MNI ASIA OPEN: Gov Miran - The Lone Dissenter

EXECUTIVE SUMMARY

- MNI: Fed Cuts 25BPS, Sees 2 More '25 Cuts; Miran Dissents

- MNI: Fed's Powell: No Widespread Support For 50BP Cut

- MNI FED: Powell Says Fed Doesn't Take Anchored LT Inflation Expectations For Granted

- MNI IMF: NY Post-Bessent Chief Of Staff Set To Become Seniormost US Off. At IMF

- MNI US DATA: Housing Activity Resumes Downtrend After Nascent Summer Pickup

US/CANADA

MNI: Fed Cuts 25BPS, Sees 2 More '25 Cuts; Miran Dissents

The Federal Reserve lowered official borrowing costs by a quarter point Wednesday, the first interest rate cut since December, and indicated two more cuts are expected this year, with newly-appointed governor Stephen Miran dissenting in favor of a larger 50 basis point reduction. The FOMC lowered its federal funds rate to a target range of 4-4.25%, citing downside risks to the labor market, and penciled in two additional reductions for 2025 and one more next year in its latest Summary of Economic Projections.

MNI: Fed's Powell: No Widespread Support For 50BP Cut

Federal Reserve Chair Jerome Powell said Wednesday there was not broad support for a larger interest rate cut despite a dissent from newly appointed governor Stephen Miran. "There wasn't widespread support at all for a 50 basis point cut today," Powell told reporters in his post-meeting press conference. The Fed cut rates by 25 basis points and officials penciled in a median of two more cuts for the year.

MNI FED: Powell Says Fed Doesn't Take Anchored LT Inflation Expectations For Granted

MNI's Jean Yung concludes the press conference, asking Powell about how he views inflation expectations, and whether fiscal deficits and the debate over Fed independence are boosting those expectations. Powell says: "Shorter term inflation expectations have tended to respond to near term inflation. So if inflation goes up, inflation expectations will predict that it takes just a little while to get back down. Fortunately, throughout this, this period, longer term inflation expectations, both breakevens in the markets and almost all of the longer term surveys, Michigan being a bit of an outlier lately, have been just rock solid in terms of running at levels that are consistent with 2% inflation over time. So we don't take that for granted. We actually assume that our actions have a real effect on that, and that we need to continually show and also mention our commitment to 2% inflation. And so you'll hear us doing that."

MNI BOC: Still "Proceeding Carefully"

The statements accompanying the BOC's 25bp rate cut (to an overnight rate of 2.50%) show increasing concerns about growth and the labor market, with inflation is seen as a lesser concern. In short, the BOC says, since July's meeting there is evidence of "a weaker economy and less upside risk to inflation", compared at that time when there was still "some resilience" in the economy, with "ongoing pressures on underlying inflation". This shift of course mirrors the developments in the data since the July meeting on all fronts.

NEWS

MNI IMF: NY Post-Bessent Chief Of Staff Set To Become Seniormost US Off. At IMF

The New York Post reports that, according to its sources, US Treasury Secretary Scott Bessent's chief of staff, Dan Katz, is set to leave the administration to take up the post of first deputy managing director of the International Monetary Fund (IMF). Speaking on the sidelines of the IMF and World Bank spring meetings in Washington, D.C., earlier this year, Bessent criticised both organisations, claiming that “mission creep has knocked these institutions off course".

MNI US: Air Defences Included In First Ukraine Military Aid Package Of Trump Admin

Ukrainian President Volodymyr Zelenskyy confirmed to reporters that Kyiv will receive air defence missiles for NASAMS and Patriot systems in the first US military aid package facilitated by the 'PURL' mechanism.

US TSYS

MNI US TSYS: Markets Whipsaw after Fed Delivers 25Bp Cut

- US Treasuries look to finish near late session lows, completely reversing the initial rate cut move rally - to weaker across the board after the bell with Dec'25 10Y futures just through early session low of 113-08 t0 113-02 (-15.5), 10Y yield +.0439 4.0718%.

- Treasury futures had extended highs after the FOMC annc 25bp rate cut, Fed Gov Miran the sole dissenter in favor of a 50bp cut. Tsy Dec'25 10Y futures climbing +8 to 113-25.

