MNI ASIA OPEN: Strong Labor Market Saps Larger Rate Cut Hopes

EXECUTIVE SUMMARY

- MNI BRIEF: Less Guidance On Slow Tariff Passthrough- Bostic

- MNI FED: Atlanta's Bostic: "No Time For Significant Shifts" In Policy

- MNI US: Rule Vote On OBBB Passes 219-213 As Conservative Holdouts Offer Backing

- MNI US DATA: Stabilization In ISM Services, But Tariff Impact Still Looms Large

- MNI US DATA: Solid Unemployment Fall Amid Continued Decline In Participation

US

MNI FED: Atlanta's Bostic: "No Time For Significant Shifts" In Policy

Atlanta Fed President Bostic largely reiterates previous commentary on current monetary policy (including at Monday's MNI event) in a speech in Frankfurt (link): "A period characterized by such widespread uncertainty is no time for significant shifts in monetary policy." "That is especially the case against the backdrop of a still resilient macroeconomy, which offers space for patience."

MNI BRIEF: Less Guidance On Slow Tariff Passthrough- Bostic

Atlanta Federal Reserve President Raphael Bostic said Thursday the tariff rollout will likely cause a slow, incremental impact on prices and the back-and-forth makes it difficult to provide guidance on borrowing costs. "That uncertainty is going to sort of weigh in a host of different ways," he said in Q&A at an event in Frankfurt, Germany. "I'm happy to be patient," he added about the monetary policy outlook. Tariff uncertainty is one reason why "we are not doing a lot of forward guidance," he said. "Guidance would not really be helpful or useful in giving people a sense of what we might do."

NEWS

MNI US: Rule Vote On OBBB Passes 219-213 As Conservative Holdouts Offer Backing

Conservative holdouts among House Republicans flipped their support on a rule vote, ensuring passage by a 219-213 margin. The final vote is expected at 08:00ET (13:00BST, 14:00ET). With the passage of the rule vote, there is now little jeopardy ahead of the final vote, with its passage all-but-assured.

MNI SOUTH KOREA: Lee Holds First Call w/NATO Sec-Gen, Looks To Deepen Defence Links

(MNI) London - President Lee Jae-myung held his first phone call with NATO Secretary General Mark Rutte earlier today, where the two discussed the prospect of deepening the partnership on defence between Seoul and the Atlantic alliance, according to the president's office. As one of NATO's 'Indo-Pacific Four', alongside Japan, Australia and New Zealand, Lee was invited to the NATO summit in late June. However, he did not attend.

US TSYS

MNI US TSYS: Yields Rebound on Strong June Jobs Gain, Dip in Unemployment

- Treasuries are broadly weaker into the early pre-holiday close, off this morning's post employment data lows - rates hold a rather narrow range after the initial knee-jerk sell-off.

- Brief two-way after the final data for the session, ISM Services Prices Paid & Employment slightly lower, New Orders higher while Factory/Durables Orders are in-line. slightly lower than expected S&P Global Services PMI, Composite near in-line.

- Currently, Sep'25 10Y trades -13 at 111-07 (110-31L / 111-28H). Through first key support at 111.08.5 (the 20-day EMA), next 110-30+ 50-day EMA, followed by 110-16 (Low Jun 20). Curves bear flatten: 2s10s -3.682 at 45.321; 5s30s -4.441 at 89.048. 10Y yield tapped 4.3576% high finished at 4.3457%.

