MNI ASIA OPEN: Solid Weekly Claims Improvement

EXECUTIVE SUMMARY

- MNI FED: Dallas's Logan: Time To Move From Fed Funds Policy Rate To Tri-Party Repo

- MNI FED: KC Fed's Schmid: Slightly Restrictive Policy The "Right Place To Be"

- MNI FED: Chicago's Goolsbee: Uneasy With Too Much Cut Frontloading

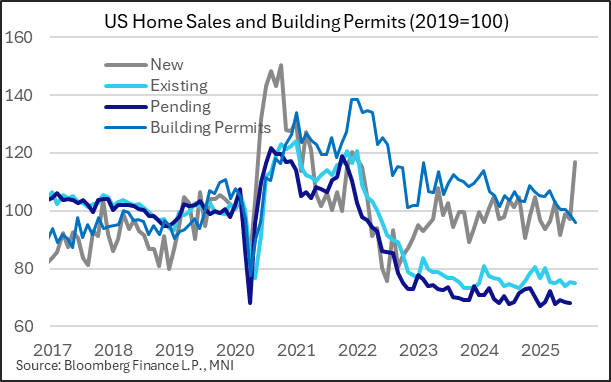

- MNI US DATA: Existing Home Sales Market Tightening Very Slightly, But Still Loose

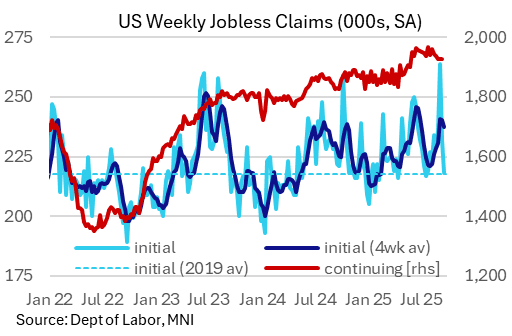

- MNI US DATA: Solid Improvement Across Initial And Continuing Jobless Claims

US

MNI FED: KC Fed's Schmid: Slightly Restrictive Policy The "Right Place To Be"

KC Fed President Schmid, who is a 2025 FOMC voter and among the most hawkish members of the Committee, continues to sound concerned over the inflation outlook in a speech Thursday, while acknowledging that some risks to the labor market are emerging. He's probably one of the 6 members who penciled in no further rate cuts this year in his 2025 Dot Plot. "I viewed the 25-basis point cut in the policy rate last week as a reasonable risk-management strategy as the Fed balances its inflation objective with some heightened concern over the health of the labor market."

MNI FED: Dallas's Logan: Time To Move From Fed Funds Policy Rate To Tri-Party Repo

Dallas Fed President Logan called for the FOMC to switch its policy target from the Federal funds rate to the tri-party general collateral rate (TGCR) in a speech Thursday. It's about as un-technical as you can get given the subject matter, but to sum up, Logan goes through several known critiques of using the Fed funds rate as the FOMC's key policy rate, and suggests alternatives, ultimately settling on the tri-party general collateral rate.

MNI FED: Chicago's Goolsbee: Uneasy With Too Much Cut Frontloading

Chicago Fed President Goolsbee (2025 FOMC voter) told reporters (including MNI) Thursday that he was "uneasy" with frontloading rate cuts: "The reason why I'm uneasy with too much frontloading of cuts is because we still need to get the information and have confidence that the rise of the inflation rate, after four and a half years of being above the target, we have to be convinced that that's transitory."

NEWS

MNI US: Trump Says He Could Lift Sanctions On Turkey "Almost Immediately"

US President Donald Trump told reporters that he wants Turkey to “stop buying Russian oil”. Speaking alongside Turkish President Recep Tayyip Erdogan in the Oval Office, Trump said, “We’ve had tremendous relationships, both having to do with war and with trade. I guess today we’re talking about both. I’d like to have him stop buying any oil from Russia while Russia continues its rampage against Ukraine…”

MNI SECURITY: Iran Vows To Continue Nuclear Program, Snapback Appear Unavoidable

Iranian Vice President and head of the Atomic Energy Organisation of Iran, Mohammad Eslami, told reporters in Moscow Iran “will continue with its nuclear program,” ahead of the Sept. 27 deadline for the reimposition of UN sanctions via the snapback mechanism triggered by the UK, Germany, and France on Aug. 28.

