US TSYS: Yields Rebound on Strong June Jobs Gain, Dip in Unemployment

Jul-03 2025 18:18

- Treasuries are broadly weaker into the early pre-holiday close, off this morning's post employment data lows - rates hold a rather narrow range after the initial knee-jerk sell-off.

- Brief two-way after the final data for the session, ISM Services Prices Paid & Employment slightly lower, New Orders higher while Factory/Durables Orders are in-line. slightly lower than expected S&P Global Services PMI, Composite near in-line.

- Currently, Sep'25 10Y trades -13 at 111-07 (110-31L / 111-28H). Through first key support at 111.08.5 (the 20-day EMA), next 110-30+ 50-day EMA, followed by 110-16 (Low Jun 20). Curves bear flatten: 2s10s -3.682 at 45.321; 5s30s -4.441 at 89.048. 10Y yield tapped 4.3576% high finished at 4.3457%.

- A 46k beat for NFPs in June (147k vs cons 106k) vs a 26k miss for private payrolls (74k vs cons 100k). The difference being government payrolls surging by 73k for the largest increase since Mar 2024. It comprised of -7k for federal (still weak after DOGE cuts earlier this year) but state +47k and local +33k.

- The major downside surprise in the unemployment rate (4.117% unrounded is the lowest since January, down from 4.244% prior and well below the rounded 4.3% consensus) came with a drop of 222k in the number of unemployed (the largest drop of the year) after 4 consecutive rises.

- Projected rate cut pricing significantly cooler vs. this morning's pre-data (*) levels: Jul'25 at -1.2bp (-6.3bp), Sep'25 at -19.1bp (-30.1bp), Oct'25 at -34.2bp (-47.3bp), Dec'25 at -51.8bp (-67bp).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: $16.2B Debt Issued Tuesday

Jun-03 2025 18:17

- Date $MM Issuer (Priced *, Launch #)

- 06/03 $3B *AfDB: $2B WNG 3Y SOFR+33, $1B WNG 10Y SOFR+64

- 06/03 $2.25B #NAB $750M 3Y +40, $750M 3Y SOFR+65, $750M 5Y +52

- 06/03 $2B #Bank of NY Mellon $750N 3NC2 +48, $500M 3NC2 SOFR+68, $750M 11NC10 +85

- 06/03 $2B *Prov. of Ontario: 10Y SOFR+95

- 06/03 $1.5B *CPPIB 5Y SOFR+54

- 06/03 $1.5B #GE Healthcare $650M +5Y +78, $850M 10Y +103

- 06/03 $1.25B *Kommuninvest +3Y SOFR+39

- 06/03 $1B *Hong Kong 5Y Green +50

- 06/03 $700M #Corebridge Global 5Y +85

- 06/03 $500M IADB 2030 tap SOFR+40

- 06/03 $500M *Autodesk WNG 10Y +87

FED: Gov Cook: Have To Be Open To "All Possibilities" For Rates...Even Hikes

Jun-03 2025 18:11

Fed Gov Cook (permanent FOMC voter, leans dovish) said Tuesday in a speech (link) hewed very close to the FOMC majority's view on monetary policy without giving much away on her personal views on future rates, saying that she believed:

- "The current stance of monetary policy is well positioned to respond to a range of potential developments. Trade policy changes and the response of financial markets, firms, and consumers suggest risks to both sides of our dual mandate. As I consider the appropriate path of monetary policy, I will carefully consider how to balance our dual mandate, and I will take into account the fact that price stability is essential for achieving long periods of strong labor market conditions."

- However in Q&A she intriguingly noted that “we have to be open to all possibilities. We don’t know how tariffs are going to play out. One could imagine those scenarios – cutting, staying or hiking, happening."

- It's not often these days we hear Fed governors even mention the possibility of hikes, even if of course that's part of keeping every possibility "open".

- Re the risks to the dual mandate, Cook elaborated in her speech that the "Administration's policies...appear to be increasing the likelihood of both higher inflation and labor-market cooling... In this environment, monetary policy will need to carefully balance our dual-mandate goals of price stability and maximum employment." The labor market "has remained resilient" and though inflation "remains somewhat above target", "most measures of longer-term inflation expectations have moved less significantly" than one-year expectations.

- On that latter note, here speech also emphasized price stability as essential: "As I consider the appropriate path of monetary policy, I will carefully consider how to balance our dual mandate, and I will take into account the fact that price stability is essential for achieving long periods of strong labor market conditions."

