MNI ASIA OPEN: Pessimism Reigns Post-Liberation Day

EXECUTIVE SUMMARY

- MNI FED: Jefferson Sticks To ‘No Need To Hurry’ Guidance Post-Liberation Day

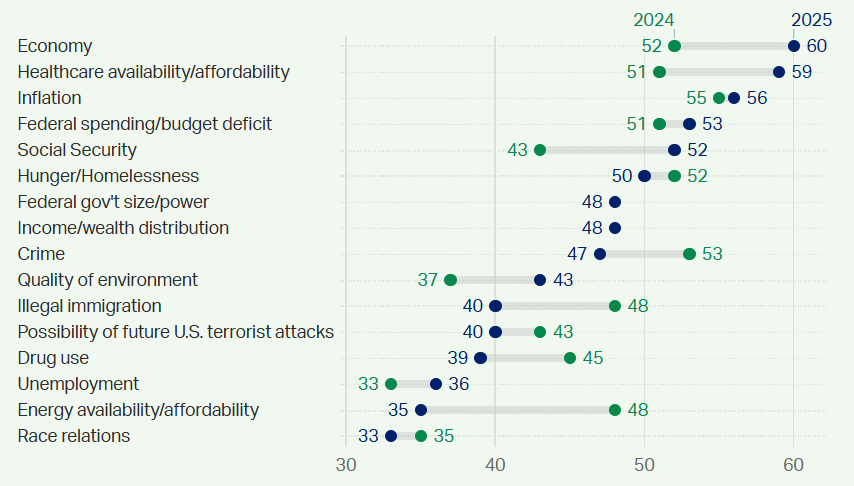

- MNI US: Concerns Over Economy And Inflation "Surge" - Gallup

- MNI US DATA: Challenger Job Cut Announcements Surge On DOGE Layoffs

- MNI US DATA: Claims Data Show Some Signs Of Rehiring Lethargy

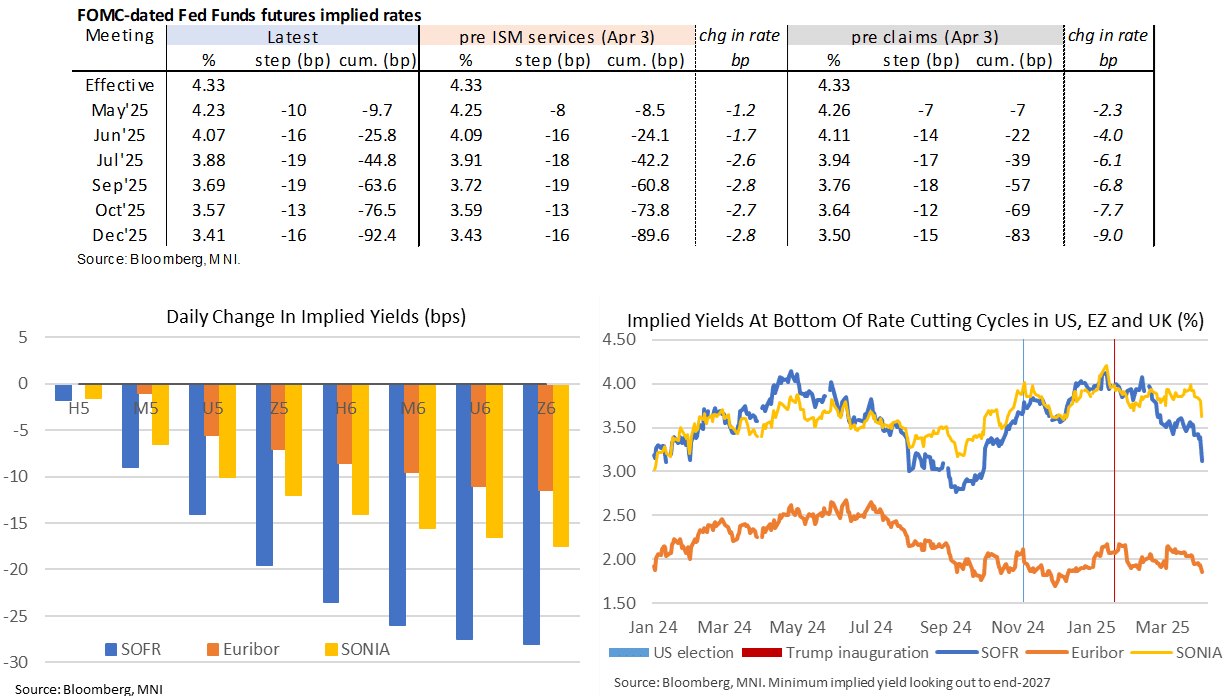

- MNI STIR: ISM Services Helps Push Over 120bp Of Fed Easing For The Cycle

- MNI US Payrolls Preview: A Pulse Check Amidst Tariff Pessimism

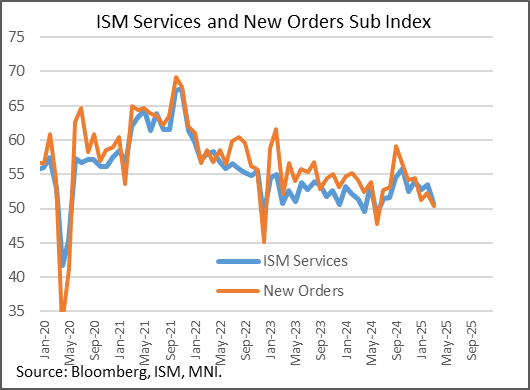

- MNI US DATA: ISM Services: Weak New Orders And Employment Send Cautious Econ Signal

US

MNI FED: Jefferson Sticks To ‘No Need To Hurry’ Guidance Post-Liberation Day

Fed Governor Jefferson (permanent voter) says there is no need to hurry to make rate adjustments, repeating a stance from Feb 19 when he last spoke on mon pol. He doesn’t go into detail on potential tariff implications after yesterday’s Liberation Day announcements besides saying there are multiple significant changes currently in progress. Jefferson, from the full speech: "In my view, there is no need to be in a hurry to make further policy rate adjustments. The current policy stance is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate."

MNI US: Concerns Over Economy And Inflation "Surge" - Gallup

A new survey from Gallup has found that US voters' worries about the US economy, healthcare, and social security have “surged” since 2024. Gallup notes: “Economic issues continue to dominate Americans’ national concerns, with majorities expressing “a great deal” of personal worry about the economy, healthcare availability and affordability, inflation and the federal budget deficit. Along with the economy and healthcare, public concern about Social Security and the environment is up significantly, with Social Security registering a 15-year high.”

Figure 1: Worries about key issues, % A great deal 2024-2025

Source: Gallup

NEWS

