MNI ASIA OPEN: Jackson Hole Assuages Market Fears - For Now

EXECUTIVE SUMMARY

- MNI FED: Boston's Collins: September Cut Not A Done Deal

- MNI FED: Powell Plays Up Employment Risks In Eyeing Potential Policy Adjustment

- MNI FED: New Monetary Policy Statement Ends Flexible Average Inflation Targeting

- MNI: US Debt-To-GDP At 250% May Not Push Up Rates - JH Paper

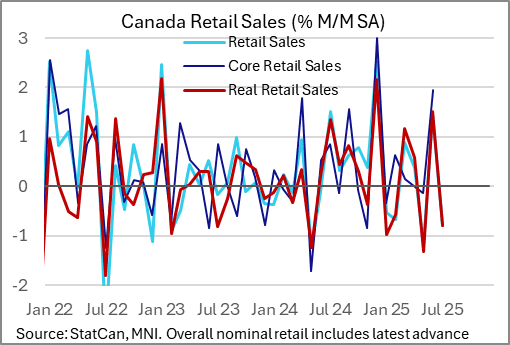

- MNI CANADA DATA: June Retail Sales Confirmed Solid, But July Flash Bodes Ill For Q3

- MNI US DATA: Dallas Fed's Weekly Growth Index Continues To Edge Up

US

MNI FED: Powell Plays Up Employment Risks In Eyeing Potential Policy Adjustment

The major near-term policy signal takeaway from Fed Chair Powell's Jackson Hole keynote (link) is that he only acknowledges that "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance", but also that the risks appear to have shifted since the July meeting ("The balance of risks appears to be shifting"), as "downside risks to employment are rising.

- Powell: "while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment."

MNI FED: New Monetary Policy Statement Ends Flexible Average Inflation Targeting

Also in Fed Chair Powell's speech (link) is a discussion of the changes to the Federal Reserve's Statement on Longer-Run Goals and Monetary Policy Strategy as part of the latest framework review (the last was in 2020, when the economic landscape looked very different). There don't appear to be any major surprises, as the review's conclusions have been well-telegraphed - below are Powell's explanation of all of the major changes, and the reasoning behind them. Below, we include a graphic comparing the new to the previous Statement on Longer-Run Goals and Monetary Policy Strategy (the new statement is available here).

NEWS

MNI: US Debt-To-GDP At 250% May Not Push Up Rates - JH Paper

The supply of U.S. debt over the next 75 years will eventually outstrip demand and force interest rates higher, though large fiscal adjustments could allow debt-to-GDP levels to increase sharply over time without pushing up interest rates, according to research presented Saturday to the Federal Reserve's annual economic symposium in Jackson Hole.

- "Our calculations suggest that, in 2100, the U.S. could sustain a debt-to-GDP ratio of 250% at the same interest rates as today. However, achieving this requires a fiscal adjustment of 10% of GDP or more in every plausible scenario," wrote economists Adrien Auclert, Hannes Malmberg, Matthew Rognlie, and Ludwig Straub, who use a supply-and-demand approach to analyze the trajectory of U.S. aggregate wealth, real interest rates, and fiscal sustainability.

MNI FED: Boston's Collins: September Cut Not A Done Deal

Boston Fed's Collins (2025 FOMC voter) sounds in this morning's Bloomberg TV interview at Jackson Hole as though she is increasingly concerned about the labor market as opposed to her earlier fears that inflation expectations could become unanchored amid tariff increases (echoing WSJ interview comments published Thursday evening).

- Nonetheless it also sounds like she will have to see more evidence of labor market deterioration to support easing, and says that a September cut is not a "done deal". Recall that this summer she suggested that her base case for rates was one cut by year-end as part of an "actively patient" policy.

- Collins: "The risks on the two sides have come into rough balance. So, that is a really complex context for monetary policy, when you could see the unemployment rate rising and you could see higher inflation. You know, my baseline is not one that is as concerned about inflation expectations rising at the moment. Earlier in the year I had more concerns about that.

MNI BRIEF: Trump - Will Fire Fed's Cook If She Doesn't Resign

President Donald Trump said Friday he will fire Federal Reserve Governor Lisa Cook if she does not resign from her position. “I’ll fire her if she doesn’t resign,” Trump told reporters at the Kennedy Center. “What she did was bad, so I’ll fire her if she doesn’t resign,” he said. A Justice Department official is set to probe Cook after she was accused by a member of President Donald Trump’s administration of committing mortgage fraud.