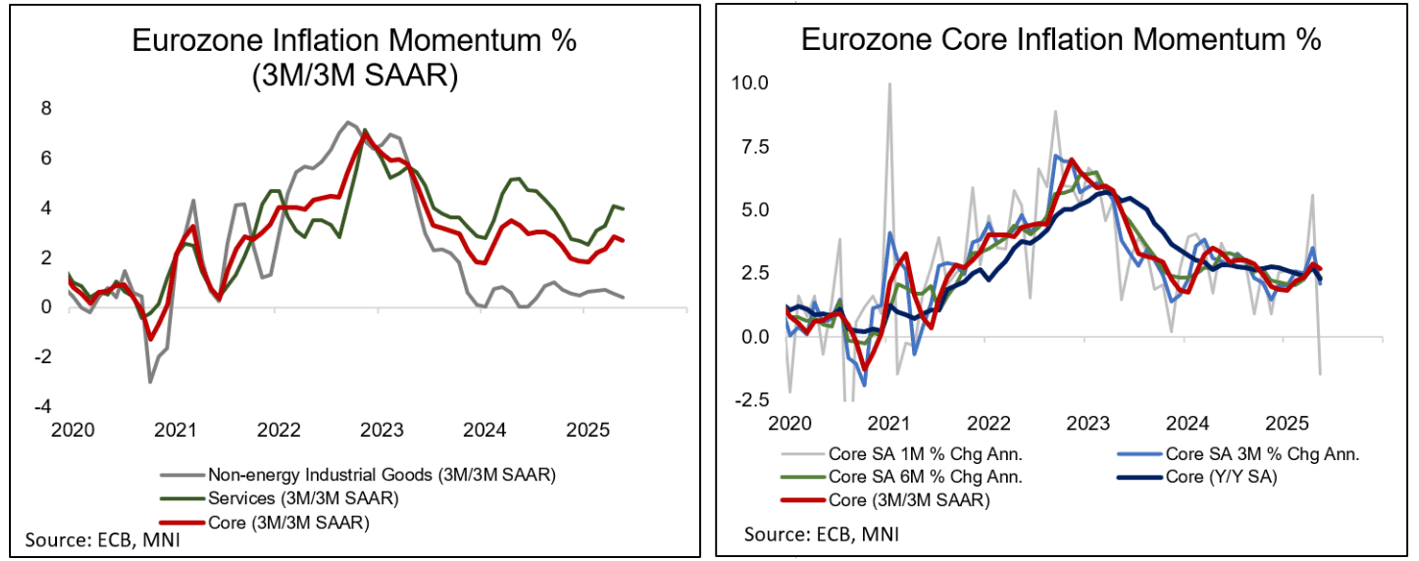

EUROPEAN INFLATION: MNI Eurozone Inflation Insight – May 2025

Jun-03 2025 18:06

We've just published our review of the May Eurozone flash inflation round - DOWNLOAD FULL REPORT HERE

Services Y/Y Falls To 3-Year Low

- Eurozone May flash HICP headline and core both printed 0.1pp below consensus expectations, at 1.9% and 2.3%, respectively. Services inflation saw a more meaningful 0.2pp ‘miss’ at 3.2% Y/Y, materially below April’s 4.0% for the lowest reading since March 2022.

- The deceleration seems to have been underpinned by an “Easter Effect” unwind but a medium-term view on the ECB’s seasonally adjusted data suggests that some underlying softening was also likely at play.

- Across the main countries, lower-than-expected readings were observed in France (0.6% Y/Y vs 0.9% cons), Spain (1.9% vs 2.0% cons), and notably the Netherlands (3.0% vs 3.8% cons), while Italy printed inline (1.9% vs 1.9% cons) and Germany was slightly firmer than expected (2.1% vs 2.0% cons). The drag on euro area inflation from the Netherlands was of particular note, as it looks to have contributed significantly to the below-expected EZ reading.

- The inflation data kept market expectations firmly for a 25bp cut at the upcoming June ECB meeting – see our full preview of the decision here.

- MNI published a sources story on May 30 highlighting that the upcoming ECB June meeting is set to see a lower inflation forecast for 2026, from 1.9% in March’s projections to 1.7% or 1.8% in the updated round. “Despite this downward revision, this deviation below 2% will not be considered strong enough to automatically trigger an additional rate cut beyond the June meeting, as some of the drivers of this inflation revision could reverse course given uncertainty over international trade”, the sources piece read (link).