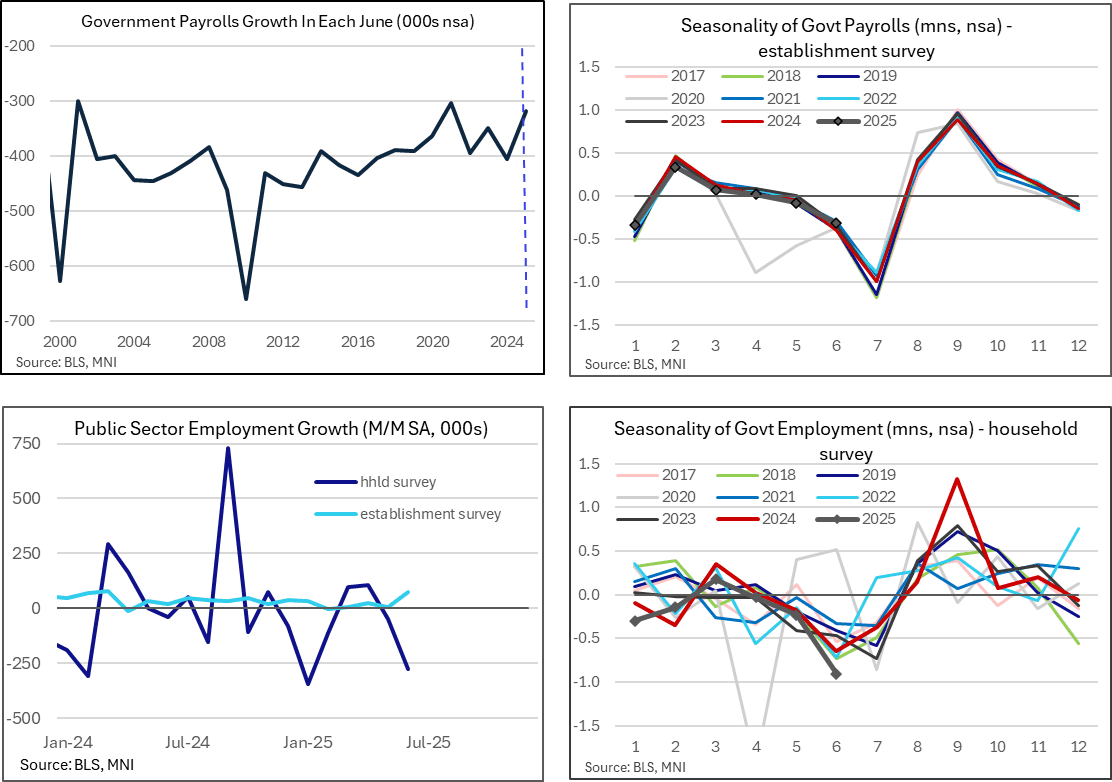

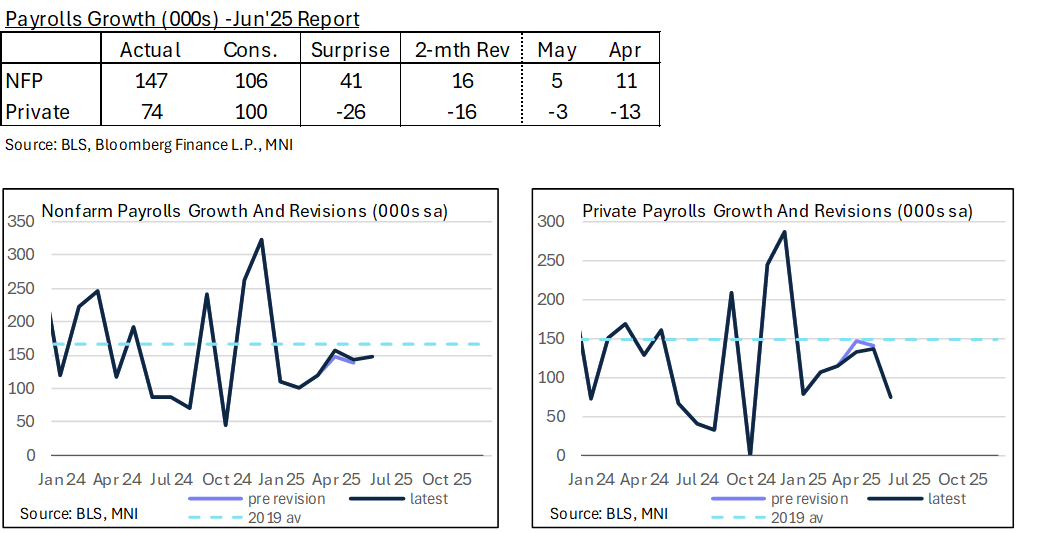

- A 46k beat for NFPs in June (147k vs cons 106k) vs a 26k miss for private payrolls (74k vs cons 100k). The difference being government payrolls surging by 73k for the largest increase since Mar 2024. It comprised of -7k for federal (still weak after DOGE cuts earlier this year) but state +47k and local +33k.

- The major downside surprise in the unemployment rate (4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus) came with a drop of 222k in the number of unemployed (the largest drop of the year) after 4 consecutive rises.