- Still digesting mixed messaging, Chairman Powell: "it's not a bad economy ... it's challenging to know what what to do ... there are no risk free paths. Now it's not incredibly obvious what to do."

- Meanwhile "downside risks to employment have risen," the Fed said in its post-meeting policy statement. "Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated."

- However, a confident sounding Chair Powell on the US economy as a whole and the mixed messages within the summary of economic projections questioned the overall dovish narrative and subsequently the US dollar aggressively reversed higher alongside US treasury yields.

- Focus turns to Thursday's weekly claims Leading Index and Net TIC Flows.

OVERNIGHT DATA

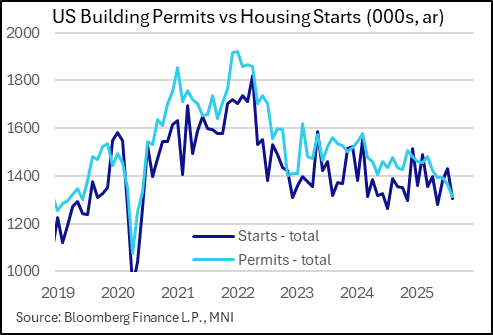

MNI US DATA: Housing Activity Resumes Downtrend After Nascent Summer Pickup

Residential construction activity fared worse in August than expected, with building permits hitting fresh cycle lows after a brief uptick was seen in June and July. Permits came in at 1,312k (SA annualized), a drop of 50k from prior and well below the 1,370k consensus. This marks a new cycle low for this key leading indicator of construction activity, with the prior low set at the start of the pandemic in 2020 and before that, June 2019. Permits have only risen % M/M in 2 of the last 12 months, and are now down 11.1% Y/Y.

MNI US DATA: Redbook Retail Sales Data Maintain Robustness Through Mid-September

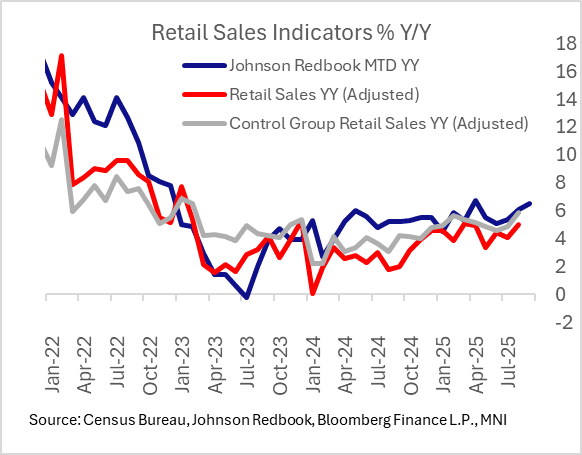

Lost somewhat in the fray after Tuesday's stronger than expected Census Bureau retail sales report: the Johnson Redbook Retail Sales Index release showed a 6.3% Y/Y rise in the week ending September 13. That follows a 6.6% rise the prior week and brought the month-to-date gain to 6.5%, a little above retailers' targeted 6.3%.

