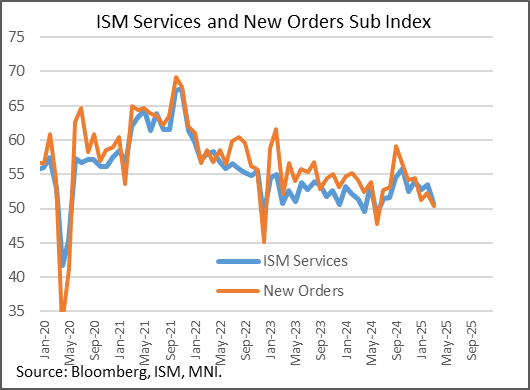

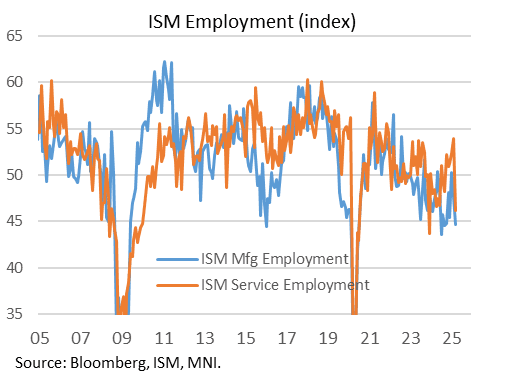

US DATA: ISM Services: Weak New Orders And Employment Send Cautious Econ Signal

March's ISM Services report showed well below-expected activity measures, alongside a softer-than-expected reading on prices. This wasn't an outright negative report, with an expansionary overall reading and mixed comments about the impact of government policy shifts including tariffs, but it certainly casts a more cautious light on the services sector than February's solid ISM data.

- The below-consensus headline reading of 50.8 (52.9 survey) was a big step back from 53.5 in February, though was in line with MNI's expectation for a disappointing figure, given poor regional Fed activity readings for the month (US OUTLOOK/OPINION: Services Activity Dropped Sharply In March, Apr 1).

- The subindices also showed broad weakness: new orders fell to 50.4 (51.9 survey, 52.2 prior), the 3rd-lowest since May 2020 (ie Covid pandemic), while of note ahead of Friday's employment report, the Employment reading fell to 46.2 (2nd weakest since July 2020, after February's was the highest since December 2021), echoing the dip in the Manufacturing ISM.

- Business Activity/production rose 1.5 points to 55.9 (with at least one anecdote of tariff front-loading), while Supplier Deliveries registered 50.6 , 2.8 points down from February (indicating slower supplier delivery performance).

- New export orders fell 6.3 points to 45.8, weakest since March 2023 and like the above, one of the weakest months in years.

- Unlike the Manufacturing ISM, price pressures remained subdued, with Prices Paid unexpectedly falling to 60.9 (63.1 survey, 62.6 prior), though again this lack of upside price pressures was largely flagged by regional Fed services surveys.

- The impact of tariffs was actually more mixed than we've seen elsewhere, per the report: "There has been a significant increase this month in the number of respondents reporting cost increases due to tariff activity. Despite an increase in comments on tariff impacts and continuing concerns over potential tariffs and declining governmental spending, there was a close balance in near-term sentiment, between panelists with good outlooks and those seeing or expecting declines."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: Belgium Long 15-year Jun-42 OLO: Priced

- Reoffer price 99.41 to yield 3.497%

- Size: E5bln (MNI had expected E4-6bln)

- Books in excess of E37bln (ex JLM interest)

- Maturity: June 22, 2042

- Spread set earlier at 0.40% Jun-40 OLO +8bp (guidance was +10bp area)

- Books above EU37b (excluding JLM interest): Leads

- Coupon: 3.45%, annual, act/act, short first

- Settlement: March 11 2025 (T+5)

- ISIN: BE0000364738

- Bookrunners: BNPP, CA-CIB, DB, HSBC (B&D), MS

- Timing: FTT immediately

From market source, Bbg, DJ

ECB: 2025/26 GDP Growth Expected To Be Revised Lower In March Projection Round

Analysts expect the ECB to revise its 2025 and 2026 growth projections lower in the March forecast round, while technical assumptions are likely to push the 2025 headline projection a touch higher.

- The median of analyst estimates compiled by MNI expect the 2025 real GDP growth projection at 0.9%, two tenths below the 1.1% seen in the December round. This reflects carry-over from the weaker-than-expected Q4 flash GDP print (0.1% Q/Q vs 0.2% projected in December) and subdued activity signals at the start of 2025.

- Most analysts (with the exception of Deutsche Bank and Morgan Stanley) do not expect the ECB to incorporate potential tariff-related impacts into its projections.

- 2026 GDP is expected to be revised a tenth lower to 1.3%, but RBC instead expect an upgrade to 1.5% (mainly due to exchange rate technical assumptions).

- The cut-off date for the ECB’s technical assumptions (e.g. energy prices, exchange rate) is expected to be between Feb 7 – Feb 12. Analysts expect high gas prices and a weaker exchange rate to push the headline projection up a tenth to 2.2% (Morgan Stanley expect 2.4%). 2026 and 2027 headline projections are expected unchanged at 1.9% and 2.1% respectively.

- Analysts generally expect minimal changes to the core inflation projections through 2025-2027 (2025: 2.3%, 2026: 1.9%, 2027: 1.9$).

- Note: The March projections are compiled by ECB staff, while the December round was compiled by Eurosystem (i.e. National Central Bank) staff.

GERMANY: Bundesbank Publishes Debt Brake Reform Proposal

Bundesbank presents debt brake reform proposal - which would allow for extra spending through 2030 conditional on debt ratio:

- Specifically, under the proposal, "the federal and state governments would be able to spend up to a total of EUR 220 billion additionally financed by loans, provided that the debt ratio is below 60%. With a debt ratio of more than 60 percent, this framework would be limited to around 100 billion euros by 2030."

- The proposal "shows a stability-oriented path for higher government investment. It thus presents a concept that supports necessary measures to strengthen infrastructure and defence and at the same time ensures long-term sustainable public finances in line with European requirements. At the same time, it maintains its position that constitutionally secured debt brakes make an indispensable contribution to long-term sustainable public finances."

- A debt brake reform would likely be distinct to the currently discussed one-off defence funds in Germany.

- Link to full pdf here.