MNI TARIFFS: Canada To Remove Retaliatory Tariffs On 'Long List' Of US Products- BBG

Canadian Prime Minister Mark Carney is expected to announce today that Ottawa will remove retaliatory tariffs on a ‘long list’ of US products that comply with the USMCA trade agreement, a major policy shift that lays the groundwork for the upcoming USMCA review, per Bloomberg. According to Bloomberg, the move means “a broad range of [USMCA compliant] US-made consumer products will no longer face a 25% tariff when imported into Canada." Bloomberg notes Canada is likely to retain 25% import taxes on US steel/aluminium/automobiles.

US TSYS

MNI US TSYS: Fed Chair Powell: Shifting Risks May Warrant Policy Adjustment

- Treasuries look to finish near session highs following Fed Chairman Powell's dovish speech from the Jackson Hole, Wy symposium. Sep'25 10Y contract trades +19 at 112-04.5 after the bell vs. 112-08 high, 10Y yield -.0739 at 4.2537% vs. 4.2402% low.

- Technical resistance attention on 112-15+, the Aug 5 high and the bull trigger. Clearance of this hurdle would resume the uptrend and pave the way for a climb towards 112-23 initially, the May 1 high.

- The major near-term policy signal takeaway from Fed Chair Powell's Jackson Hole keynote (link) is that he only acknowledges that "with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance", but also that the risks appear to have shifted since the July meeting ("The balance of risks appears to be shifting"), as "downside risks to employment are rising.

- Boston Fed President Collins: Sep cut not a done deal as "risks on the two sides have come into rough balance. So, that is a really complex context for monetary policy, when you could see the unemployment rate rising and you could see higher inflation. You know, my baseline is not one that is as concerned about inflation expectations rising at the moment. Earlier in the year I had more concerns about that.

- Focus in the coming week shifts to any further policy signaling from central bank officials at Jackson Hole. BoE's Bailey, ECB's Lagarde, BoJ's Ueda, Riksbank's Thedeen and several more FOMC members are in attendance - meaning it should be a busy weekend for central bank commentary.

OVERNIGHT DATA

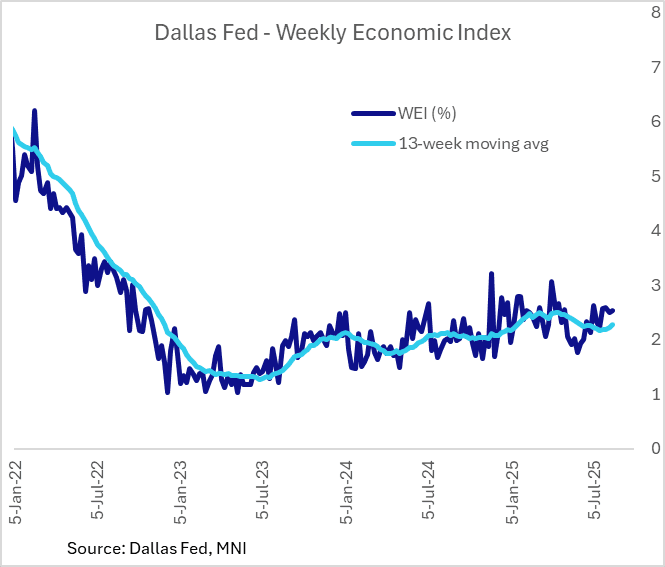

MNI US DATA: Dallas Fed's Weekly Growth Index Continues To Edge Up

The Dallas Fed's weekly economic index (WEI) for the week ended Aug 16 remained relatively stable at 2.54% vs 2.50% the week prior (the figures are scaled to

4-quarter GDP growth).

- But continued stabilization above 2.50% in recent weeks (vs sub-2% in May) brought the 13-week moving average up to 2.28% from 2.23% prior, a 4th-consecutive weekly acceleration for the highest since end-May.

- The latest estimates are consistent with steady growth or potentially a modest pickup in Q3 vs Q2, when 4-quarter GDP growth posted 2.0%.