MNI US: Sens Grassley & Cantwell Introduce Bill To Reassert Influence Over Tariffs

Senators Chuck Grassley (R-IA) and Maria Cantwell (D-WA) have introduced legislation that would reassert some Congressional power over tariffs. The bill, modeled on the War Powers Resolution of 1973, would water down the emergency measures President Trump has used to impose tariffs unilaterally via executive authority. The legislation dictates that the President must notify Congress of new tariffs within 48 hours of imposition, explaining the reasoning behind the tariff and providing an assessment of the potential impact on US businesses and consumers. The bill states that Congress must then enact the tariff into law with a joint resolution within 60 days or the tariff will expire.

MNI UK: Trade Sec-Consultation w/Business On Retaliatory Tariffs Until 1 May

Secretary of State for Business and Trade Jonathan Reynolds speaking in the Commons on US tariffs. Says that he is launching a "request for input from British business on the implications of retaliatory action on tariffs". The minister sets a 1 May deadline for the consultation, adding that the action will be "paused" if an economic agreement is reached with the US in the meantime. Reynolds says that "a US deal is not just possible, but favourable to both."

MNI TARIFFS: Canada Will Respond With "Calibrated" And "Targeted" Measures - Carney

Canadian Prime Minister Mark Carney has delivered remarks stating that Canada will respond to US President Donald Trump’s tariffs with a “carefully calibrated” and “targeted” response. Carney reiterates that 80 years of US-Canada integration is “over,” and says, “we must respond with purpose and force.” He says Ottawa will match US auto tariffs by imposing a 25% tariff on all vehicles imported from the US that are not USMCA compliant. Carney notes that Canadian tariffs will not affect auto parts and will not affect vehicle content from Mexico, as Mexico complies with USMCA. He also confirms that previously announced retaliatory tariffs will remain in place.