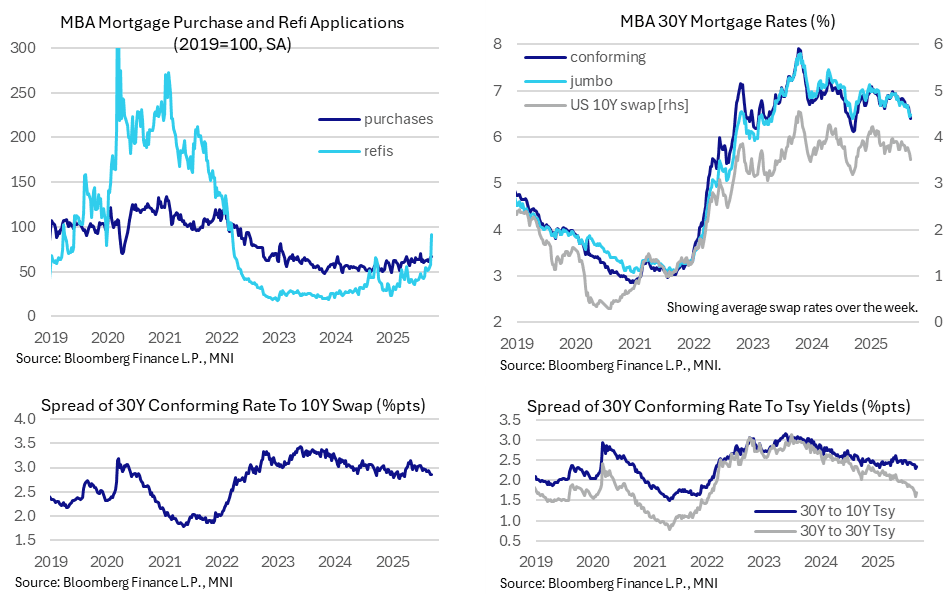

MNI US DATA: Mortgage Refinancing Surges On Lower Rates

MBA mortgage applications jumped last week as refis surged in response to a further decline in mortgage rates, building strongly on what had been signs of traction to lower rates in the week beforehand. It leaves the composite level of applications at their highest since April 2022. MBA composite mortgage applications jumped 29.7% (sa) last week to build on a solid 9.2% increase the week before that.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 260.42 points (0.57%) at 46018.32

S&P E-Mini Future down 4.5 points (-0.07%) at 6663

Nasdaq down 72.6 points (-0.3%) at 22261.33

US 10-Yr yield is up 4.6 bps at 4.0737%

US Dec 10-Yr futures are down 13.5/32 at 113-4

EURUSD down 0.0054 (-0.46%) at 1.1813

USDJPY up 0.48 (0.33%) at 146.96

WTI Crude Oil (front-month) down $0.51 (-0.79%) at $64.02

Gold is down $31.07 (-0.84%) at $3659.35

European bourses closing levels:

EuroStoxx 50 down 2.61 points (-0.05%) at 5369.7

FTSE 100 up 12.71 points (0.14%) at 9208.37

French CAC 40 down 31.24 points (-0.4%) at 7786.98

US TREASURY FUTURES CLOSE

3M10Y +4.884, 10.089 (L: 1.54 / H: 11.19)

2Y10Y +0.011, 52.269 (L: 47.907 / H: 53.903)

2Y30Y -2.26, 112.069 (L: 109.259 / H: 115.255)

5Y30Y -3.592, 102.62 (L: 101.717 / H: 106.656)

Current futures levels:

Dec 2-Yr futures down 2.625/32 at 104-11.875 (L: 104-11.625 / H: 104-17)

Dec 5-Yr futures down 9.25/32 at 109-19 (L: 109-18 / H: 110-01.25)

Dec 10-Yr futures down 13.5/32 at 113-4 (L: 113-02 / H: 113-25.5)

Dec 30-Yr futures down 17/32 at 117-14 (L: 117-10 / H: 118-21)

Dec Ultra futures down 18/32 at 121-9 (L: 121-02 / H: 122-21)

MNI US 10YR FUTURE TECHS: (Z5) Bull Mode

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-10 1.0% 10-dma envelope / High Apr 7 (cont.)

- RES 2: 114-00 Round number resistance

- RES 1: 113-29 High Sep 5

- PRICE: 113-19 @ 11:06 BST Sep 17

- SUP 1: 112-28 20-day EMA

- SUP 2: 112-05+ 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

A bull-mode condition in Treasury futures remains intact. Note that the recent impulsive rally signaled an acceleration of the uptrend. Also, moving average studies are in a bull-mode position, highlighting a dominant uptrend. This suggests scope for an extension through 114-00 next and a test of 114-10, the Apr 7 high (cont). Initial firm support to watch is 112-28, the 20-day EMA.