- Projected rate cut pricing significantly cooler vs. this morning's pre-data (*) levels: Jul'25 at -1.2bp (-6.3bp), Sep'25 at -19.1bp (-30.1bp), Oct'25 at -34.2bp (-47.3bp), Dec'25 at -51.8bp (-67bp).

OVERNIGHT DATA

MNI US DATA: Question Marks Of Strength Of Government Payrolls In June

As noted at the time, government payrolls growth was surprisingly strong in June at a seasonally adjusted 73k for the largest increase since Mar 2024. It follows an average of just 8k in Feb-May early on in DOGE efforts to reduce federal headcount.

- It comprised of -7k for federal (still weak after an average -16k in the four months prior) but state in particular jumped 47k (strongest since Jan 2023) whilst local also increased 33k (strongest since Mar 2024). Education played a big role, worth +40k for state and +23k for local.

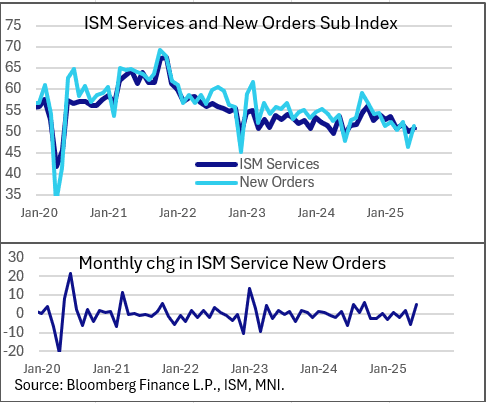

MNI US DATA: Stabilization In ISM Services, But Tariff Impact Still Looms Large

June's ISM Services report was mixed, with prices, activity and new orders stabilizing after a worrying May, but employment and order backlogs notably soft as inventories continued to grow. Tariffs continued to cast a shadow over the survey, with anecdotes appearing more wary of the demand outlook than suggested by the improvement in the major aggregates.

- The headline index rose 0.9 points to 50.8 (consensus 50.6), ending a brief 1-month period in sub-50 territory for the 11th month in 12 at 50-plus. The main standouts on the positive side were in new orders, jumping 4.9 points to 51.3 (consensus 48.2) and reversing most of May's surprising weakness, and in new export orders, rising 2.6 points to 51.1 for the first 50+ reading since February as tariff concerns began to ramp up.

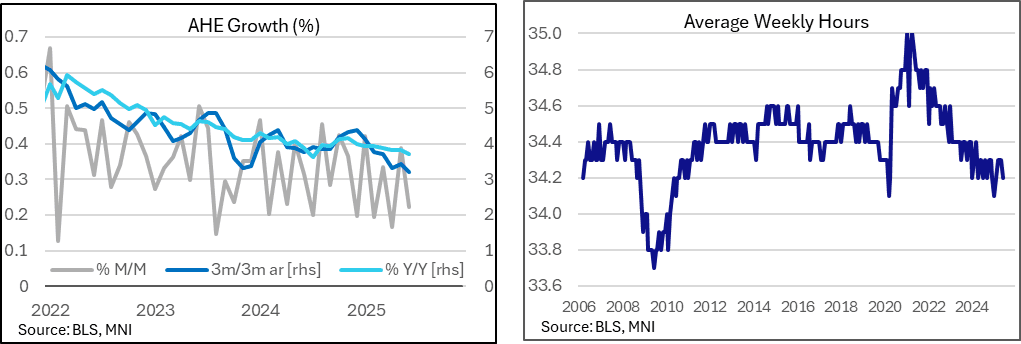

MNI US DATA: Softer Than Expected Wages And Hours Side Of Establishment Survey

The earnings side of the establishment survey surprised weaker in June, from both wages and average hours worked, chiming with some softer private sector payrolls. Average hourly earnings growth was softer than expected in June at 0.22% M/M (cons 0.3) although there had been a mild dovish skew to analyst forecasts. Downward revisions added to this softer take from the earnings side of the establishment survey – see details below.

MNI US DATA: Strong Government Job Creation Hides Weaker Private Sector

A 46k beat for NFPs in June (147k vs cons 106k) vs a 26k miss for private payrolls (74k vs cons 100k). The difference being government payrolls surging by 73k for the largest increase since Mar 2024. It comprised of -7k for federal (still weak after DOGE cuts earlier this year) but state +47k and local +33k.

