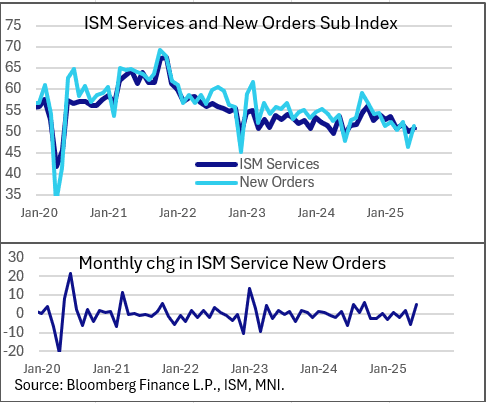

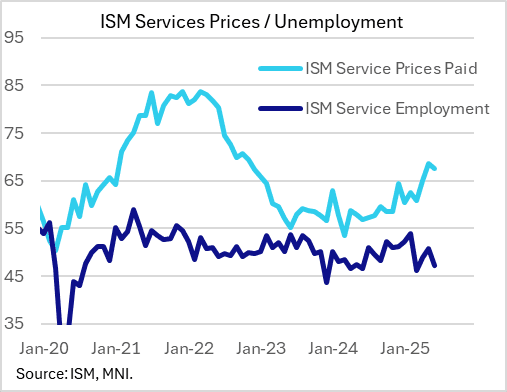

US DATA: Stabilization In ISM Services, But Tariff Impact Still Looms Large

June's ISM Services report was mixed, with prices, activity and new orders stabilizing after a worrying May, but employment and order backlogs notably soft as inventories continued to grow. Tariffs continued to cast a shadow over the survey, with anecdotes appearing more wary of the demand outlook than suggested by the improvement in the major aggregates.

- The headline index rose 0.9 points to 50.8 (consensus 50.6), ending a brief 1-month period in sub-50 territory for the 11th month in 12 at 50-plus. The main standouts on the positive side were in new orders, jumping 4.9 points to 51.3 (consensus 48.2) and reversing most of May's surprising weakness, and in new export orders, rising 2.6 points to 51.1 for the first 50+ reading since February as tariff concerns began to ramp up.

- Indeed there was some semblance of trade normalization after tariffs impacted activity heavily in previous months: aside from export orders, imports rose for the first time in the last 3 months, up 3.5 points to to 51.7.

- There was some respite in inflation, with prices paid unexpectedly pulling back 1.2 points to 67.5 (consensus was for a 0.2 point rise), though at these levels, price pressures remain elevated.

- The biggest point of weakness was in employment: the index fell 3.5 points to 47.2, more than the expected 1.2 point deterioration and the 3rd month in 4 in contractionary territory.

- Elsewhere, inventories continued to rise (up 3 points to 52.7), with supplier deliveries falling 2.2 points to 50.3 and backlogs falling 1 point to 42.4 for the weakest since Aug 2023 and the 10th fall in 11 months. For inventories, some respondents noted buying extra inventory "in case the talks with China don't go well" with "a need to increase stock purchases" due to longer lead times and anticipated further price increases.

- Per the report, "slow growth and economic uncertainty were frequently referenced by respondents...Price increases impacting costs of operations were mentioned more frequently this month. Middle East tensions were a new subject of comments in June, but there was no indication of related supply chain disruptions. The most common topic among survey panelists continued to be concerns about impacts related to tariffs.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Jul'25 10Y Vol Sales

- -4,000 TYN5 110.5/110.75 strangle w/ 110.25/111 strangle, 1.63 net 110-19.5

- 3,000 TYN5 110.5 straddles, 115

US DATA: April JOLTS Report More Of The Same Rather Than Sharper Deterioration

The JOLTS report for April was on balance one of relative stability in another look at early reaction to Trump administration policies. Job openings surprisingly increased whilst the hire rate pushed to its highest since September although the quits rate pushed back lower again after what to us was a surprising uptick back in March. Of course, this is only for April in a fast-moving environment.

- Job openings: 7391k (sa, cons 7100k) in April after a marginal upward revised 7200k (initial 7192k) in March.

- The ratio of vacancies to unemployed inched up from 1.02 to 1.03. The 1.02 was technically the lowest since Apr 2021. For context it has been in a relatively narrow range of 1.02-1.13 with an average 1.07 since Jun 2024) and averaged 1.2 in 2019 and 1.0 in 2017-18.

- The quits rate meanwhile dropped to 2.00% after what to us was a surprise increase back in March to 2.10%, for its lowest since Dec 2024.

- This rate is still above the 1.91 in November but remains significantly below the 2.3% in 2019 and 2.2% in 2017-18 in a sign of a cooling labor market.

- There’s a similar trend specifically for the private sector, at 2.22% after 2.33%, whilst government quit rates remain historically low at 0.8% overall and 0.5% specifically for federal employees.

- Hire rates showed some more encouraging signs, rising to 3.49% from 3.39% for their highest since Sep 2024, as it picks up from some low levels. It averaged 3.8% in 2017-18 and 3.9% in 2019.

- There’s a roughly similar story in private hire rates as well whilst the federal government hire rate held around 1% again, low by historical levels but continuing to stabilize rather than pushing lower.

- Layoffs meanwhile bounced to 1786k in April after the 1590k in March had been the lowest since Jun 2024. As is usually the case, gyrations are driven by the private sector. Government layoffs meanwhile fell back to 76k in April after two months at 100k, below the 83k averaged in 2024 for instance. The federal government only accounted for 3k of this. (Putting these gross layoffs into perspective, outright hire levels were 358k for the government and 31k for federal in April).

- Note that whilst Bloomberg now shows consensus expectations for quits and layoffs, the response sizes are much smaller than for openings, at 5 and 4 vs 32 respectively.

EQUITIES: Estoxx Rolling Put

SX5E (19th Sep vs 19th Dec) 5100p, sold the Dec at 60 in 5k.