SOFR FUTURES CLOSE

Current White pack (Dec 25-Sep 26):

Dec 25 +0.005 at 96.365

Mar 26 -0.015 at 96.60

Jun 26 -0.045 at 96.830

Sep 26 -0.060 at 96.975

Red Pack (Dec 26-Sep 27) -0.09 to -0.075

Green Pack (Dec 27-Sep 28) -0.095 to -0.09

Blue Pack (Dec 28-Sep 29) -0.09 to -0.08

Gold Pack (Dec 29-Sep 30) -0.08 to -0.07

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.12), volume: $2.857T

- Broad General Collateral Rate (BGCR): 4.36% (-0.14), volume: $1.139T

- Tri-Party General Collateral Rate (TCR): 4.36% (-0.14), volume: $1.115T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $98B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $191B

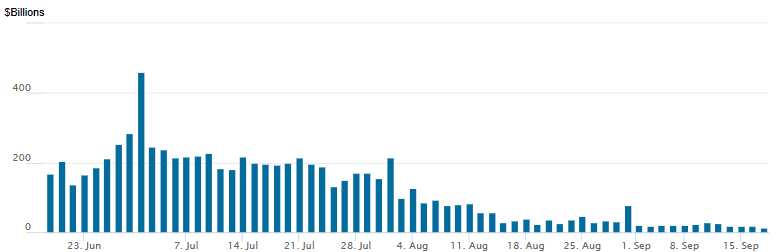

FED Reverse Repo Operation

RRP usage retreats to new lowest levels since early April 2021 this afternoon: $13.963B with 14 counterparties vs. $18.817B Tuesday. Today's drop compares to $16.954B on Monday. This year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

MNI PIPELINE: Corporate Bond Roundup: $37.25B Debt Issued Mon-Tue

No new issuance today, sidelined ahead of this afternoon's FOMC policy annc. $20.25B Priced Tuesday.

- Date $MM Issuer (Priced *, Launch #)

- 09/16 $8B *Mexico $1.5B +5Y +123, $4B +7Y +165, $2.5B 10Y +165

- 09/16 $2B *Phillips 66 $1B each: 30.5NC5.25 5.875%, 30.5NC10.25 6.2%

- 09/16 $1.75B *World Bank 7Y SOFR+50

- 09/16 $1.6B Directv 8.875% 2030 Tap

- 09/16 $1.5B *ZF N America 5.5NC 7.5%

- 09/16 $1.1B *Southern Power $550M each: 5Y +70, 10Y +90

- 09/16 $1B Solstice Advanced Materials 8NC3 5.625%

- 09/16 $800M *Carlyle 10Y +105

- 09/16 $700M Lucky Strike 7NC3 7%a

- 09/16 $750M Chord Energy 5NC2 6%

- 09/16 $550M *Transurban 10.5Y +90

- 09/16 $500M *Melco Res 8NC3 6.875%

MNI FOREX: Sharp Reversal Higher for US Dollar After DXY Prints Cycle Lows

- The initial reaction to the Fed’s 25bp rate cut and dovish adjustments to the statement was a sharp selloff for the US dollar. This marked a continuation of the recent theme of greenback weakness and prompted the USD index to briefly break to the lowest point since February 2022. Most notably, this propelled EURUSD to a high of 1.1919.

- However, a confident sounding Chair Powell on the US economy as a whole and the mixed messages within the summary of economic projections questioned the overall dovish narrative and subsequently the US dollar aggressively reversed higher alongside US treasury yields.

- The USD index rallied around 0.8%, with the likes of EURUSD and USDJPY reversing nearer to 1%.

- For USDJPY in particular, the false break below the bear trigger of 146.21 places a significant focus on today’s daily close and whether bearish momentum can be sustained for the pair. Markets will be aware of the risks surrounding the LDP leadership and Friday’s BOJ meeting.

- EURUSD rose to a high of 1.1919, within four pips of the 2.00 proj of the Feb 28 - Mar 18 - 247 price swing. Separately, GBPUSD traded as high as 1.3726 before trading back to 1.3650 as we approach the APAC crossover and tomorrow’s BOE meeting. Cycle highs for cable reside at 1.3789, the July 1 and key resistance.

- New Zealand GDP and Australian employment data kick off the Thursday calendar, before the focus turns to Norges bank and BOE decisions.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/09/2025 | 0710/0910 | ECB Lagarde Video Message at Women Leadership Summit | ||

| 18/09/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 18/09/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/09/2025 | 0800/1000 | ECB de Guindos at MNI Connect Event | ||

| 18/09/2025 | 0900/1100 | ** | EZ Construction Output | |

| 18/09/2025 | 0945/1145 | ECB Schnabel Chairs Panel at ECB Research Conference | ||

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS | |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |