US 10YR FUTURE TECHS: (Z5) Corrective Pullback Extends

Sep-25 13:03

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-12/29 High Sep 18 / High Sep 11 and the bull trigger

- RES 1: 113-00 High Sep 24

- PRICE: 112-07+ @ 13:52 BST Sep 25

- SUP 1: 112-01 50.0% retracement of the Jul 15 - Sep 11 bull phase

- SUP 2: 111-26 Low Aug 26

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 111-01+ 76.4% retracement of the Jul 15 - Sep 11 bull phase

Treasury futures have continued to weaken and remain in retracement mode. Today’s sell-off has resulted in a print below the 50-day EMA, at 112-10. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13, the Aug 18 low and the next key support. Initial resistance to watch is 113-00, the Sep 24 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US Q2 FHFA HPI Q/Q SA -0.0% V +2.9% Q2 2024

Aug-26 13:00

- MNI: US Q2 FHFA HPI Q/Q SA -0.0% V +2.9% Q2 2024

MNI:US JUN FHFA HPI SA -0.2% V -0.1% MAY; +2.6% Y/Y

Aug-26 13:00

- MNI:US JUN FHFA HPI SA -0.2% V -0.1% MAY; +2.6% Y/Y

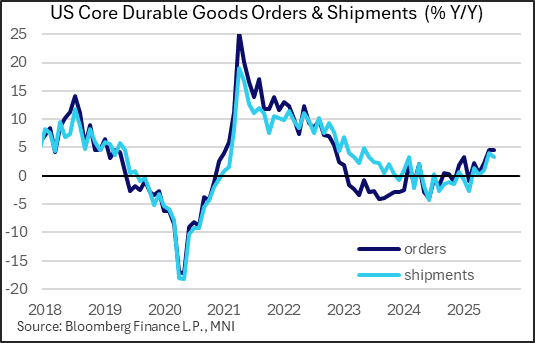

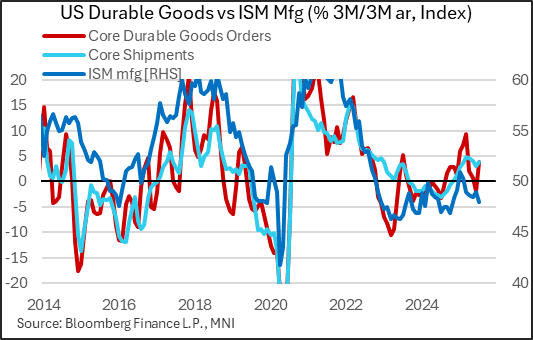

US DATA: Solid Start To Q3 For Durable Goods Activity

Aug-26 12:57

Durable goods orders showed a pickup in July, with better revisions casting a slightly better light on goods production and business equipment investment this summer.

- Headline durable goods orders bested expectations at -2.8% M/M (-3.8% expected, -9.4% prior), weighed down once again by the extremely volatile nondefense aircraft orders category (-33% M/M, after -53% prior).

- A better signal came from durable orders ex-transportation, which rose 1.1% (0.2% expected) after 0.3% prior. And the key core capital goods orders (nondefense, ex-aircraft) category also rose by 1.1% M/M (0.2% expected), more than reversing June's decline (-0.6%, upwardly revised from -0.8%).

- Meanwhile, core shipments continued to hum along, rising by a 27-month high 0.7% M/M (0.2% expected, 0.4% prior rev from 0.3%).

- Zooming out, core capital goods orders are nor rising at a 3.8% 3M/3M annualized pace, the strongest since March at which point activity was seen to be heavily influenced by tariff front-running.

- The Y/Y NSA figure may tell a clearer story, and it's a positive one: core orders have risen 4.4% Y/Y by that measure for two consecutive months, the best seen since Q4 2022.

- Category-wise, there was strength pretty much across the board, with metal products, machinery, computers/electronics, and electrical equipment/appliances/ components, and motor vehicles and parts all seeing a rise in new orders (we exclude volatile aircraft).

- One note of caution here is that the figures are in nominal dollar terms and thus may be reflecting a bottoming out of goods / components prices in addition to orders volumes. But momentum appears to be headed back in a positive direction, at least tentatively.