US DATA: Jobless Claims Data Don’t Rock The Boat

Jul-03 2025 16:05

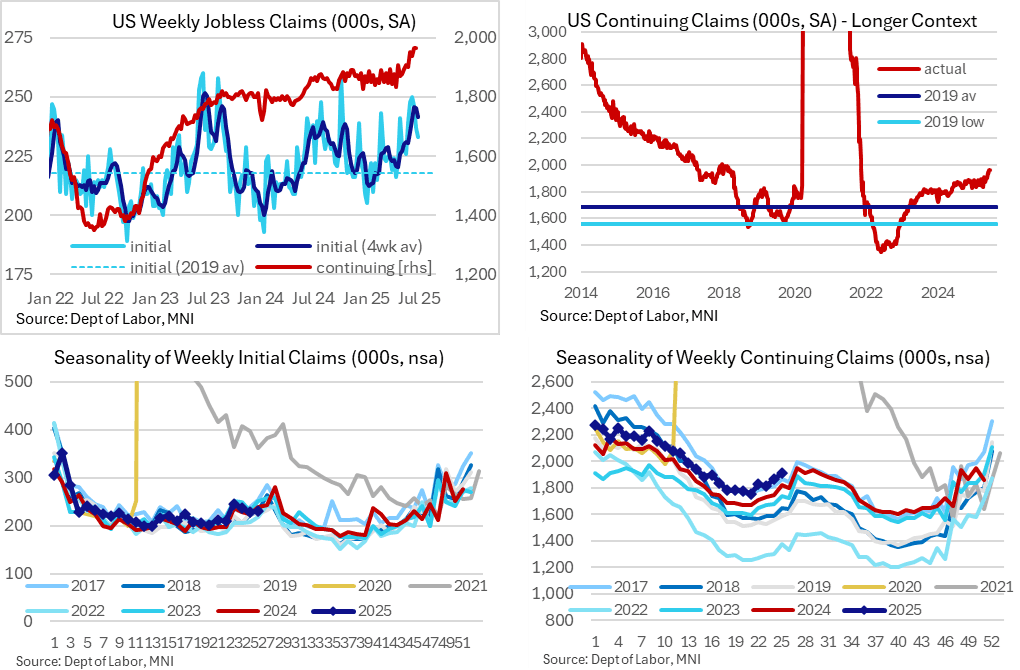

The latest weekly jobless claims data point to another small dip in initial claims even if the four-week average remains elevated whilst continuing claims unsurprisingly held at highs since late 2021. It continues to broadly point to a ‘low firing, low hiring’ labor market with the pace of deterioration slowing a touch compared to recent weeks.

- Initial jobless claims were lower than expected at 233k (sa, cons 241k) in the week to Jun 28 after a marginally upward revised 237k, marking a third consecutive decline.

- The four-week average eased lower to 242k, a second weekly decline having recently peaked at 246k at what had been the highest since Aug 2023, although it’s still elevated by recent standards.

- Continuing claims meanwhile were as expected at 1964k (sa, cons 1962k) in the week to Jun 21 after a slightly downward revised 1964k (initial 1974k).

- In non-seasonally adjusted terms, initial claims remain within typical ranges for the time of year whilst continuing claims are right at the top end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY TO SELL $55.000 BLN 8W BILL JUN 05, SETTLE JUN 10

Jun-03 2025 16:05

- US TSY TO SELL $55.000 BLN 8W BILL JUN 05, SETTLE JUN 10

US TSYS: Midday Update: Treasury Yields Rising With US Stocks

Jun-03 2025 15:57

- Treasury futures are trading mixed ahead midday, continuing to pare gains after this morning's higher than expected JOLTS job gains. Latest headlines/social media posting re: potential talk between Pres Trump and China's Xi notwithstanding.

- Tsy Sep'25 10Y futures currently trades -2.5 to session low of 110-12.5, 10Y yield +.0238 at 4.4636%. Technical support well below at 109-12.5, May 22 low. Curves flatter/off lows: 2s10s -0.925 at 49.195, 5s30s -1.204 at 94.656.

- Cross asset: Stocks gaining, top of range (SPX eminis +27.25 at 5974.5), Gold lower/off lows at 3349.56, Bbg US$ index remains firm at 1213.95 (+5.19).

OPTIONS: Larger FX Option Pipeline

Jun-03 2025 15:45

- EUR/USD: Jun05 $1.1050(E5.9bln), $1.1300(E2.3bln), $1.1375-85(E1.6bln), $1.1400(E2.2bln), $1.1415-25(E1.6bln), $1.1500(E1.5bln); Jun06 $1.1500(E1.0bln); Jun09 $1.1425(E1.7bln)

- USD/JPY: Jun05 Y142.00($1.2bln), Y143.00-05($1.1bln), Y145.00-20($1.6bln)

- AUD/USD: Jun06 $0.6300(A$1.5bln)