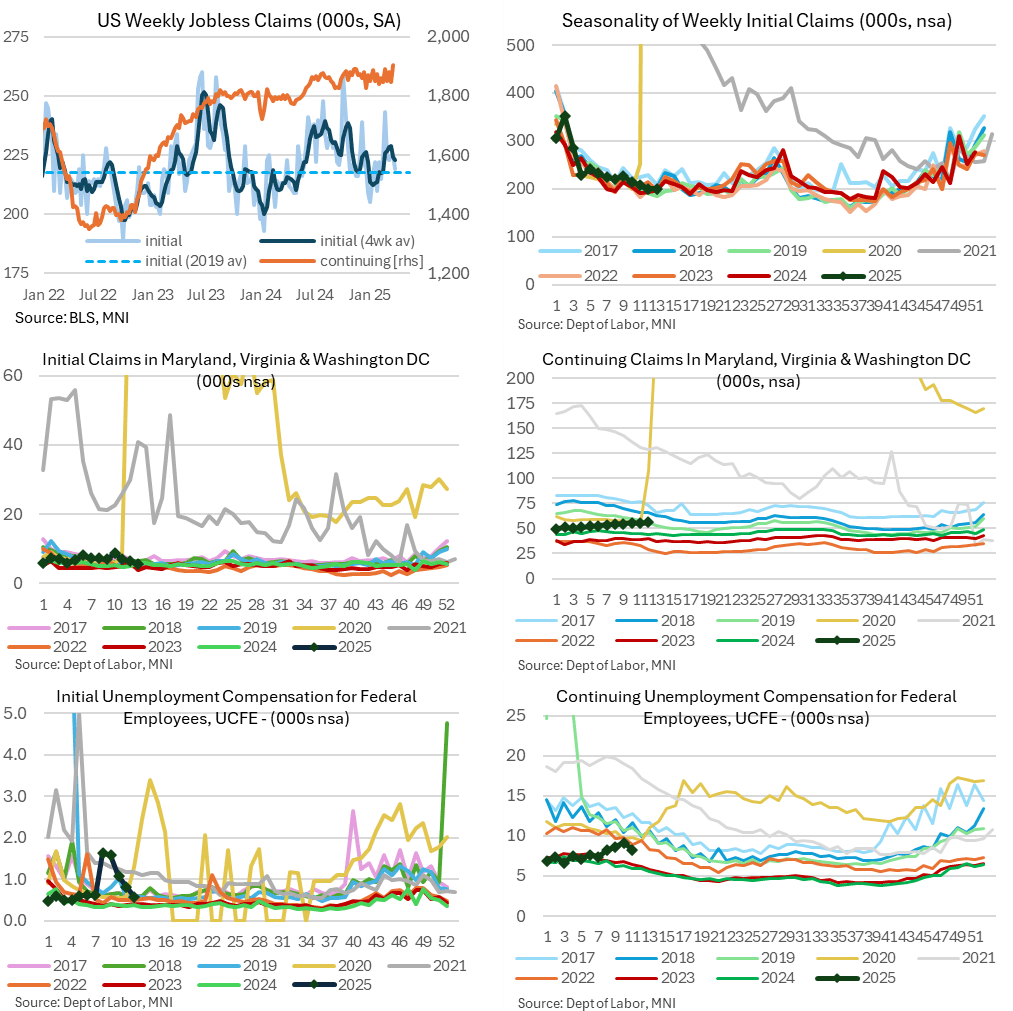

US DATA: Claims Data Show Some Signs Of Rehiring Lethargy

Initial claims showed no sign of increase (as opposed to the sharp rise in Challenger job cut announcements) but continuing claims are showing evidence of slowing re-hiring.

- Initial jobless claims were lower than expected at 219k (sa, cons 225k) in the week to Mar 29 after a marginally upward revised 225k (initial 224k).

- The four-week average fell 1k to 223k to a new lows since mid-Feb, close to the 218k in 2019 for our usual marker of a previously tight labor market.

- Continuing claims were higher than expected at 1903k (sa, cons 1870k) in the week to Mar 22, for a sizeable increase from a downward revised 1847k (initial 1856k).

- It pokes above recent highs of 1892k seen a few times since November for a new high since late 2021.

- This doesn’t look like a DOGE-related push higher, at least not directly from a federal government layoff angle. Non-seasonally adjusted data show no sign of a marked increase in continuing claims in Maryland, Virginia & Washington DC (those with greatest reliance on federal government) whilst the UCFE program, which is lagged another week later than most continuing data, actually dipped ~1k to 8.2k.

- Whilst continuing claims have pushed higher most recently, its translation to payrolls reference periods will look more encouraging. The downward revised 1847k leaves it unchanged from the February payrolls reference period and close to the 1849k in Jan for an improvement from 1882k in Dec.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK: CX Looks To Facilitate Military Procurement w/Voter Concerns Over Defence Up

At ~1425GMT (0925ET, 1525CET), Chancellor of the Exchequer Rachel Reeves will take part in a fireside chat at the MakeUK manufacturers' association conference. Reports claim Reeves intends to use the event to “fire up Britain’s industrial base” to boost arms production and to cut red tape to facilitate faster procurement of defence equipment.

- The latest 'important issues' opinion poll from YouGov shows defence and security leaping as one of the top issues facing the country. In the 1-3 March survey, the three most important issues in the minds of respondents remained the same; the economy was raised by 51% of respondents (down 3% from 22-23 Feb), immigration by 46% (+1) and healthcare 38% (+1). Defence and security came in fourth place, raised by 31% of respondents (+4%). This figure is the highest since Russia launched its full-scale invasion of Ukraine in Feb 2022.

- The increased public concern about the UK's defence outlook could ease pressure on PM Sir Keir Starmer after some within his centre-left Labour Party criticised his gov'ts decision to cut aid spending to boost the UK's military capacity, sparking the resignation of one minister.

- Reuters reports comments from the PM's spox. Confirms Starmer held a call with US President Donald Trump on the evening of 3 March. Spox does not confirm if Starmer was informed of Trump's impending decision to pause aid to Ukraine, instead saying, "The prime minister and President Trump are focused on the same outcome, which is delivering a secure and lasting peace in Ukraine".

US TSY FUTURES: BLOCK: June'25 5Y Buy

- +5,000 FVM5 108-12.75, buy through 108-12.5 post time offer at 0726:20ET, DV01 $205,000. The 5Y contract trades 108-11.5 last (+8.75).

FOREX: Markets Happy to Sell Into Already Weak USD Market at NY Crossover

As was the case yesterday, US markets are extending the weaker USD theme at the crossover and pushing the USD Index to fresh lows. This is helping the latest bidtone in both EUR/USD (testing 1.0550) and GBP/USD (testing 1.2750) to mark a new YTD high across both pairs

- How much further could the USD downdraft go? We remain ~1.75% higher in the USD Index relative to election results day in November, and 5.75% above the September lows. This leaves 105.178 as a key level ahead - the 50% retracement of the Trump-tied rally off last year's lows, which would equate to (approximately) 1.0630 for EUR/USD.

- Tariff target currencies are performing very well, despite tariff pressure, with MXN 1% off overnight lows, USD/CNH on track to post the biggest daily downtick since January and - perhaps most impressively given oil prices - USD/CAD over 125 pips off the Monday high.

- Yesterday's closing volumes were solid for currency futures (EUR futures saw daily turnover of 40% above average) and that will likely be repeated today - with volatile spot markets driving participation.