MNI TARIFFS: Macron Asks European Businesses To Suspend Investments In US

French President Emmanuel Macron, speaking on US tariffs following a meeting with business leaders, calls for EU investments in the US to be suspended. Macron: "We are not naive, so we are going to protect ourselves. [It is] important that future investments, or those announced in recent weeks, be, for a time, suspended, until things have been clarified with the United States. What would be the message of having major European players start investing billions of euros in the American economy at a time when they are hitting us,"

MNI US TSYS: US Trade Policy Continues to Weigh Heavily on Sentiment

- Treasuries looked to finish broadly higher Thursday, little off midday highs as markets continue to react negatively to Pres Trump's reciprocal tariff announcement late Wednesday, SPX eminis index fell over 4.25%, the tech-heavy Nasdaq over 5.5%, the DJIA over 3.4%.

- Heavy risk-off support in rates saw June 10Y futures climb to 113-02 midmorning, shy of technical resistance of 113-05 (1.764 proj of the Jan 13 - Feb 7 - Feb 12 price swing), currently trade +1-06.5 at 112-22.5; 10Y yields fall below 4.0 briefly (3.9966% low), currently at 4.0455% after the bell.

- March's ISM Services report showed well below-expected activity measures, alongside a softer-than-expected reading on prices. This wasn't an outright negative report, with an expansionary overall reading and mixed comments about the impact of government policy shifts including tariffs, but it certainly casts a more cautious light on the services sector than February's solid ISM data.

- Despite a rise in projected rate cuts in 2025 rising to three 25bp moves by late October, Fed Governor Jefferson (permanent voter) says there is no need to hurry to make rate adjustments, repeating a stance from Feb 19 when he last spoke on mon pol. "The current policy stance is well positioned to deal with the risks and uncertainties that we face in pursuing both sides of our dual mandate."

- US pessimism reverberated into global currency markets, with dollar indices sharply lower on the session. The ICE dollar index is off its worst levels, but is broadly consolidating a 1.75% decline on Thursday, currently trading around the 102.00 mark.

OVERNIGHT DATA

MNI US Payrolls Preview: A Pulse Check Amidst Tariff Pessimism

- Nonfarm payrolls are seen increasing a seasonally adjusted 140k in March in the Bloomberg survey after 151k in February. Primary dealer analysts also see 140k whilst the Bloomberg whisper is just 120k despite an uplift after Wednesday’s stronger than expected ADP report. A return of 15k returning strikers and more favorable weather clashes with likely further government layoffs (albeit possibly modest) and broader hiring caution.

MNI STIR: ISM Services Helps Push Over 120bp Of Fed Easing For The Cycle

- A 2pt miss for ISM Services including a particularly weak employment sub-component has pushed Fed Funds implied rates lower still. It’s a relatively small additional move though (Dec’25 implied rate 3bps lower post-data) having already slid ahead of the release.

- Cumulative cuts from 4.33% effective: 9.7bp May, 25.8bp Jun, 44.8bp Jul and 92.4bp Dec.

- The Dec’25 implied rate is now 15bp lower on the day but negative growth impacts from tariff continue to be seen more heavily further out with the SFRZ6 implied yield some 28bp lower on the day in particularly fluid trading.

- The terminal yield is seen in that Dec’26 contract as of today, at 3.12% implying ~120bp of cuts ahead, vs 3.395% in the Sep’26 as of yesterday.

MNI US DATA: ISM Services: Weak New Orders And Employment Send Cautious Econ Signal

March's ISM Services report showed well below-expected activity measures, alongside a softer-than-expected reading on prices. This wasn't an outright negative report, with an expansionary overall reading and mixed comments about the impact of government policy shifts including tariffs, but it certainly casts a more cautious light on the services sector than February's solid ISM data.

- The below-consensus headline reading of 50.8 (52.9 survey) was a big step back from 53.5 in February, though was in line with MNI's expectation for a disappointing figure, given poor regional Fed activity readings for the month (US OUTLOOK/OPINION: Services Activity Dropped Sharply In March, Apr 1).

- The subindices also showed broad weakness: new orders fell to 50.4 (51.9 survey, 52.2 prior), the 3rd-lowest since May 2020 (ie Covid pandemic), while of note ahead of Friday's employment report, the Employment reading fell to 46.2 (2nd weakest since July 2020, after February's was the highest since December 2021), echoing the dip in the Manufacturing ISM.

- Business Activity/production rose 1.5 points to 55.9 (with at least one anecdote of tariff front-loading), while Supplier Deliveries registered 50.6 , 2.8 points down from February (indicating slower supplier delivery performance).

- New export orders fell 6.3 points to 45.8, weakest since March 2023 and like the above, one of the weakest months in years.

