FED: Dallas's Logan: Time To Move From Fed Funds Policy Rate To Tri-Party Repo

Sep-25 17:58

Dallas Fed President Logan called for the FOMC to switch its policy target from the Federal funds rate to the tri-party general collateral rate (TGCR) in a speech Thursday.

- It's about as un-technical as you can get given the subject matter, but to sum up, Logan goes through several known critiques of using the Fed funds rate as the FOMC's key policy rate, and suggests alternatives, ultimately settling on the tri-party general collateral rate.

- To sum up:

- "Options fall in three broad categories. The first includes administered rates, such as interest on reserves or the rate on the Overnight Reverse Repurchase Agreement Facility or the Standing Repo Facility. The second category involves measures of the constellation of money market rates. And the third category entails switching to a different single market rate.

- "I’m not a fan of targeting an administered rate...Targeting the constellation of market rates is also unattractive..."

- "So which single rate is best? Overnight repo markets are the center of gravity. Within those markets, repos against Treasury collateral make the most appropriate target, because when risk-managed appropriately, they are essentially riskless."

- "Participants in dollar funding markets have widely adopted SOFR as a reference rate....But SOFR isn’t currently a clean gauge of funding costs...."

- "The tri-party general collateral rate (TGCR) is cleaner, and I think it would currently offer the best target."

- While she acknowledges that these are "only my views", she suggests that the FOMC could change its target rate "proactively" "when markets are functioning smoothly and market participants can have plenty of advance notice", though an intermediate option "would be to announce a contingency plan but not implement it for the time being.".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Interview With Fed Governor Nominee Stephen Miran

Aug-26 17:54

MNI interviews Fed governor nominee Stephen Miran on his economic outlook. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

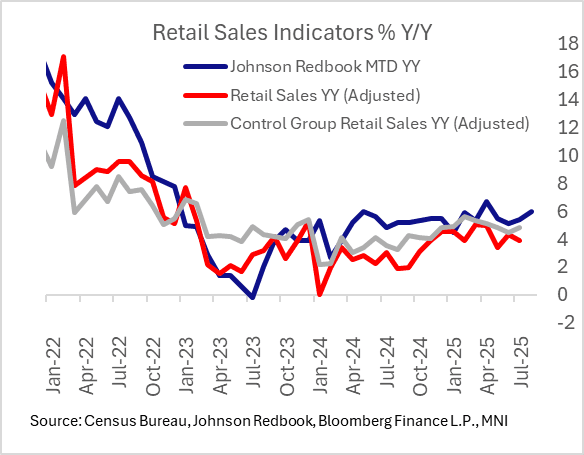

US DATA: Redbook Retail Sales Remain Solid Into Late August, Tariff Impacts Seen

Aug-26 17:47

Retail sales remained robust into late August, with the Johnson Redbook index up 6.5% in the week ending Aug 23, after 5.9% the prior week. That brings month-to-date sales growth to 6.0% Y/Y, getting closer to retailers' targeted 6.2%.

- Anecdotes from the report noted higher prices resulting from tariffs, which spurred traffic at discount stores: "Back-to-school sales were active last week as the start of the school year approaches. Apparel and accessories sales, particularly from private labels, performed well in the Southern and Midwestern regions, where the school year begins earlier. Shoppers are purchasing items closer to the time they need them. Most of the Trump administration's tariffs took effect at the beginning of August, leading to higher prices. As a result, shoppers—especially those with lower incomes—tend to seek bargains at large discount stores, which have significant supply chain advantages that allow them to maintain lower prices. Additionally, the positive effects of state tax holidays were evident in the sales results for Connecticut."

- Despite continued weakness in consumer sentiment, retail sales growth looks as though it is remaining steady in August.

- That's even if the Redbook (along with the "official" Census Bureau) data, which is in nominal terms, is somewhat exaggerated due to price differences, at 4-6% nominal growth, price-adjusted volumes are likely still firmly positive (total Census Bureau advance retail sales were up 3.9% Y/Y in July, with ex-autos/gas up 4.4% and control group 4.8%).

- We will get a little more insight on recent spending trends with Friday's PCE spending data for July.

BONDS: EGBs-GILTS CASH CLOSE: OAT/Bund Spread Continues To Widen On Politics

Aug-26 17:38

OATs remained under pressure Tuesday as political risk concerns remained prevalent.

- The OAT/Bund spread widening initiated Monday by PM Bayrou's call for a confidence on his own government (to be held Sep 8) continued, with speculation that President Macron could have to call another set of legislative elections.

- French yields actually closed lower on the day, but the 10Y yield touched its highest level (3.534%) since March before recovering. 10Y OAT/Bund closed at 77.3bp, the widest since April 11 and up over 7bp this week.

- Elsewhere, French consumer confidence came in on the weak side, while BOE's Mann in a speech appeared to rule out any further rate cuts in the short-term.

- The German curve bull steepened, with the UK's bear steepening (the underperformance in cash being due to a catch-up from bank holiday market closure). Periphery EGB spreads widened modestly.

- Wednesday's schedule is on the light side, with German GfK consumer confidence and UK CBI Sales data, with main focus remaining on flash August Eurozone inflation later in the week.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.7bps at 1.938%, 5-Yr is down 4.7bps at 2.268%, 10-Yr is down 3.4bps at 2.723%, and 30-Yr is down 1.2bps at 3.32%.

- UK: The 2-Yr yield is up 2.4bps at 3.968%, 5-Yr is up 3.8bps at 4.139%, 10-Yr is up 4.7bps at 4.74%, and 30-Yr is up 6bps at 5.608%.

- Italian BTP spread down 0.5bps at 83.3bps / French OAT up 5.1bps at 77.3bps