- The government also led positive two-month revisions. Total non-farm payrolls were revised 16k higher (5k in May and 11k in April) but private payrolls were revised -16k (-3k in May and -13k in April).

- The difference sees nonfarm payrolls averaging 150k over the latest three months, comfortably above long-run breakeven estimates thought to be around 100k, although with private payrolls less elevated at 115k.

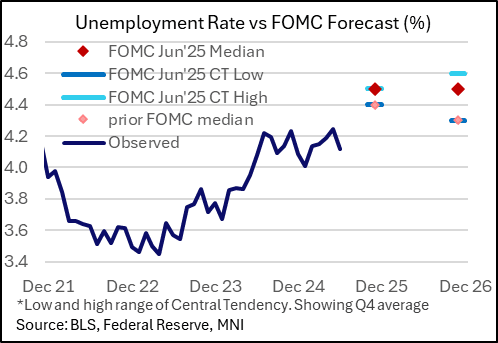

MNI US DATA: Solid Unemployment Fall Amid Continued Decline In Participation

June's Household Survey was healthier than expectations on most fronts, with the key exception of a continued decline in the size of the labor force and participation suggesting diminishing labor supply.

- The major downside surprise in the unemployment rate (4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus) came with a drop of 222k in the number of unemployed (the largest drop of the year) after 4 consecutive rises. This suggests a faster-than-expected deterioration will be required for the final 6 months of the year to reach the FOMC's June Q4 median projection of 4.5%.

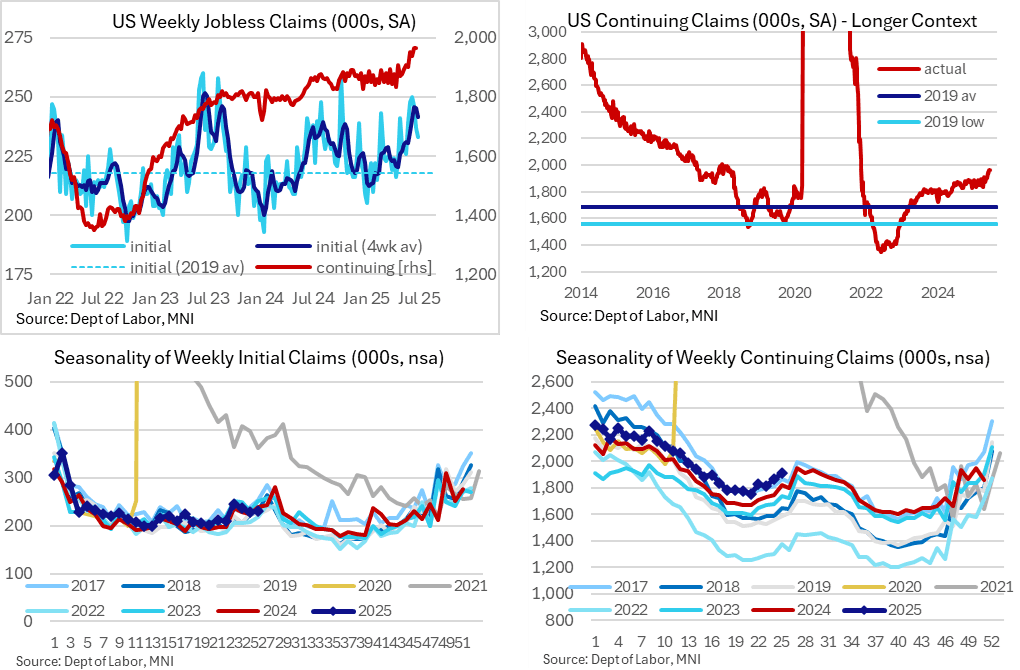

MNI US DATA: Jobless Claims Data Don’t Rock The Boat

The latest weekly jobless claims data point to another small dip in initial claims even if the four-week average remains elevated whilst continuing claims unsurprisingly held at highs since late 2021. It continues to broadly point to a ‘low firing, low hiring’ labor market with the pace of deterioration slowing a touch compared to recent weeks.

- Initial jobless claims were lower than expected at 233k (sa, cons 241k) in the week to Jun 28 after a marginally upward revised 237k, marking a third consecutive decline.

