FED: New Monetary Policy Statement Ends Flexible Average Inflation Targeting

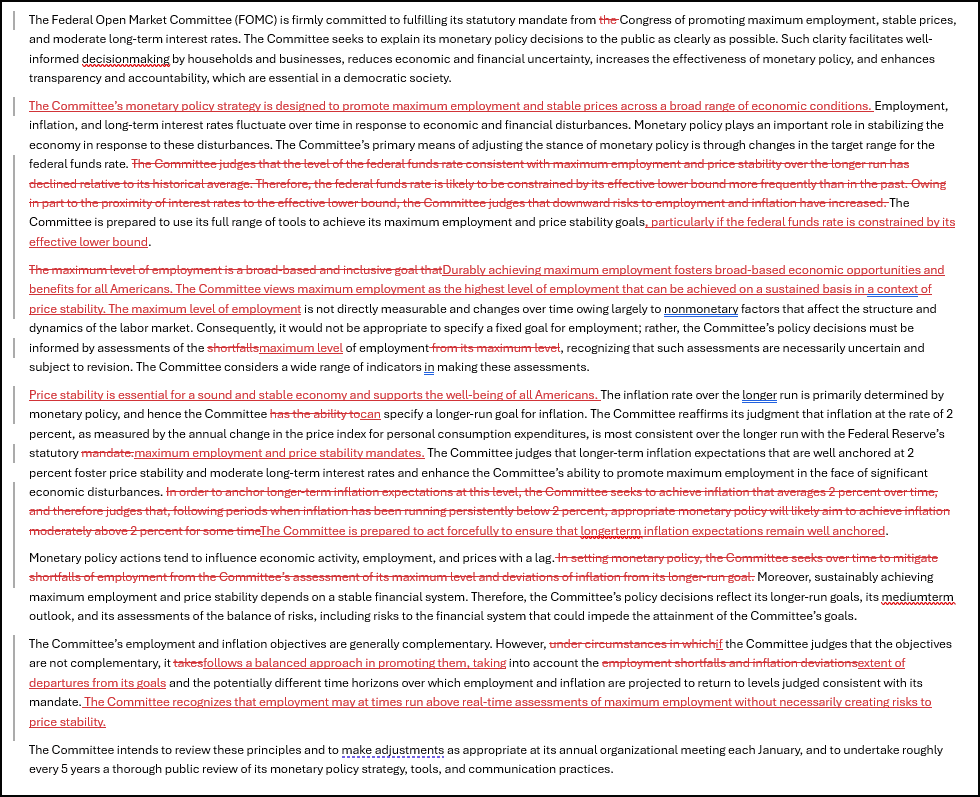

Also in Fed Chair Powell's speech (link) is a discussion of the changes to the Federal Reserve's Statement on Longer-Run Goals and Monetary Policy Strategy as part of the latest framework review (the last was in 2020, when the economic landscape looked very different). There don't appear to be any major surprises, as the review's conclusions have been well-telegraphed - below are Powell's explanation of all of the major changes, and the reasoning behind them. Below, we include a graphic comparing the new to the previous Statement on Longer-Run Goals and Monetary Policy Strategy (the new statement is available here).

- "First, we removed language indicating that the [effective lower bound of interest rates] was a defining feature of the economic landscape. Instead, we noted that our "monetary policy strategy is designed to promote maximum employment and stable prices across a broad range of economic conditions." The difficulty of operating near the ELB remains a potential concern, but it is not our primary focus. The revised statement reiterates that the Committee is prepared to use its full range of tools to achieve its maximum-employment and price-stability goals, particularly if the federal funds rate is constrained by the ELB."

- "Second, we returned to a framework of flexible inflation targeting and eliminated the "makeup" strategy. As it turned out, the idea of an intentional, moderate inflation overshoot had proved irrelevant. There was nothing intentional or moderate about the inflation that arrived a few months after we announced our 2020 changes to the consensus statement, as I acknowledged publicly in 2021." [Re the previous "FAIT" framework, Powell says: in 2020 "we adopted flexible average inflation targeting—a "makeup" strategy to ensure that inflation expectations would remain well anchored even with the ELB constraint. In particular, we said that, following periods when inflation had been running persistently below 2 percent, appropriate monetary policy would likely aim to achieve inflation moderately above 2 percent for some time.""]

- "Third, our 2020 statement said that we would mitigate "shortfalls," rather than "deviations," from maximum employment...Instead, the revised document now states more precisely that "the Committee recognizes that employment may at times run above real-time assessments of maximum employment without necessarily creating risks to price stability." Of course, preemptive action would likely be warranted if tightness in the labor market or other factors pose risks to price stability."

- "Fourth, consistent with the removal of "shortfalls," we made changes to clarify our approach in periods when our employment and inflation objectives are not complementary. In those circumstances, we will follow a balanced approach in promoting them. The revised statement now more closely aligns with the original 2012 language. "

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Bunds Off Lows, Spreads To Bunds Still Tighter

Bunds have recovered from session lows, with deepening Eurozone growth risks surrounding EU countermeasures against U.S. tariffs and the potential for a further deterioration in trade relations explaining much of the move.

- A downtick in crude oil prices also aided the recovery.

- Bund futures closed the initial opening gap lower after bears were not able to force a test of the July 21 low (129.73) during this morning’s sell off.

- Yields little changed to 3bp higher across the curve, with the lingering impact from JGB price action and a rally in equities felt on the slope of the curve.

- EGB spreads to Bunds hold tighter despite the recovery in German paper, aided by equities rallying, albeit with the latter trading off best levels of the day.

- German swap spreads and ASWs are a touch tighter, once again probably driven by associated readthrough for ECB policy from trade-related growth fears and the risk-on feel to wider price action.

OPTIONS: Expiries for Jul24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E1.6bln), $1.1500-10(E1.4bln), $1.1550(E908mln), $1.1620-30(E4.3bln), $1.1645-60(E2.2bln), $1.1700(E2.0bln), $1.1750-60(E1.7bln), $1.1800(E985mln)

- USD/JPY: Y146.00-05($570mln), Y147.00-10($1.1bln), Y147.50($1.6bln)

- AUD/USD: $0.6600(A$886mln), $0.6625-30(A$596mln)

- USD/CAD: C$1.3785($617mln)

MNI: US EIA: CRUDE OIL STOCKS EX SPR -3.17M TO 419.0M JUL 18 WK

- US EIA: CRUDE OIL STOCKS EX SPR -3.17M TO 419.0M JUL 18 WK

- US EIA: DISTILLATE STOCKS +2.93M TO 109.9M IN JUL 18 WK

- US EIA: GASOLINE STOCKS -1.74M TO 231.1M IN JUL 18 WK

- US EIA: CUSHING STOCKS +0.46M TO 21.9M BARRELS IN JUL 18 WK

- US EIA: SPR -0.2M TO 402.5M BARRELS IN JUL 18 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +1.6% TO 95.5% IN JUL 18 WK