UK: US-Trump/Starmer Presser Talks On Russia, Energy, & Immigration

Sep-18 14:41

In the presser between US President Donald Trump and UK PM Sir Keir Starmer, numerous issues raised in the presser:

- On immigration, Trump says his advice to Starmer would be to 'stop the situation immediately' and 'use the military if necessary'. Starmer says 'there is no silver bullet' on returning illegal immigrants amid legal challenges to deportation exchange flights leaving the UK.

- On energy policy, Starmer says, 'I am determined to ensure the cost and price of energy comes down'. Starmer: 'The mix will include oil and gas for many years to come'. Starmer defends renewables investment, Trump calls wind energy 'a joke'.

- On Russia, Trump says again Putin has let him down, but says it 'Does not affect the United States'. Reiterates the claim that the war would not have happened if he were president in 2022. Starmer says "We have to put extra pressure on Putin, its only when [Trump] has put pressure on Putin that he has acted". Raises "recklessness" of Putin in hitting British Council and EU buildings in Kyiv

- Trump says the US wants Bagram Air Base in Afghanistan back from the Taliban, claiming that it is "hours away from where China makes its nuclear weapons."

- On the recognition of a Palestinian state, Trump says it is one of the few areas where he disagrees with Starmer.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Aug20 NY cut 1000ET (Source DTCC)

Aug-19 14:34

- EUR/USD: $1.1550(E915mln), $1.1600(E854mln), $1.1660-75(E1.4bln)

- USD/JPY: Y147.25-35($982mln), Y148.00-10($1.5bln)

- USD/CAD: C$1.3800($1.1bln), C$1.3835-55($872mln)

- USD/CNY: Cny7.1050($500mln)

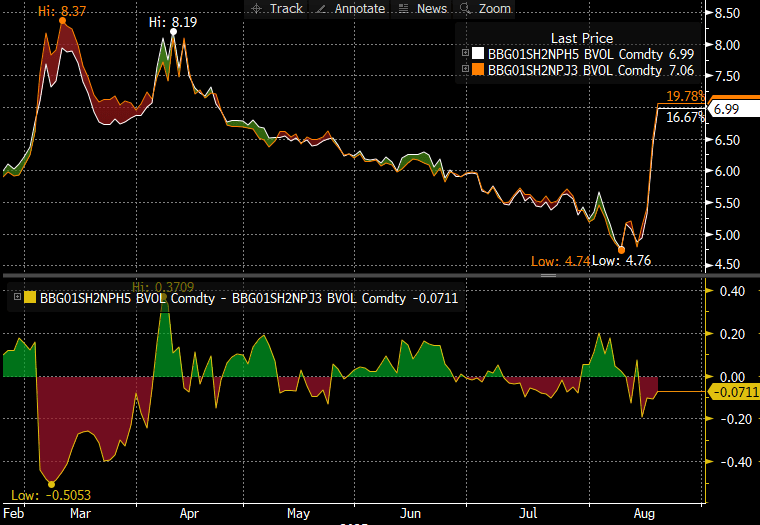

BUNDS: Implied Vol Surges as Markets May be Looking to Cover Short Bund Calls

Aug-19 14:34

- Bund vols have surged to start this week, with implied sharply higher over the Sep-25 future to rise to levels last seen in late April, despite generally subdued trade in the underlying (see chart below).

- Anecdotally, desks report sizeable short positioning in 129.50 Sep-25 calls, with sizeable buying of 15-20k contracts toward the tail-end of last week likely responsible for the surge in vol. Additionally, given the OTC nature of the market, other pricing sources see implied vols marked lower: between 5.25 - 5.75%.

- Bund risks into the futures expiry (September 8) include the following:

- a) a potential extension of core FI steepening trends, movers could include the Eurozone data released over the next two weeks (flash PMIs, August inflation).

- b) any feedthrough from this week's Jackson Hole conference, that could be either in terms of Fed's Powell rowing against an expected September cut, or ECB's Lagarde giving any indication of a final cut in the cycle happening or not.

- c) headline flow from talks on the Russia - Ukraine conflict, with a sustainable peace deal likely bolstering risk-on moves.

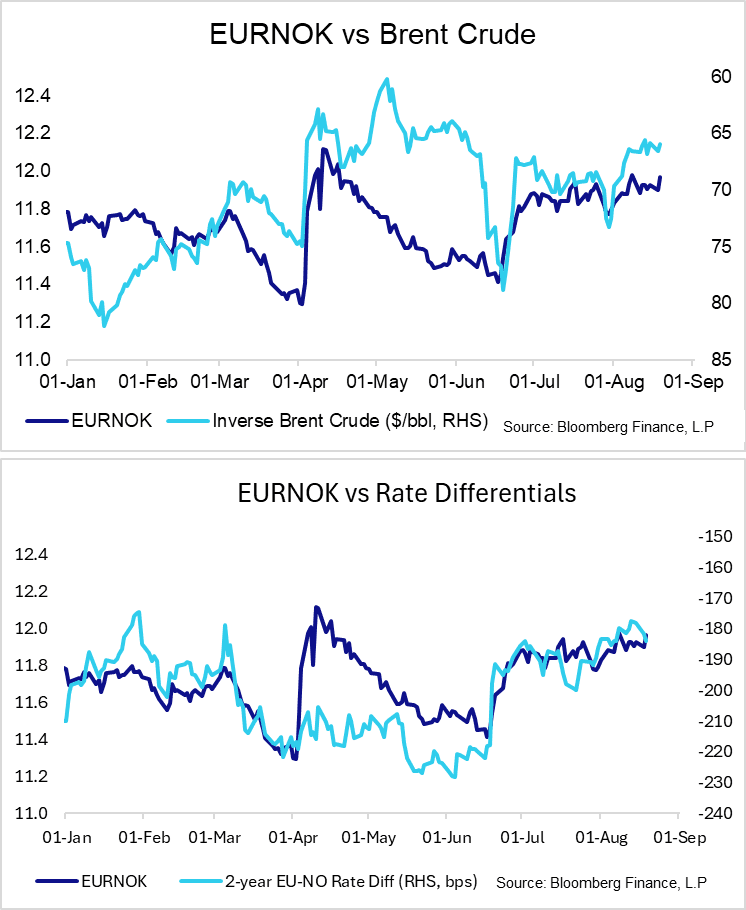

NOK: EURNOK Extending Higher, Narrowing Gap To Resistance

Aug-19 14:31

EURNOK is extending higher, with the krone now comfortably underperforming the G10 basket intraday. We haven't seen an obvious driver for this afternoon’s NOK weakness, which comes despite a 2bp intraday tightening in 2-year EUR-NOK swap rate differentials.

- EURNOK is 0.6% higher at 11.9725, narrowing the gap to resistance at 11.9895 (Aug 8 high). This level shields the psychological 12.0000 handle, which the cross has been unable to sustainably consolidate above on several occasions since 2023.

- A reminder that last week's Norges Bank decision saw rates held at 4.25% and the June guidance retained almost verbatim. Although the communication lacked a clear signal for a September cut, it certainly didn’t rule out such a move. The Committee seems quite content in keeping its options open.

- Q2 GDP is due on Thursday morning, and will be one important input into the September decision and feed into the updated MPR rate path projection. Mainland GDP is expected at 0.3% Q/Q, which is line with Norges Bank's June MPR projection. Q1 mainland GDP was a solid 1.0% Q/Q, driven by household consumption and investment.