US TSYS: Treasury Yields Rising As Weekly Jobless/Continuing Claims Improve

Sep-18 20:03

- Treasuries look to finish weaker but off early Thursday lows. Rates traded firmer overnight - paring Wednesday's post-FOMC sell-off - but reversed course/extended lows after better than expected weekly & continuing claims.

- Initial jobless claims were lower than expected at 231k (sa, cons 240k) in the week to Sep 13, a payrolls reference week. It follows a marginally upward revised 264k (initial 263k) in what was a much higher than expected print at the time after a spike in Texas initial claims in what has since been revealed as linked to ID fraud that has increased since Labor Day.

- Continuing claims meanwhile also offer a relatively encouraging report, easing to 1920k (sa, cons 1950k) in the week to Sep 6 after yet another downward revision to 1927k (initial 1939k).

- After the bell the Tsy Dec'25 10Y contract trades -6.5 at 112-29.5 (yld 4.1140% +.0269) vs. 112-23.5 low (113-12 o/n high) - initial technical support at 112-15.5 (High Aug 5 and 14). Curves steeper: 2s10s +.833 at 54.026, 5s30s +2.156 at 105.571.

- Information Technology sector shares led equity indexes run to new highs - namely semiconductor makers after Intel surged nearly 30% to new 52-wk highs of 32.37 after Nvidia (+3.31% - recovering from Wednesday's decline) announced a $5B investment and AI infrastructure collaboration.

- Both the Bank of England vote split and APF reduction were in line with expectations provided little fresh impetus for GBP (-0.51%) on Thursday, allowing cable to suffer from broader dynamics.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Redirects Focus Higher

Aug-19 20:00

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1 and a bull trigger

- PRICE: 1.3855 @ 16:34 BST Aug 19

- SUP 1: 1.3763/22 20-day EMA / Low Aug 22

- SUP 2: 1.3576 Low Jul 23

- SUP 3: 1.3557/40 Low Jul 3 / Low Jun 16 and the bear trigger

- SUP 4: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

A bear threat in USDCAD remains present, despite today’s recovery. A break of 1.3879, the Aug 1 high, would cancel a bear threat and resume the recent bull cycle. Downside focus is on support around the 20-day EMA, at 1.3763. A clear break of this EMA would resume the correction off the early August high. This would expose 1.3576, the Jul 23 low. Key medium-term support and the bear trigger lies at 1.3540, the Jun 16 low.

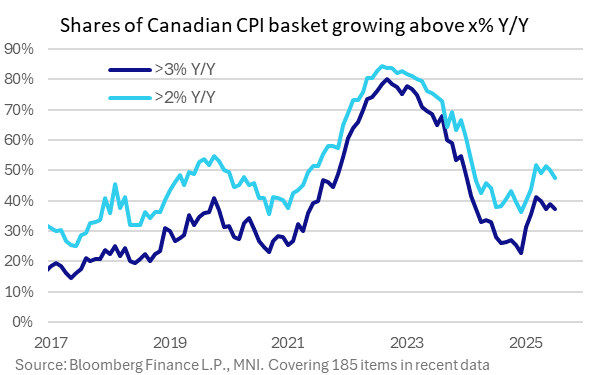

CANADA DATA: Inflation Breadth Narrows Slightly In July Report

Aug-19 19:47

MNI's estimates of inflationary "breadth" showed narrower price pressures in the July Canada CPI report.

- The percentage of CPI categories rising by more than 2% (looking at 185 CPI basket items) fell to 47.6% from 50.3% prior, for the narrowest since February.

- The % above 3% fell back to May's level, at 37.3%, from 38.9% prior. The proportion rising by more than 4% however remained unchanged at 30.3%.

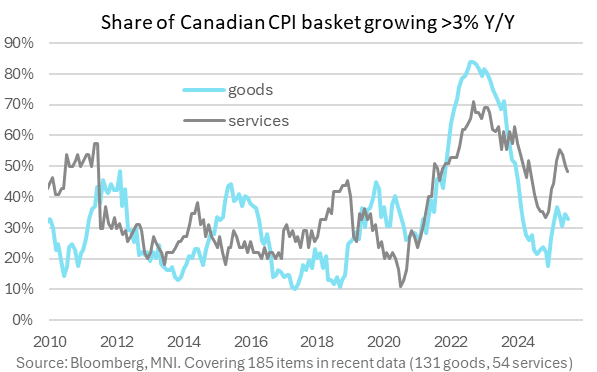

- Both goods and services breadth narrowed, with goods rising 2+% at 30.3% (31.4% prior, 3-month low) and services 17.3% (18.9% prior, 5-month low).

- Traditionally, the >3% breadth metric has been most closely tracked by the BOC in terms of gauging broad inflation pressures, and while this remains uncomfortably high it appears to be on the way down.

US TSYS: Early Support From Soft US Build Permits & Canadian CPI Data

Aug-19 19:30

- Treasuries look to finish near late Tuesday session highs (TYU5 +8.5 at 111-25), curves bull flattening with bonds outperforming (2s10s -2.245 at 54.607, 5s30s -.571 at 107.952).

- Rates rebounded after this morning's data - lower than expected build permits outweighing higher than expected housing starts, while softer Canadian CPI aggregates added to support.

- Housing starts were far stronger than expected in July at 1428k (saar, cons 1297k) after an upward revised 1358k (initial 1321k) in June. It left starts rising 5.2% M/M (cons -1.8%) after a stronger than first thought 5.9% (initial 4.6%) as they bounced after a -8.3% M/M decline in May (also revised from -9.7%).

- Canadian all-items CPI rose 1.73% Y/Y unrounded (1.86% prior, 1.8% expected by MNI median), and 0.12% M/M (0.18% prior, 0.4% expected).

- US$ rising to one week highs, price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Stocks in retreat (Nasdaq -323.04 at 21306.66) ahead of Wednesday's July FOMC minutes not to mention Friday's annual economic symposium in Jackson Hole Wyoming.