MNI US: MNI POLITICAL RISK - OMB Threatens Mass Layoffs As Shutdown Looms

The Trump administration raised the stakes of its shutdown standoff with Democrats ahead of the September 30 deadline for funding the government. Office of Management and Budget director Russell Vought issued a memo threatening mass firings of federal workers if the government shuts down on October 1.

US TSYS

MNI US TSYS: Hawkish Reaction to Flood of Economic Data

- Treasuries reacted hawkishly to a flood of data

- Initial jobless claims surprised to the downside in the week of Sep 20, at 218k (233k consensus, 232k prior rev up by 1k), continuing claims sustained their recent retracement lower, to 1,926k (1,932k consensus, 1,928k prior albeit rev up by 8k).

- Existing home sales totaled 4.00M in August on a seasonally-adjusted, annualized basis, per the National Association of Realtors. This was a little above the expected 3.95M, though a small decline from July's 4.01M.

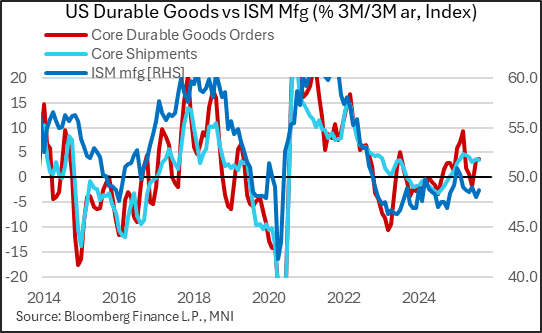

- Durable and capital goods orders exceeded expectations in August. Headline orders came in at 2.9% M/M, besting the expected 0.3% contraction and reversing August's 2.7% fall (rev from a 2.8% drop).

- Currently, the Dec'25 10Y trades -8.5 at 112-12 (yld 4.1678% +.0213) vs. 112-06 low - technical support below at 112-01 (50.0% retracement of the Jul 15 - Sep 11 bull phase). Curves flatter: 2s10s -3.399 at 50.642, 5s30s -4.530 at 98.639.

- Projected rate cut pricing receded vs. early morning levels (*): Oct'25 at -21.5bp (-22.7bp), Dec'25 at -39.0bp (-42.7bp), Jan'26 at -47.7bp (-53.2bp), Mar'26 at -57.5bp (-64.8bp).

- Firmer-than-expected US GDP data on Thursday, alongside lower-than-expected weekly jobless claims has kept the greenback trading with a very supportive tone throughout the US session. The dollar index (+0.68%) has been steadily grinding higher, extending to a high of 98.61 as we approach the APAC crossover, now ~2.4% above the post-Fed cycle lows.

- KC Fed President Schmid, a 2025 FOMC voter and among the most hawkish members of the Committee, continues to sound concerned over the inflation outlook in a speech Thursday, while acknowledging that some risks to the labor market are emerging.

- Looking ahead to Friday's schedule: Personal Income/Spending, PCE Price Index (0830ET), U. of Mich. Sentiment & inflation outlook (1000ET). Fed Speak: Richmond Fed Barkin outlook, moderated discussion (0900ET), Fed VC Bowman moderated Q&A on policy (1300ET).

OVERNIGHT DATA

MNI US DATA: Solid Improvement Across Initial And Continuing Jobless Claims

Initial jobless claims surprised to the downside in the week of Sep 20, at 218k (233k consensus, 232k prior rev up by 1k). This was the lowest number of initial claims in 9 weeks, and brought the 4-week average down to a 3-week low 238k. Meanwhile continuing claims sustained their recent retracement lower, to 1,926k (1,932k consensus, 1,928k prior albeit rev up by 8k). This marked the lowest in 16 weeks.

