US DATA: Question Marks Of Strength Of Government Payrolls In June

Jul-03 2025 14:41

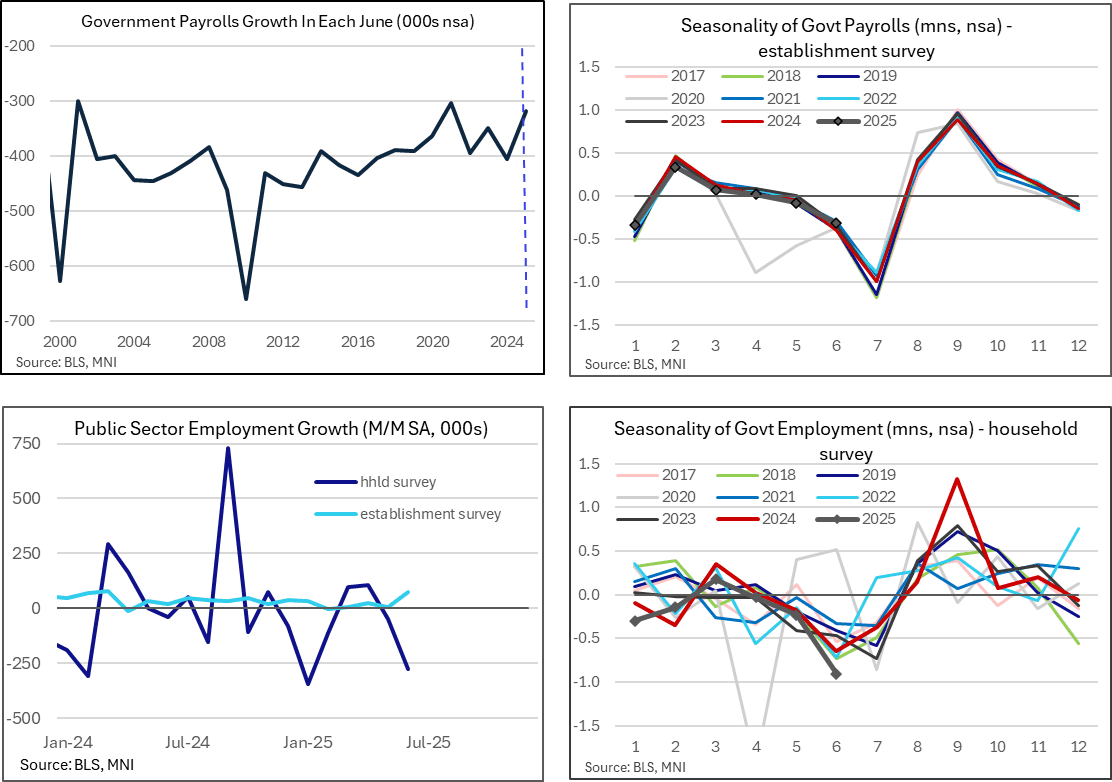

- As noted at the time, government payrolls growth was surprisingly strong in June at a seasonally adjusted 73k for the largest increase since Mar 2024. It follows an average of just 8k in Feb-May early on in DOGE efforts to reduce federal headcount.

- It comprised of -7k for federal (still weak after an average -16k in the four months prior) but state in particular jumped 47k (strongest since Jan 2023) whilst local also increased 33k (strongest since Mar 2024). Education played a big role, worth +40k for state and +23k for local.

- Some potential factors at play:

- i) It’s possible that those either directly affected by federal cuts (federal govt payrolls have dropped a cumulative 69k over the five months through Feb-Jun) or discouraged by federal cuts more broadly have looked to positions in state and local government roles (yesterday’s JOLTS report for back in May showed a 0.2pp rise in the federal quit rate to 0.7% for its highest since early 2023). That could however be a risky strategy if broader government roles come under pressure, and we also expect there to only be limited crossover from federal to education positions.

- ii) A likely better explanation is the role seasonality plays against this backdrop of cutbacks, although this too has pitfalls. June tends to see sizeable outright declines in non-seasonally adjusted terms, albeit not to the same extent as in July. Having averaged -383k in the previous three Junes, this month saw a smaller -318k which could be reluctance of government departments to cut positions if considering the possibility of hiring freezes or cuts ahead. That said, education seasonality plays a major role here, with June typically being the start of the summer holidays, and this argument of holding onto government employees is less compelling here. An alternative case is simply that school holidays started a little later this year although it’s hard to confirm.

- As such, a quirk of the seasonal adjustment process looks likely to be at play even if it’s hard to pin it down on anything more concrete. Further complicating matters, whilst highly volatile, those identified as employed by the government in the household survey fell by a heavy -275k (sa) on the back of an unusually heavy non-seasonally adjusted decline.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Call Condor Close Out

Jun-03 2025 14:40

ERM5 97.875/98.00/98.125/98.25 call condor, sold out at 11 in 10k.

STIR: Back To 50bp Of Fed Cuts For 2025 On Solid JOLTS Report

Jun-03 2025 14:39

- Stronger than expected job openings have seen Fed Funds implied rates rise 1bp for Sep/Oct meetings and 2bp for the Dec 2025.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 21.5bp Sep, 35.5bp Oct and 50.5bp Dec.

- It helps some continued paring of last week’s second half decline in implied rates although the Dec’25 is still 6bp lower than levels shortly before Thursday’s dovish jobless claims and GDP revisions.

- The SOFR terminal implied yield of 3.295% (SFRZ6) is 3.5bp higher post-data for 1bp higher on the day.

BOC: Instant Answers For BOC Rate Decision Expected Wed

Jun-03 2025 14:38

Following are the expected Instant Answers for the Bank of Canada interest-rate decision Wed at 945am EST:

- Overnight Rate Target

- Does the Bank signal it is prepared to LOWER rates in the future?

- Does the Bank signal it is prepared to RAISE rates in the future?

- Does the Bank signal it intends to leave rates on hold?

- Does the Bank mention core inflation has been elevated or above the 2% target for headline CPI?

- Does the Bank say the trade war is boosting inflation or inflation expectations?

- Does the Bank say the risks to growth from the trade war appear to have eased?