US DATA: Challenger Job Cut Announcements Surge On DOGE Layoffs

Apr-03 11:59

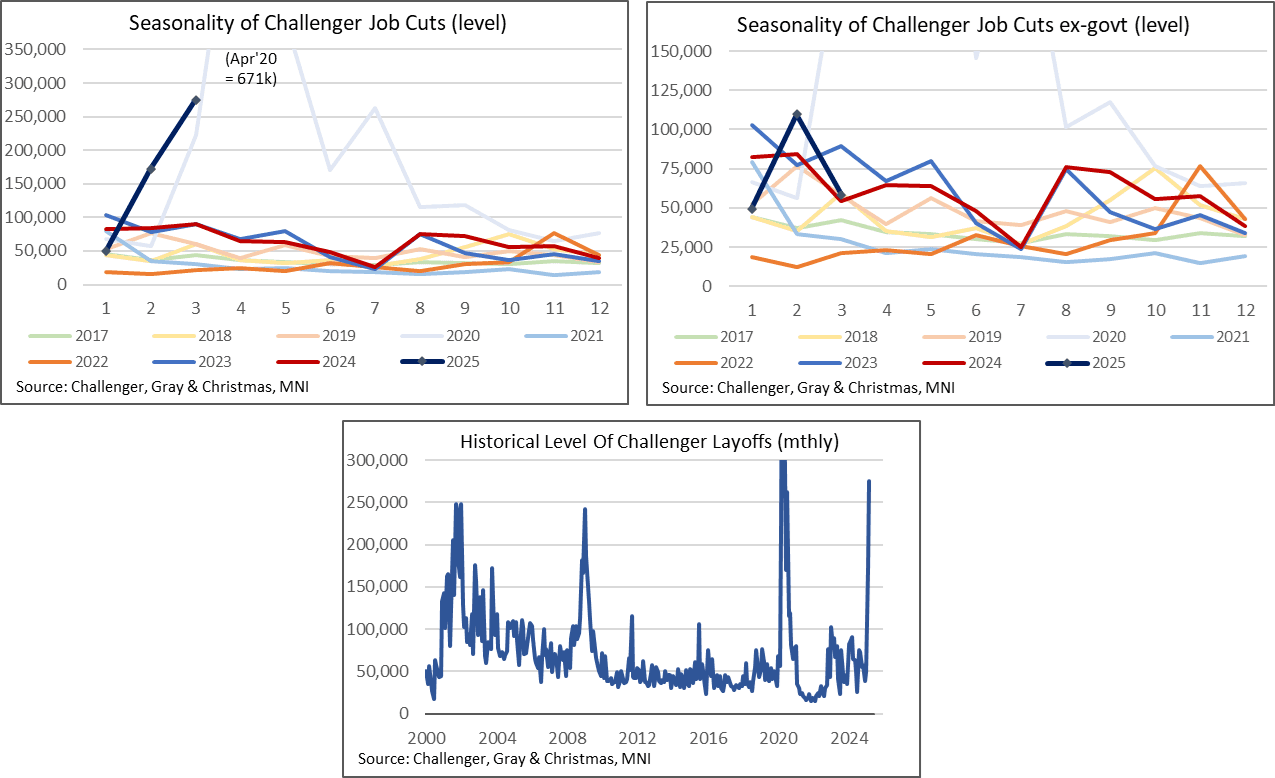

- Challenger job cut announcements surged further in March, with the report specifically noting that most of the March job cuts were attributed to DOGE streamlining.

- Job cut announcements increased to 275k (205% Y/Y) after 172k in Feb (103% Y/Y) and 50k (-40% Y/Y) in Jan.

- It was driven by government layoffs jumping to 217k after 62k in Feb and 0.3k in Jan.

- With the risk that comes with omitting any industry that sees a sharp increase, it’s still notable that job cut announcements ex government looks less troubling this time. They stood at 58k in March (7% Y/Y) having jumped to 110k in Feb (30% Y/Y) after 50k in Jan (-40% Y/Y).

- Challenger summary of DOGE cuts (from the full report here): “Over the last two months, DOGE actions have been attributed to 280,253 layoff plans of federal workers and contractors impacting 27 agencies, according to Challenger tracking. Another 4,429 job cuts have come from the downstream effect of cutting federal aid or ending contracts, impacting mostly Non-Profits and Health organizations.”

- And specifically on DOGE cuts and recalled workers:

- “Challenger attempted to track the federal layoff plans that were rescinded and found 3,972. This figure was included in the report’s hiring plans. It is unclear if all workers who were recalled returned to their positions.

- Separately, the administration attempted to cut tens of thousands of probationary employees, 24,000 of whom were recalled, according to court filings. This matter is still undergoing legal challenges. Challenger did not count probationary employee cuts as a whole and therefore, did not include the recalled probationary employees in its hiring totals. It is possible that some probationary employees were included in individual agency layoff plans.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: /SWAPS: Modest Upside Pressure In 30-year Bunds Post Syndi Mandate

Mar-04 11:59

Modest upside pressure in 30-year Bund yields following the syndication mandate, helping the 5s30s curve reach its steepest level since July 2022, now up 6.0bps today at 64.7bps.

- The long-end German syndication has been on the cards for some time, but we had little conviction over the timing. The previously uncertain timing is what’s driving the immediate market reaction.

- Buxl ASW (vs 3-month Euribor) remains within this morning’s range at -43.7bps. The contained reaction probably reflects already short positioning in spreads, particularly given existing week-to-date tightening on the back of increased German defence spending prospects.

OUTLOOK: Price Signal Summary - WTI Heads South

Mar-04 11:58

- On the commodity front, the latest pullback in Gold appears to be a correction. The move through the 20-day EMA does signal scope for an extension towards the next important support around the 50-day EMA, at $2808.1. However, Monday’s gains are a positive development and potentially an early reversal signal. A stronger rally would refocus attention on the next objective at $2962.2, a 2.00 projection of the Nov 14 - Dec 12 - 19 price swing. This would also open the $3000.0 handle.

- In the oil space, the current bearish condition in WTI futures remains intact and this week’s fresh short-term cycle low reinforces current conditions. Recent weakness has resulted in a clear breach of support at $70.20, the Feb 6 low. This confirmed a resumption of the downtrend that started Jan 15 and paves the way for an extension towards $66.41 next, the Dec 6 ‘24 low. Key short-term resistance is at $73.33, the Feb 11 high. Initial resistance is at $71.16, the 50-day EMA.

EGB SYNDICATION: Belgium Long 15-year Jun-42 OLO: Final terms

Mar-04 11:54

- Size: E5bln (MNI had expected E4-6bln)

- Books in excess of E37bln (ex JLM interest)

- Maturity: June 22, 2042

- Spread set earlier at 0.40% Jun-40 OLO +8bp (guidance was +10bp area)

- Books above EU37b (excluding JLM interest): Leads

- Coupon: Short first

- Settlement: March 11 2025 (T+5)

- ISIN: BE0000364738

- Bookrunners: BNPP, CA-CIB, DB, HSBC (B&D), MS

From market source, Bbg, DJ