- Unlike the Manufacturing ISM, price pressures remained subdued, with Prices Paid unexpectedly falling to 60.9 (63.1 survey, 62.6 prior), though again this lack of upside price pressures was largely flagged by regional Fed services surveys.

- The impact of tariffs was actually more mixed than we've seen elsewhere, per the report: "There has been a significant increase this month in the number of respondents reporting cost increases due to tariff activity. Despite an increase in comments on tariff impacts and continuing concerns over potential tariffs and declining governmental spending, there was a close balance in near-term sentiment, between panelists with good outlooks and those seeing or expecting declines."

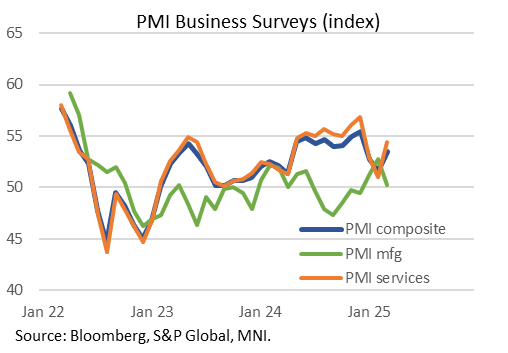

MNI US DATA: March Services PMI: Confidence Weaker But Positive, Activity Picks Up

Final March Services PMI was revised up 0.1 points from flash to 54.4, reflecting a strong improvement from 51.0 in February. The Composite reading was unchanged at 53.5 (despite an increase in Manufacturing PMI in the final to 50.2 from 49.9, per data out earlier in the week). The main headlines from the S&P Global Services PMI release: "Activity and new business growth both pick up…although sentiment about the future remains downbeat...Cost inflation up to 18-month high".

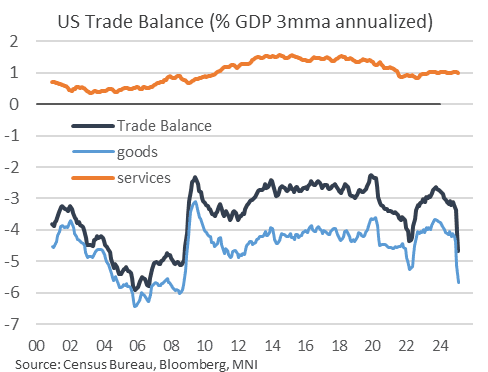

MNI US DATA: Even Gold Aside, Trade Deficits Were Wide Through February

The US trade deficit remained unusually wide in February at $122.7B (after $130.7B prior, downwardly revised from $131.4B). That was slightly smaller than expected ($123.5B survey), though the difference was accounted for by the January revision. Goods exports picked up 4.8% M/M with services declining 0.4% (first fall since June 2024), while goods imports dipped 0.2% (after +12.3% in January), with services imports growth steady at 0.7%.

- Goods imports outside of the "industrial supplies and materials" haven't really picked up much in nominal terms early 2025, not even automobiles (still running around $37-38B monthly), though consumer goods show signs of tariff front-running ($80.7B February deficit, a single-month record, after $78.3B in January), and the overall goods import rises in real terms have been strong vs weak exports.

- In terms of GDP, the 3month moving average of the trade deficit has risen to around 4.7% of GDP, a post-2008 high and up from 2.9% a year earlier. The goods deficit is running at 5.7% of GDP the last 3 months, well up from 4.2% in November, with Services continuing to run its long-standing 1.0% of GDP surplus.

- And from a tariffs perspective, the biggest bilateral goods trade balance deterioration appears gold-related (eg deficit with Switzerland of 0.7% of US GDP over the last 3 months, vs a longer-term average of 0.1%).

- The 12-month rolling goods trade deficits with Canada (0.2% of GDP), Mexico (0.6%), the EU (0.8%), and China (1.0%) are all fairly steady over the last few months, though have gotten slightly larger since the start of 2024.