MNI CANADA DATA: June Retail Sales Confirmed Solid, But July Flash Bodes Ill For Q3

June's retail sales report was extremely mixed, with strength at the end of Q2 offset by initial indications of a sharp pullback at the start of Q3. Retail sales rose by 1.5% M/M (nominal, SA) in June, a little lower than the 1.6% seen in the flash estimate, but still the strongest sequential reading since December 2024. However, more attention in this release is on the July flash estimate which indicates a contraction of 0.8% M/M. That would still leave retail sales above the May level, but below the end-2024 level in a fairly significant setback.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 826.5 points (1.85%) at 45612.02

S&P E-Mini Future up 90 points (1.41%) at 6478.75

Nasdaq up 374.7 points (1.8%) at 21476.29

US 10-Yr yield is down 7 bps at 4.2576%

US Sep 10-Yr futures are up 18/32 at 112-3.5

EURUSD up 0.0113 (0.97%) at 1.1719

USDJPY down 1.49 (-1%) at 146.88

Gold is up $31 (0.93%) at $3369.77

European bourses closing levels:

EuroStoxx 50 up 26.07 points (0.48%) at 5488.23

FTSE 100 up 12.2 points (0.13%) at 9321.4

German DAX up 69.75 points (0.29%) at 24363.09

French CAC 40 up 31.4 points (0.4%) at 7969.69

US TREASURY FUTURES CLOSE

3M10Y -2.721, 6.166 (L: 1.834 / H: 9.943)

2Y10Y +3.365, 56.338 (L: 51.246 / H: 58.069)

2Y30Y +6.716, 118.84 (L: 109.918 / H: 120.457)

5Y30Y +5.994, 112.013 (L: 104.746 / H: 112.638)

Current futures levels:

Sep 2-Yr futures up 5.375/32 at 103-29.625 (L: 103-23.125 / H: 103-30.875)

Sep 5-Yr futures up 13.5/32 at 109-0.75 (L: 108-18 / H: 109-03.25)

Sep 10-Yr futures up 18.5/32 at 112-4 (L: 111-15.5 / H: 112-08)

Sep 30-Yr futures up 24/32 at 114-26 (L: 113-29 / H: 115-04)

Sep Ultra futures up 23/32 at 117-14 (L: 116-17 / H: 117-28)

MNI US 10YR FUTURE TECHS: (U5) Support Remains Intact For Now

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5 and the bull trigger

- PRICE: 112-04 @ 1505ET Aug 22

- SUP 1: 111-12 50-day EMA

- SUP 2: 110-23+/08+ Low Aug 1 / Low Jul 15 & 16

- SUP 3: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

A bullish theme in Treasury futures remains intact and the contract continues to trade above support around the 50-day EMA, at 111-12. A clear break of this average would expose support at 110-23+, the Aug 1 low. For bulls, gains would refocus attention on 112-15+, the Aug 5 high and the bull trigger. Clearance of this hurdle would resume the uptrend and pave the way for a climb towards 112-23 initially, the May 1 high.

SOFR FUTURES CLOSE

Sep 25 +0.030 at 95.890

Dec 25 +0.085 at 96.225

Mar 26 +0.110 at 96.485

Jun 26 +0.115 at 96.730

Red Pack (Sep 26-Jun 27) +0.105 to +0.115

Green Pack (Sep 27-Jun 28) +0.095 to +0.10

Blue Pack (Sep 28-Jun 29) +0.090 to +0.090

Gold Pack (Sep 29-Jun 30) +0.080 to +0.090

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.32% (+0.01), volume: $2.702T

- Broad General Collateral Rate (BGCR): 4.30% (+0.01), volume: $1.132T

- Tri-Party General Collateral Rate (TCR): 4.31% (+0.01), volume: $1.109T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $117B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $263B

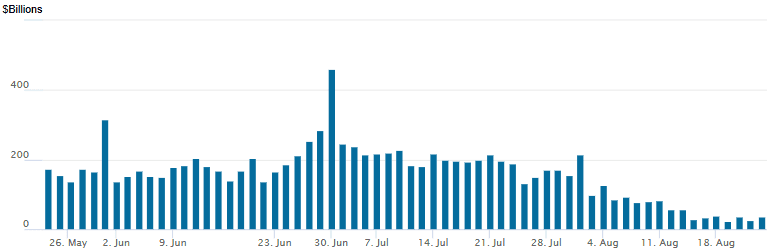

FED Reverse Repo Operation

RRP usage rises to $36.275B this afternoon from $25.358B yesterday -- compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021. Total number of counterparties at 16. This week's retreat compares this year's high usage of $460.731B on June 30.