- The four-week average eased lower to 242k, a second weekly decline having recently peaked at 246k at what had been the highest since Aug 2023, although it’s still elevated by recent standards.

- Continuing claims meanwhile were as expected at 1964k (sa, cons 1962k) in the week to Jun 21 after a slightly downward revised 1964k (initial 1974k).

- In non-seasonally adjusted terms, initial claims remain within typical ranges for the time of year whilst continuing claims are right at the top end.

MNI CANADA DATA: Canada's May Trade Balance -CAD5.9B Vs Apr Record -CAD7.6B

- Canada May trade balance narrowed to -CAD5.9B from record -CAD7.6B in April.

- Exports +1.1% MOM after prior -11%; Imports -1.6% MOM, third straight monthly decline.

- Non-U.S. exports +5.7% to record high, share of Canada exports to U.S. near record low of 68%.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 344.11 points (0.77%) at 44828.53

S&P E-Mini Future up 49.25 points (0.78%) at 6324.25

Nasdaq up 208 points (1%) at 20601.1

US 10-Yr yield is up 6.9 bps at 4.3457%

US Sep 10-Yr futures are down 13.5/32 at 111-6.5

EURUSD down 0.0049 (-0.42%) at 1.175

USDJPY up 1.4 (0.97%) at 145.06

WTI Crude Oil (front-month) down $0.4 (-0.59%) at $67.04

Gold is down $28.42 (-0.85%) at $3329.10

European bourses closing levels:

EuroStoxx 50 up 24.43 points (0.46%) at 5343.15

FTSE 100 up 48.51 points (0.55%) at 8823.2

German DAX up 144.02 points (0.61%) at 23934.13

French CAC 40 up 16.13 points (0.21%) at 7754.55

US TREASURY FUTURES CLOSE

3M10Y +4.765, -1.577 (L: -11.53 / H: 0.964)

2Y10Y -3.042, 45.961 (L: 43.465 / H: 50.14)

2Y30Y -3.813, 97.519 (L: 93.006 / H: 103.326)

5Y30Y -1.115, 92.374 (L: 86.742 / H: 95.284)

Current futures levels:

Sep 2-Yr futures down 6.125/32 at 103-21.875 (L: 103-19.625 / H: 103-29.75)

Sep 5-Yr futures down 10/32 at 108-11 (L: 108-04.25 / H: 108-25.75)

Sep 10-Yr futures down 14/32 at 111-6 (L: 110-31 / H: 111-28)

Sep 30-Yr futures down 15/32 at 114-7 (L: 113-31 / H: 115-11)

Sep Ultra futures down 22/32 at 117-19 (L: 117-13 / H: 119-05)

MNI US 10YR FUTURE TECHS: (U5) Support Holds

- RES 4: 113-07 76.4% retracement of the Apr 7 - 11 bear leg

- RES 3: 112-23 High May 1 and key resistance

- RES 2: 112-12+/15 High Jul 1 / 61.8% of the Apr 7 - 11 sell-off

- RES 1: 111-28 High Jul 3

- PRICE: 111-06 @ 16:55 BST Jul 03

- SUP 1: 110-30+ 50-day EMA

- SUP 2: 110-16 Low Jun 20

- SUP 3: 110-10+ Low Jun 16

- SUP 4: 110-03 76.4% of the May 22 - Jul 1 bull leg

A bull cycle in Treasury futures is intact, particularly as the intraday pressure Thursday saw price bounce off 50-day EMA support. Nonetheless, prices remain below Tuesday’s high and today’s sell-off marks an extension of the short-term correction. Support to watch is 110-30+, the 50-day EMA. A clear break of this average would signal scope for a deeper correction and also highlight a possible reversal. For bulls, a move higher would refocus attention on 112-15, the 61.8% retracement of the Apr 7 - 11 steep sell-off.