MNI US DATA: Existing Home Sales Market Tightening Very Slightly, But Still Loose

Existing home sales totaled 4.00M in August on a seasonally-adjusted, annualized basis, per the National Association of Realtors. This was a little above the expected 3.95M, though a small decline from July's 4.01M. The 6-month average for sales is exactly 4.00M, so this report merely confirms the recent trend (or lack thereof) in sales activity, which remains about 25% below 2019 (pre-Covid) levels.

MNI US DATA: Core Durable Goods Solidifying After Volatile Period

Durable and capital goods orders exceeded expectations in August. Headline orders came in at 2.9% M/M, besting the expected 0.3% contraction and reversing August's 2.7% fall (rev from a 2.8% drop). As is more often the case than not, aircraft orders volatility played a key role here, though it wasn't just the usual nondefense aircraft & parts (i.e. Boeing)

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 194.99 points (-0.42%) at 45929.8

S&P E-Mini Future down 37.75 points (-0.56%) at 6655

Nasdaq down 133.7 points (-0.6%) at 22365.49

US 10-Yr yield is up 2.1 bps at 4.1678%

US Dec 10-Yr futures are down 9.5/32 at 112-11

EURUSD down 0.008 (-0.68%) at 1.1658

USDJPY up 0.9 (0.6%) at 149.8

Gold is up $14.35 (0.38%) at $3750.49

European bourses closing levels:

EuroStoxx 50 down 19.67 points (-0.36%) at 5444.89

FTSE 100 down 36.45 points (-0.39%) at 9213.98

German DAX down 131.98 points (-0.56%) at 23534.83

French CAC 40 down 32.03 points (-0.41%) at 7795.42

US TREASURY FUTURES CLOSE

3M10Y +0.035, 18.4 (L: 14.985 / H: 21.439)

2Y10Y -3.205, 50.836 (L: 50.427 / H: 54.768)

2Y30Y -5.525, 108.925 (L: 108.327 / H: 115.104)

5Y30Y -4.431, 98.738 (L: 97.945 / H: 103.46)

Current futures levels:

Dec 2-Yr futures down 4/32 at 104-3 (L: 104-02.375 / H: 104-07)

Dec 5-Yr futures down 8/32 at 109-2 (L: 108-31 / H: 109-10.25)

Dec 10-Yr futures down 9.5/32 at 112-11 (L: 112-06 / H: 112-22)

Dec 30-Yr futures down 3/32 at 116-7 (L: 115-24 / H: 116-17)

Dec Ultra futures up 2/32 at 119-22 (L: 119-00 / H: 120-02)

MNI US 10YR FUTURE TECHS: (Z5) Corrective Pullback Extends

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 113-00 High Sep 24

- PRICE: 112-10 @ 1402 ET Sep 25

- SUP 1: 112-01 50.0% retracement of the Jul 15 - Sep 11 bull phase

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Treasury futures have continued to weaken and remain in retracement mode. Today’s sell-off has resulted in a print below the 50-day EMA, at 112-10. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13, the Aug 18 low and the next key support. Initial resistance to watch is 113-00, the Sep 24 high.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 -0.050 at 96.265

Mar 26 -0.080 at 96.435

Jun 26 -0.090 at 96.645

Sep 26 -0.080 at 96.795

Red Pack (Dec 26-Sep 27) -0.085 to -0.075

Green Pack (Dec 27-Sep 28) -0.065 to -0.06

Blue Pack (Dec 28-Sep 29) -0.05 to -0.04

Gold Pack (Dec 29-Sep 30) -0.035 to -0.02

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.13% (+0.01), volume: $2.852T

- Broad General Collateral Rate (BGCR): 4.12% (+0.03), volume: $1.155T

- Tri-Party General Collateral Rate (TCR): 4.12% (+0.03), volume: $1.114T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $176B

FED Reverse Repo Operation

RRP usage slips to $25.369B with 21 counterparties this afternoon from $29.172B Wednesday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $7.28B to Price Thursday, $73.53B/wk

- Date $MM Issuer (Priced *, Launch #)

- 09/25 $3B #Emirate of Abu Dhabi $1B 3Y +10, $2B 10Y +18

- 09/25 $1.58B #Olympus Water US 7.5NC3 7.25%, not including E830M 7.5NC3

- 09/25 $1.4B #Windstream Services 8NC3 7.5%

- 09/25 $800M #Realty Income $400M +3Y +48, $400M +7Y +73

- 09/25 $500M #CNH Industrial Capital 5Y +78

MNI BONDS: EGBs-GILTS CASH CLOSE: 10Y Yields See Highest Close In Weeks

European yields rose Thursday, with Gilts underperforming peers and periphery spreads widening to Bunds.

