saw limited moves in EGBs and Gilts, with little net impact from the Federal Reserve decision the previous day after the cash close.

- The BOE decision (7-2 vote for a hold) was fully as expected, though there was a bit of twist steepening subsequently seen in the UK curve as the front-end faded a pre-meeting buildup of hawkish positioning.

- Stronger-than-expected US jobless claims data saw a sell-off in Treasuries spill over into Europe.

- In an interview later in the session, BOE's Bailey pointed to ongoing expectations for further rate cuts, while assuaging fears over the impact of QT, helping limit Gilt losses going into the close.

- ECB Vice President de Guindos told an MNI Connect event that the risk of persistent inflation undershooting is not that big.

- The German and UK curves both bear steepened on the day, with little difference in performance. Periphery / semi-core EGB spreads were little changed.

- Friday concludes a busy week for the UK with retail sales and public sector finance data, while we also get French confidence data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 2.011%, 5-Yr is up 2.7bps at 2.306%, 10-Yr is up 5.1bps at 2.726%, and 30-Yr is up 7.9bps at 3.309%.

- UK: The 2-Yr yield is up 0.2bps at 3.961%, 5-Yr is up 2.9bps at 4.103%, 10-Yr is up 5.1bps at 4.676%, and 30-Yr is up 7.7bps at 5.507%.

- Italian BTP spread up 0.7bps at 79.7bps / French OAT up 0.2bps at 80.8bps

MNI FOREX: Greenback Relief Rally Extends Following Strong US Data

- The lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference. This prompted the USD’s bearish momentum to stall on Wednesday and aggressively reverse higher.

- Better-than-expected US jobless claims and philly fed data then bolstered the relief rally Thursday. At its highest point today, USDJPY (+0.70%) recovered by an impressive 278 pips from the post-Fed lows, potentially exacerbated by the lingering political uncertainty in Japan, the close proximity to the BOJ meeting Friday and a bullish reversal signal on the chart.

- The New Zealand dollar is the standout underperformer in the G10 space, following a particular weak set of Q2 GDP data overnight. The much weaker-than-expected growth figures have weighed heavily on the Kiwi, currently down 1.4% as we approach the APAC crossover, placing the renewed short-term focus on pivot support at the 0.5800 mark.

- The NZ data trumped the weaker-than-expected August employment change figure out of Australia, which has notably allowed AUDNZD to extend its impressive rally from the April lows to ~5.9%.

- Price action today has seen the cross rise above 1.12 for the first time since late 2022 and steady appreciation saw spot eclipse the next target for the move of 1.1250, the 76.4% Fibonacci retracement of the 2022 price swing. Above here, resistance appears scant until the 2022 highs, located at 1.1491.

- Both the Bank of England vote split and APF reduction coming in line with expectations provided little fresh impetus for GBP (-0.51%) on Thursday, allowing cable to suffer from broader dynamics. A bullish theme for cable remains intact and the move down from Wednesday’s high is considered corrective at this juncture, with a deeper retracement potentially allowing an overbought condition to unwind. Initial firm support to watch is 1.3492, the 50-day EMA.

- Aside from the BOJ decision and press conference, UK and Canadian retail sales highlight Friday’s data calendar.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 19/09/2025 | 0600/0700 | *** | Public Sector Finances | |

| 19/09/2025 | 0600/0700 | *** | Retail Sales | |

| 19/09/2025 | 0600/0800 | ** | PPI | |

| 19/09/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 19/09/2025 | 1005/1205 | ECB Lagarde and Cipollone at Eurogroup ECOFIN Meeting | ||

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1230/0830 | ** | Retail Trade | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 19/09/2025 | 1830/1430 | San Francisco Fed's Mary Daly |