MNI BONDS: EGBs-GILTS CASH CLOSE: Powell Ensures 10Y Yields Down On The Week

The highly-anticipated Jackson Hole speech by Federal Reserve Chair Powell brought a dovish message, spurring a rally across global FI Friday that included EGBs and Gilts.

- Bunds outperformed global peers in early trade, though moves were limited as markets awaited Powell's comments. German Q2 GDP was revised downward, with ECB Q2 negotiated wages broadly in line with tracking estimates.

- Yields dropped sharply in mid-afternoon trade as Powell signaled openness to a September Fed cut in more overt fashion than had been expected, noting a "shifting balance of risks may warrant adjusting our policy stance".

- Bund yields finished a little higher than the levels seen in the immediate aftermath of Powell's speech, but Gilt yields continued to fall, closing near session lows.

- A Bloomberg sources piece pointed to a September ECB hold, but markets took little impact with rate markets already pricing that in.

- The German and UK curves both bull flattened on the day, while periphery/semi-core EGB spreads tightened in a broader risk rally.

- For the week, the German curve bull flattened with the UK's twist flattening: UK 2Y +1.1bp, 10Y -0.3bp; German 2Y -2.5bp, 10Y -6.6bp.

- Saturday includes a panel at Jackson Hole with BOE's Bailey and ECB's Lagarde, with next week's calendar highlight being August flash Eurozone inflation data.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.4bps at 1.948%, 5-Yr is down 3.8bps at 2.277%, 10-Yr is down 3.5bps at 2.722%, and 30-Yr is down 1.8bps at 3.309%.

- UK: The 2-Yr yield is down 2.6bps at 3.944%, 5-Yr is down 2.3bps at 4.101%, 10-Yr is down 3.6bps at 4.693%, and 30-Yr is down 3bps at 5.548%.

- Italian BTP spread down 2bps at 80.4bps / French OAT down 1.2bps at 69.5bps

MNI FOREX: USD Breaks To August Lows as Markets Resolve Around Sept Fed Cut

- The USD sank sharply against all others on Friday, falling sharply following Powell's appearance at the Jackson Hole Policy Symposium. In acknowledging that the balance of risks to the US economy has shifted, he signaling a much higher likelihood of a rate cut at the Fed's September meeting - helping OIS markets resolve pricing and send the dollar lower in the process. Immediate strength in EUR/USD put the pair through yesterday's highs to narrow the gap with 1.1693, the next upside level intraday. The move coincides with a firm rally for equities - putting the E-mini S&P within range of the weekly high at 6484.25.

- The price action was backed up by a follow-up claim from Trump that he will fire Fed's Cook should she not resign - adding to the evidence that Trump may look to build a corner of policymakers within the FOMC that favour his view of lower rates for the US economy. Rates markets built in expectations for not just a September rate cut, but additional easy policy into year-end - with over 50bps now well priced.

- Second to USD weakness, CAD also trade poorly as softer oil prices countered any bullish signal from slightly better-than-expected retail sales data as well as Carney's decision to unilaterally remove retaliatory tariffs against US imports. Gains this week in USDCAD and the breach of resistance at 1.3879, the Aug 1 high, marked a positive development, however the slippage into the Friday close undermines this sentiment - for now. Moving average studies have crossed and are in a bull-mode position, reinforcing current conditions. An extension higher would signal scope for a climb towards 1.4019, a Fibonacci retracement. On the downside, support to watch lies at 1.3769, the 50-day EMA - a level not yet challenged by the correction lower.

- Focus in the coming week shifts to any further policy signaling from central bank officials at Jackson Hole. BoE's Bailey, ECB's Lagarde, BoJ's Ueda, Riksbank's Thedeen and several more FOMC members are in attendence - meaning it should be a busy weekend for central bank commentary. A UK Bank Holiday should keep markets set for a quieter start to the week, but German IFO, US consumer confidence, Australian CPI and European inflation numbers are all due - as well as NVIDIA's earnings release.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 25/08/2025 | 0700/0900 | ** | PPI | |

| 25/08/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/08/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 25/08/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 25/08/2025 | 1400/1000 | *** | New Home Sales | |

| 25/08/2025 | 1400/1000 | *** | New Home Sales | |

| 25/08/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 25/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 25/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 25/08/2025 | 1915/1515 | Dallas Fed's Lorie Logan | ||

| 26/08/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 25/08/2025 | 2315/1915 | New York Fed's John Williams |