SOFR FUTURES CLOSE

Sep 25 -0.120 at 95.870

Dec 25 -0.140 at 96.160

Mar 26 -0.125 at 96.415

Jun 26 -0.105 at 96.635

Red Pack (Sep 26-Jun 27) -0.085 to -0.05

Green Pack (Sep 27-Jun 28) -0.045 to -0.04

Blue Pack (Sep 28-Jun 29) -0.045 to -0.04

Gold Pack (Sep 29-Jun 30) -0.04 to -0.04

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.40% (-0.04), volume: $2.882T

- Broad General Collateral Rate (BGCR): 4.37% (-0.02), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.37% (-0.02), volume: $1.104T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $129B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $268B

FED Reverse Repo Operation:

RRP usage slips to $214.665B this afternoon from $237.307B yesterday, total number of counterparties at 45. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to yesterday's (July 1) $460.731B highest usage since December 31.

MNI PIPELINE: Corporate Bond Roundup: $17.5B Priced Monday-Wednesday

No new issuance on Thursday's shortened pre-holiday session, $4B Priced Wednesday, $17.5B/wk:

- Date $MM Issuer (Priced *, Launch #)

- 07/02 $2.2B *SoftBank Group $500M 3.75Y 6.5%, $600M 5.5Y 6.875%, $600M 7 Y 7.25%, $500M 10Y 7.5% (in addition to 3 Eur tranches: 4.25Y, 6Y & 8Y) Note, SoftBank Corp issued $1B over 2 tranches on Monday.

- 07/02 $800M *Korea Gas $300M 3Y SOFR+65, $500M 5Y +47

- 07/02 $800M *National Bank of Kuwait PerpNC6 6.375%

- 07/02 $500M *HIKMA Pharmaceuticals 5Y +135a

- 07/02 $500M *Qatar Insurance NC6 6.15%

MNI BONDS: EGBs-GILTS CASH CLOSE: Yields Pull Back Despite Strong Data

European yields fell in a bull flattening move Thursday, shrugging off a stronger-than-expected US employment report.

- Bunds and Gilts were stronger in early trade, recovering some of the ground lost after Wednesday's UK fiscal panic-related selloff and despite notable French/Spanish bond supply and an upward revision to Eurozone and UK final PMIs.

- US nonfarm payrolls came in above consensus with the unemployment rate unexpectedly falling, pushing yields sharply higher, but the move reversed over the rest of the afternoon into the cash close.

- The German and UK curves both bull flattened, with Gilts outperforming after Wednesday's sizeable underperformance.

- Periphery/semi-core EGB spreads were mixed, with BTPs outperforming and OAT spreads widening slightly.

- Friday's calendar includes German factory orders and French/Spanish industrial production data, along with appearances by ECB's Elderson and Villeroy, as well as BOE's Taylor.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.9bps at 1.834%, 5-Yr is down 4.1bps at 2.142%, 10-Yr is down 4.9bps at 2.615%, and 30-Yr is down 4bps at 3.077%.

- UK: The 2-Yr yield is down 4bps at 3.841%, 5-Yr is down 6.2bps at 3.98%, 10-Yr is down 7bps at 4.542%, and 30-Yr is down 8.2bps at 5.338%.

- Italian BTP spread down 1.6bps at 83.4bps / French OAT up 0.3bps at 66.1bps

FOREX

MNI FOREX: USD Remains Stronger on NFP, but Gains Fading Fast

- The USD is holding the bulk of the post-payrolls gains, with JPY, NZD and CHF among the hardest hit - as identified by the run-up in vols headed into today's print. Infitting with straddle pricing, USD/JPY trades ~120 pips above pre-data levels, but has faded off the high of 145.23.

- While EUR/USD initially fell to a weekly low at 1.1718, the losses are being pared swiftly, rallying ~40 pips off lows - likely as markets assess the continued decline in the size of the labor force and participation suggesting diminishing labor supply (more on that above).

- For the USD Index, this has put price back above the well-trodden downtrendline support drawn off the March 2024 low and - theoretically - back inside the falling wedge pattern that's dictated the USD's decline this year.

- We wrote earlier this week that the oversold position does raise the possibility that either; a correction unfolds soon, or that the pace of the trend slows down, resulting in more volatile price action going forward.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/07/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/07/2025 | 0645/0845 | * | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Unemployment | |

| 04/07/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/07/2025 | 0800/1000 | * | Retail Sales | |

| 04/07/2025 | 0800/1000 | ECB Elderson Speech At IMF OEDNE/World Bank Meeting | ||

| 04/07/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/07/2025 | 0900/1100 | ** | PPI | |

| 04/07/2025 | 1500/1600 | BOE Taylor Speech On Natural Interest Rate |