- Early trade was constructive, with some bull flattening in the curve attributed partly to a solid Japanese long-end auction overnight.

- But yields started to rise in late London morning trade, with large selling orders in Bund observed alongside equities extending losses, albeit no apparent headline trigger to the move.

- They would spike again on stronger than expected US economic data in the early European afternoon - including GDP and jobless claims.

- Yields closed near their highs, with 10Y Gilt and Bund each seeing their highest close since Sept 2. The German curve bear flattened on the day, with underperformance in the belly, while the UK's bear steepened.

- Periphery/semi-core EGB spreads closed wider alongside a retracement in equities, with BTPs faring worst.

- Elsewhere, the SNB held rates as expected; German GfK consumer climate more than expected.

- Friday's agenda includes Spanish final GDP, Italian confidence / sentiment indicators, and ECB Wave inflation expectations, along with appearances by ECB's Cipollone and Escriva.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.7bps at 2.039%, 5-Yr is up 3.3bps at 2.36%, 10-Yr is up 2.5bps at 2.773%, and 30-Yr is up 0.4bps at 3.342%.

- UK: The 2-Yr yield is up 6.6bps at 4.019%, 5-Yr is up 7.9bps at 4.177%, 10-Yr is up 8.8bps at 4.757%, and 30-Yr is up 7.9bps at 5.566%.

- Italian BTP spread up 1.7bps at 83.4bps / Spanish up 1.1bps at 56.4bps

MNI FOREX: USD Strength Extends, NZD and GBP Technical Breaks Exacerbate Momentum

- Firmer-than-expected US GDP data on Thursday, alongside lower-than-expected weekly jobless claims has kept the greenback trading with a very supportive tone throughout the US session. The dollar index (+0.68%) has been steadily grinding higher, extending to a high of 98.61 as we approach the APAC crossover, now ~2.4% above the post-Fed cycle lows. The DXY appears to have solidly broken above the 50-day EMA, a bullish development.

- While associated declines across the G10 have been broad based, with the likes of EUR and JPY falling around 0.65%, both GBP and NZD are the clear underperformers, with significant technical breaks exacerbating downside momentum.

- For GBPUSD (-0.83%) specifically, we highlighted the breach of two support trendlines, drawn from both the Aug 01 and the January lows. Spot has moved sharply lower, and has significantly bridged the gap to the first target of 1.3333, the Sep 3 low and a key support. Below here, a key medium-term level resides at 1.3140. Both fiscal uncertainty and political tensions are rising in the UK, potentially underpinning the fundamentals behind the latest GBP pessimism.

- For NZDUSD (-0.86%), today’s weakness has seen the pair dip through the noted pivot level of 0.5800. A daily close below this mark would be a further bearish development, targeting a Fibonacci retracement at 0.5728.

- US data will continue to set the tone for the dollar, with markets eagerly awaiting next week’s employment report. On Friday, the monthly Personal Income and Outlays report for August will provide greater clarity on recent momentum. Core PCE will also be watched with it widely expected to print softer than the 0.35% M/M seen for core CPI.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/09/2025 | 0700/0900 | *** | GDP (f) | |

| 26/09/2025 | 0715/0915 | ECB Cipollone At ECB-CEPR Conference | ||

| 26/09/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 26/09/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 26/09/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 26/09/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 26/09/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 26/09/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 26/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 26/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 26/09/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 26/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/09/2025 | 1700/1300 | Fed Vice Chair Michelle Bowman |