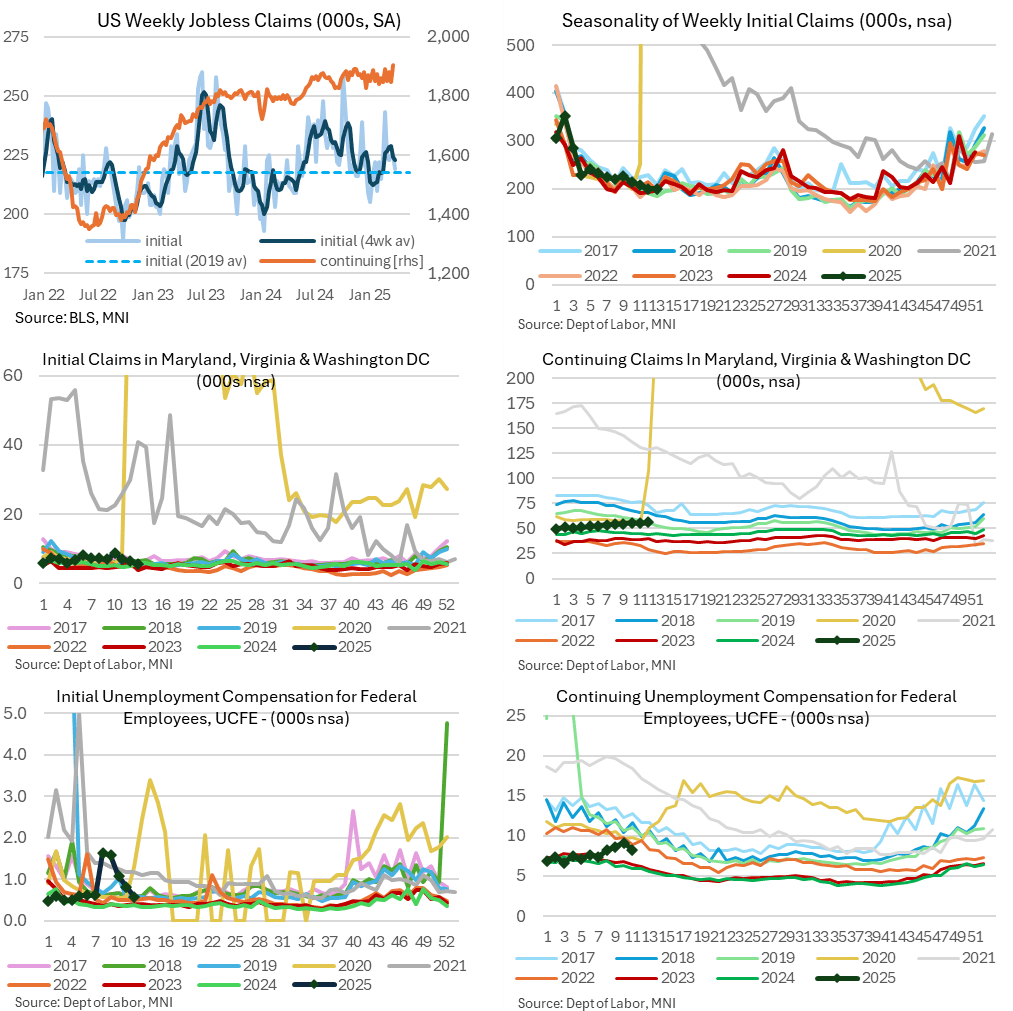

MNI US DATA: Claims Data Show Some Signs Of Rehiring Lethargy

Initial claims showed no sign of increase (as opposed to the sharp rise in Challenger job cut announcements) but continuing claims are showing evidence of slowing re-hiring.

- Initial jobless claims were lower than expected at 219k (sa, cons 225k) in the week to Mar 29 after a marginally upward revised 225k (initial 224k). Continuing claims were higher than expected at 1903k (sa, cons 1870k) in the week to Mar 22, for a sizeable increase from a downward revised 1847k (initial 1856k).

- It pokes above recent highs of 1892k seen a few times since November for a new high since late 2021.

- This doesn’t look like a DOGE-related push higher, at least not directly from a federal government layoff angle. Non-seasonally adjusted data show no sign of a marked increase in continuing claims in Maryland, Virginia & Washington DC (those with greatest reliance on federal government) whilst the UCFE program, which is lagged another week later than most continuing data, actually dipped ~1k to 8.2k.

- Whilst continuing claims have pushed higher most recently, its translation to payrolls reference periods will look more encouraging. The downward revised 1847k leaves it unchanged from the February payrolls reference period and close to the 1849k in Jan for an improvement from 1882k in Dec.

