US: Air Defences Included In First Ukraine Military Aid Package Of Trump Admin

Ukrainian President Volodymyr Zelenskyy confirmed to reporters that Kyiv will receive air defence missiles for NASAMS and Patriot systems in the first US military aid package facilitated by the 'PURL' mechanism.

- Reuters reported yesterday that Undersecretary of Defense for Policy at the Pentagon, Elbridge Colby, “has approved as many as two $500 million shipments under the new mechanism called the Prioritized Ukraine Requirements List, known under the acronym PURL.” In total, PURL is expected to deliver roughly USD$10 billion in US weapons to Ukraine, funded by NATO partners in Europe via PURL.

- The Kyiv Independent notes, “Since taking office in 2025, U.S. President Donald Trump's administration has sold weapons to Ukraine or shipped deliveries authorized under former U.S. President Joe Biden. The new mechanism marks the first aid packages initiated during Trump's second term.”

- UK Prime Minister Sir Keir Starmer is expected to advance Europe’s case for stepping up pressure on Russia at a bilateral meeting with Trump at the Prime Minister’s Chequers residence tomorrow.

- Politico cautions against expecting any major breakthroughs but reports the two could strike an agreement on “lowering the price cap set on Russian oil, which the EU and U.K. have lowered while the US has not,” and Trump could “join European sanctions on individual Russian ships.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Selloff Persists, Futures Narrow Gap To Support

Today’s selloff in Gilt futures is persisting, now -46 ticks at 90.64 and narrowing the gap to support at 90.59 (May 29 low). The latest Guardian story on stamp duty (see above) appears to have added some fresh pressure. Although details are vague and no final decisions have been made, it is another example of the difficult fiscal backdrop facing the Chancellor ahead of the Autumn budget.

- Gilt yields have registered fresh sessions highs across the curve, currently 3.5-4.5bps higher.

- 30-year nominal yields are testing the 5.60% handle for the first time since May. Meanwhile, linker yields are currently +4bps at 2.541%, the highest since 1998 according to Bloomberg Finance L.P data.

- 5s30s is just shy of Friday’s 148bp high (currently at 147.5bps), but is still at its steepest since 2017.

- UK CPI headlines this week’s regional calendar on Wednesday. MNI’s preview will be released tomorrow morning.

US TSY FUTURES: September'25-December'25 Roll Update

The latest Tsy quarterly futures roll volumes from September'25 to December'25 below. Percentage complete is running 5% or lower across the curve ahead the "First Notice" date on August 29. Current roll details:

- TUU5/TUZ5 appr 41,800 from -8.75 to -7.75, -8.0 last; 2%

- FVU5/FVZ5 appr 64,500 from -4.75 to -4.25, -4.5 last; 4%

- TYU5/TYZ5 appr 129,000 from -0.25 to +0.25, +0.0 last; 5%

- UXYU5/UXYZ5 appr 13,300 from 0.25 to 1.25, 1 last; 1%

- USU5/USZ5 appr 3,600 from 12.75 to 13.5, 13 last; 2%

- WNU5/WNZ5 appr 1,000 from 8.0 to 8.5, 8.25 last; 1%

- Reminder, Sep futures won't expire until next month: 10s, 30s and Ultras on September 22, 2s and 5s on September 30. Meanwhile, Sep'25 Tsy options will expire this Friday, August 22.

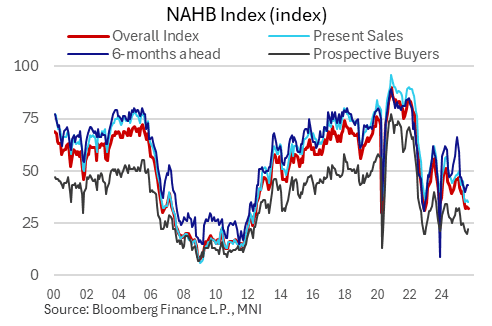

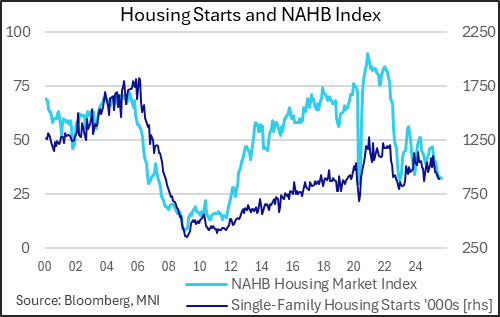

US DATA: Homebuilder Sentiment Still Historically Weak, Boding Ill For Activity

August's NAHB/Wells Fargo Housing Market report showed little improvement in the homebuilding sector, with present sales weakening modestly and selling prospects steady/moderately better.

- The headline index fell 1 point to 32 - reverting back to June's level which is around post-2022 lows, and dashing consensus expectations for a slight improvement to 34. Likewise, present sales reverted 1 point to June levels (35).

- Future sales remained at 43 for a second month, though in a bright spot, there was the biggest improvement in prospective buyer traffic since November 2024, up 2 points to 22 (but still below May's level).

- The standout move under the surface is a sharp drop in activity in the Northeast (the other 3 US regions were steady/slightly higher), dropping 9 points to a 31-month low 39.

- Per the report, weak demand conditions continue to have an impact on prices and incentives: "37% of builders reported cutting prices in August down from 38% in July. This share has remained at 37% or 38% for the past three months. Meanwhile, the average price reduction was 5% in August, the same as it’s been every month since last November. The use of sales incentives was 66% in August, up from 62% in July and the highest percentage in the post-Covid period."

- Overall, conditions for homebuilders remain historically weak amid extreme unaffordability for buyers (albeit potentially relieved somewhat by a moderation in mortgage rates in recent weeks). Weak NAHB sentiment signals continued weakness in residential sector activity, with single home starts likely to remain under downside pressure.