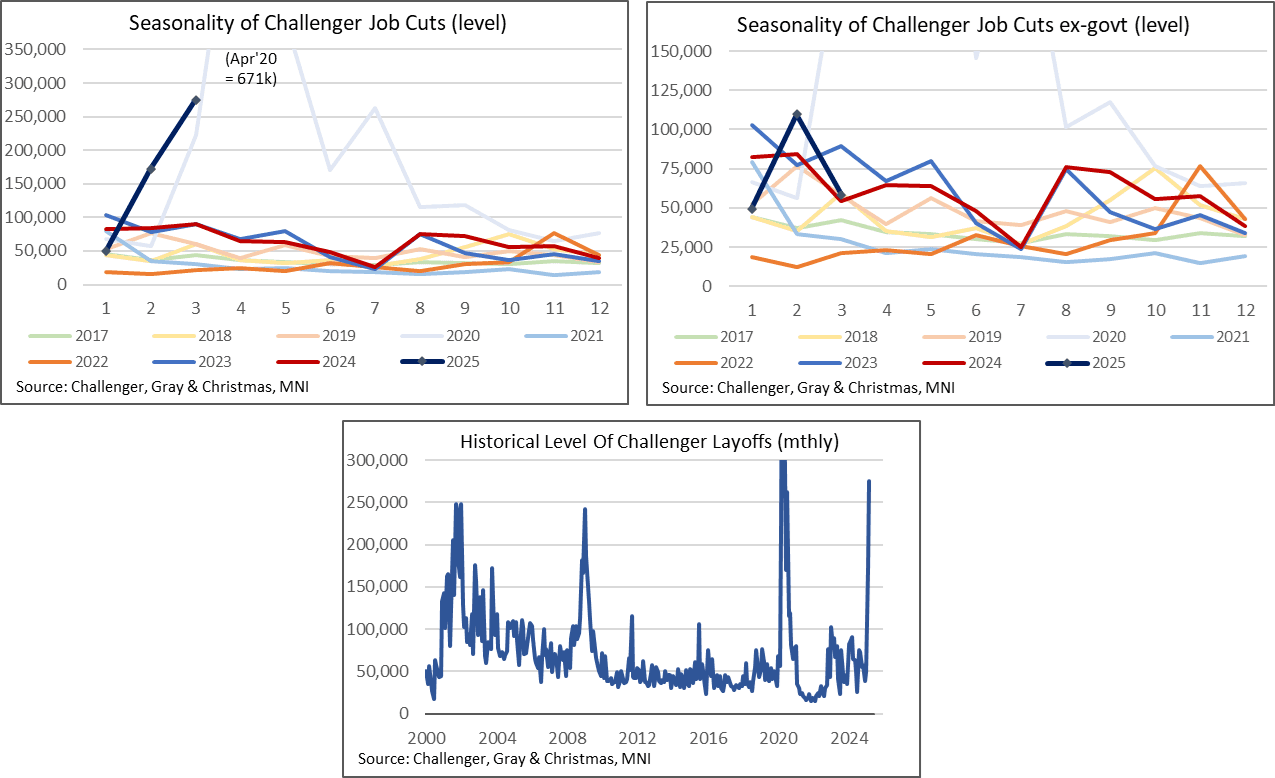

MNI US DATA: Challenger Job Cut Announcements Surge On DOGE Layoffs

- Challenger job cut announcements surged further in March, with the report specifically noting that most of the March job cuts were attributed to DOGE streamlining. Job cut announcements increased to 275k (205% Y/Y) after 172k in Feb (103% Y/Y) and 50k (-40% Y/Y) in Jan. It was driven by government layoffs jumping to 217k after 62k in Feb and 0.3k in Jan.

- With the risk that comes with omitting any industry that sees a sharp increase, it’s still notable that job cut announcements ex government looks less troubling this time. They stood at 58k in March (7% Y/Y) having jumped to 110k in Feb (30% Y/Y) after 50k in Jan (-40% Y/Y).

- Challenger summary of DOGE cuts (from the full report here): “Over the last two months, DOGE actions have been attributed to 280,253 layoff plans of federal workers and contractors impacting 27 agencies, according to Challenger tracking. Another 4,429 job cuts have come from the downstream effect of cutting federal aid or ending contracts, impacting mostly Non-Profits and Health organizations.”

- And specifically on DOGE cuts and recalled workers:

- “Challenger attempted to track the federal layoff plans that were rescinded and found 3,972. This figure was included in the report’s hiring plans. It is unclear if all workers who were recalled returned to their positions.

- Separately, the administration attempted to cut tens of thousands of probationary employees, 24,000 of whom were recalled, according to court filings. This matter is still undergoing legal challenges. Challenger did not count probationary employee cuts as a whole and therefore, did not include the recalled probationary employees in its hiring totals. It is possible that some probationary employees were included in individual agency layoff plans.”

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA down 1657 points (-3.92%) at 40567.07

S&P E-Mini Future down 270.75 points (-4.74%) at 5439.5

Nasdaq down 1037.6 points (-5.9%) at 16562.41

US 10-Yr yield is down 8.7 bps at 4.0436%

US Jun 10-Yr futures are up 39.5/32 at 112-23.5

EURUSD up 0.0165 (1.52%) at 1.1019

USDJPY down 2.93 (-1.96%) at 146.35

WTI Crude Oil (front-month) down $4.93 (-6.87%) at $66.78

Gold is down $32.38 (-1.03%) at $3102.98

European bourses closing levels:

EuroStoxx 50 down 190.67 points (-3.59%) at 5113.28

FTSE 100 down 133.74 points (-1.55%) at 8474.74

German DAX down 673.45 points (-3.01%) at 21717.39

French CAC 40 down 259.85 points (-3.31%) at 7598.98

US TREASURY FUTURES CLOSE

3M10Y -6.987, -25.473 (L: -30.172 / H: -20.255)

2Y10Y +7.496, 33.734 (L: 24.752 / H: 33.99)

2Y30Y +13.948, 77.436 (L: 63.195 / H: 77.694)

5Y30Y +11.935, 73.523 (L: 62.191 / H: 74.18)

Current futures levels:

Jun 2-Yr futures up 12.625/32 at 103-31.75 (L: 103-24 / H: 104-00.875)

Jun 5-Yr futures up 29.75/32 at 109-6.25 (L: 108-23 / H: 109-12.75)

Jun 10-Yr futures up 1-07.5/32 at 112-23.5 (L: 112-05.5 / H: 113-02)

Jun 30-Yr futures up 1-17/32 at 119-17 (L: 119-03 / H: 120-05)

Jun Ultra futures up 1-13/32 at 124-29 (L: 124-18 / H: 126-19)

MNI US 10YR FUTURE TECHS: (M5) Resumes Its Uptrend

- RES 4: 113-26+ 2.000 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 3: 113-23 76.4% of the Sep 11 ‘24 - Jan 13 bear cycle (cont)

- RES 2: 113-05 1.764 proj of the Jan 13 - Feb 7 - Feb 12 price swing

- RES 1: 113-02 Intraday high

- PRICE: 112-25.5 @ 1019 ET Apr 3

- SUP 1: 111-17+/110-28+ High MAr 20 / 20-day EMA

- SUP 2: 110-12+ 50-day EMA

- SUP 3: 110-06 Low Mar 27

- SUP 4: 110-00 High Feb 7 and a key support

Treasury futures have traded sharply higher today and in the process confirmed a clear break of resistance at 112-01, the Mar 4 high. The break confirms a resumption of the uptrend that started mid-January. The move higher sets the scene for an extension towards 113-05, a Fibonacci projection point, and 113-23, a Fibonacci retracement on the continuation chart. Initial firm support lies at 110-28+, the 20-day EMA.

SOFR FUTURES CLOSE

Jun 25 +0.090 at 95.985

Sep 25 +0.160 at 96.340

Dec 25 +0.220 at 96.595

Mar 26 +0.255 at 96.760

Red Pack (Jun 26-Mar 27) +0.270 to +0.285

Green Pack (Jun 27-Mar 28) +0.230 to +0.255

Blue Pack (Jun 28-Mar 29) +0.195 to +0.225

Gold Pack (Jun 29-Mar 30) +0.165 to +0.190

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00184 to 4.32114 (-0.00251/wk)

- 3M +0.00735 to 4.28469 (-0.01292/wk)

- 6M +0.01341 to 4.17789 (-0.03772/wk)

- 12M +0.01995 to 3.97115 (-0.08171/wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.37% (-0.02), volume: $2.555T

- Broad General Collateral Rate (BGCR): 4.34% (-0.01), volume: $983B

- Tri-Party General Collateral Rate (TCR): 4.34% (-0.01), volume: $952B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $258B

FED Reverse Repo Operation

RRP usage retreats to $196.265B this afternoon from $233.488B on Wednesday. Usage had surged to the highest level since December 31, 2024 this last Monday: $399.167B. Compares to $58.770B (lowest level since mid-April 2021) on February 14. The number of counterparties at 46.

PIPELINE

No new corporate bonds Thursday, issuers sidelined in the aftermath of late Wednesday's reciprocal tariff announcement. Summary from Wednesday:

- Date $MM Issuer (Priced *, Launch #)

- 04/02 $3.4B #Holcim Finance $700M 2Y +70, $700M 3Y +80, $1B 5Y +100, $1B 10Y +120

- 04/02 $1B Patterson Cos 7NC3 investor calls

MNI BONDS: EGBs-GILTS CASH CLOSE: Sizeable Bull Steepening On US Tariffs

Core European FI soared with semi-core/periphery spreads widening Thursday in a flight-to-safety move.

- The dominant force throughout the session was Wednesday evening's US tariff announcement, which proved much harsher on global trading partners than expected overall.

- Equities fell sharply, boosting rate cut pricing globally and driving a bid for core bonds.

- Weak US Services ISM data deepened the risk-off sentiment, and yields would close near the session lows.

- Curves bull steepened. 2Y German yields saw their lowest close since early December, with UK 2s lowest since October.

- Periphery instruments couldn't keep up with the Bund rally, with Iberian paper underperforming (SPGBs/PGBs around 3bp wider of Bund).

- Looking ahead, Friday's data slate includes German factory orders.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 9bps at 1.948%, 5-Yr is down 9.5bps at 2.233%, 10-Yr is down 7bps at 2.651%, and 30-Yr is down 3bps at 3.042%.

- UK: The 2-Yr yield is down 15.9bps at 4.01%, 5-Yr is down 16.3bps at 4.094%, 10-Yr is down 12bps at 4.52%, and 30-Yr is down 6.6bps at 5.184%.

- Italian BTP spread up 2.6bps at 112.1bps / Spanish up 2.9bps at 65.3bps

MNI FOREX: USD Index Sharply Lower as US Trade Policy Shakes Global Markets

- Analysts continue to cite the most recent US tariff announcements as a pivotal turning point for global trade policy. While risk sentiment has been negatively impacted, US pessimism reverberated into global currency markets, with dollar indices sharply lower on the session.

- The ICE dollar index is off its worst levels, but is broadly consolidating a 1.75% decline on Thursday, currently trading around the 102.00 mark. This is just 2% above the 2024 lows, marking the significance of the pullback across 2025 so far, and the close proximity to significant medium-term objectives.

- Standing out have been the moves for the dollar against the low yielding safe havens. USDJPY remains down 2.1% despite a 100 pip bounce off the 145.20 lows. AS for USDCHF, spot remains 2.5% lower on the day, having breached the US election inspired lows at 0.8615, and extending as low as 0.8547.

- EURUSD also had a very aggressive move higher in late European trade, with liquidity evaporating on a swift move above 1.11. Spot reached as high as 1.1147 before stabilising, but remains on course for a move to a cluster of highs around the 1.12 mark. At one point, EURUSD was registering its biggest intra-day advance since 2015.

- Weaker sentiment in equity markets have offset the appreciations for the likes of AUD, NZD and GBP, only advancing between 0.75-1.00% today.

- Emphasising the broad dollar weakness, even the Mexican peso has rallied one percent, bolstered by the relatively lenient outcome for the nation of the US liberation day announcements. The Bloomberg dollar index, which includes a broader basket of currencies, notably fell below the US election lows, and is now 5.5% below the February highs.

- The US employment report will be the highlight on Friday’s economic data calendar. Additionally, subsequent comments from Fed Chair Powell will be eagerly awaited given the recent turbulence in markets.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/04/2025 | 0545/0745 | ** | Unemployment | |

| 04/04/2025 | 0600/0800 | Flash CPI | ||

| 04/04/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/04/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 04/04/2025 | 0630/0730 | DMO announce Apr-Jun issuance operations | ||

| 04/04/2025 | 0645/0845 | * | Industrial Production | |

| 04/04/2025 | 0700/0900 | ** | Industrial Production | |

| 04/04/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/04/2025 | 0800/1000 | * | Retail Sales | |

| 04/04/2025 | 0800/1000 | ECB's De Guindos Gives Lecture In Barcelona | ||

| 04/04/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/04/2025 | 1230/0830 | *** | Employment Report | |

| 04/04/2025 | 1525/1125 | Fed Chair Jerome Powell | ||

| 04/04/2025 | 1600/1200 | Fed Governor Michael Barr | ||

| 04/04/2025 | 1645/1245 | Fed Governor Chris Waller | ||

| 04/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 04/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |