MNI ASIA MARKETS ANALYSIS: Tsys Follow Bund Lead Off Early Low

HIGHLIGHTS

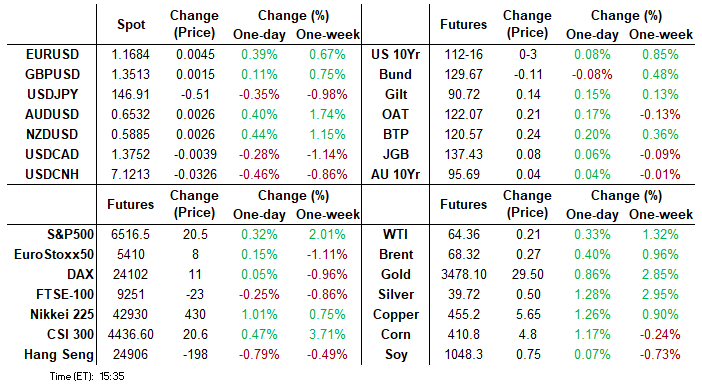

- Treasuries ratcheted off early lows, looking to finish near second half highs Thursday, curves twisting flatter with the short end holding weaker (2s10s -4.974 at 57.195).

- USD retreated Thursday, putting the USD Index into negative territory - although remaining anchored by the 50-dma of 98.061 throughout.

- WTI crude has rallied in recent trade and is now higher on the day as the market awaits an expected Trump announcement on Russia/Ukraine later.

US TSYS

US TSYS: Tsys Finishing Near Highs, Curves Reverse Midweek Steepening

- Off early lows, Treasuries look to finish mostly higher & near the top end of the session range Thursday, following similar bounce in Bunds - curves twisting flatter with the short end resisting the move: 2s10s -5.179 at 56.990, 5s30s -4.728 at 117.528.

- Treasury futures had extend lows after lower than expected continuing jobless claims data, prior down-revised as well, weekly claims decline largely in-line with expectations. Initial jobless claims were essentially as expected at 229k (sa, cons 230k). Continuing claims meanwhile surprised lower at 1954k (cons 1966k) in the week to Aug 16, covering a payrolls reference period.

- Second read of core PCE in-line while GDP annualized figure rises higher than anticipated. Real GDP revised to 3.29% annualized (cons 3.1) from 2.97% in the advance Q2 release, after -0.5% in Q1. Real personal consumption revised to 1.57% annualized (cons 1.6) from 1.44% in the advance Q2 release, after 0.5% in Q1.

- Meanwhile, the National Association of Realtors' index of pending home sales fell to 71.4 in July from 72.0 prior, a 3-month low and a little worse than expected (-0.4% M/M vs -0.2% expected, -0.8% prior).

- Treasuries recovered quickly after the $44B 7Y note auction (91282CNW7) tailed: 3.925% high yield vs. WI of 3.920%; bid-to-cover 2.49x from 2.79x prior.

- Note, WTI crude has rallied in recent trade and is now higher on the day as the market awaits an expected Trump announcement on Russia/Ukraine later.

- Looking ahead to Friday's Data Calendar: Personal Income/Spending, Core PCE, Chi PMI and U of Mich Sentiment/inflation expectations.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.36% (-0.02), volume: $2.889T

- Broad General Collateral Rate (BGCR): 4.35% (-0.02), volume: $1.162T

- Tri-Party General Collateral Rate (TCR): 4.35% (-0.02), volume: $1.120T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $114B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $229B

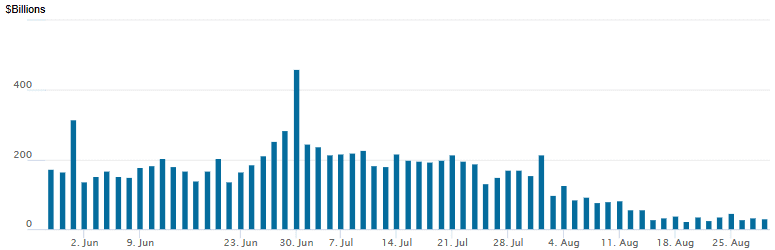

FED Reverse Repo Operation

RRP usage slips to $31.966B with 20 counterparties this afternoon, from $34.744B yesterday. Compares to $22.344B on Tuesday, Aug 19 - lowest since April 5, 2021 vs. this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options remained largely mixed Thursday, two-way directional and vol flows. Underlying Tsy futures off with curves twisting flatter (2s10s -5.156 at 57.013) unwinding a portion of Wednesday's steepening. Projected rate cuts near late Wednesday (*) levels: Sep'25 at -21.2bp (-21.6bp), Oct'25 at -34.6bp (-34.6bp), Dec'25 at -54.8bp (-55.6bp), Jan'26 at -67.1bp (-69.1bp).

SOFR Options:

Block, 5,000 SFRU5 96.00/96.12/96.18 broken call flys, 0.75 net

-10,000 0QZ5 97.00/97.50/98.00 call flys, 10.0

+5,000 0QZ5 96.25/98.12 strangles, 2.5

+2,000 SFRV5 96.18/96.25 strangles, 16.5 ref 96.215

-8,000 SFRU5 95.81/96.18 put over risk reversals, 1.25

+5,000 0QU5 96.50/96.75 put spds, 2.0 vs. 96.905/0.05%

+2,000 SFRU6 97.00/97.12/97.25 call flys, 1.0

2,000 SFRZ5 95.87/96.00 put spds ref 96.23

2,000 SFRZ5 96.56/96.68 call spds ref 96.235

2,000 SFRX5 96.37/96.87 call spds, 6.0 ref 96.235

+4,000 SFRZ5 96.37 calls, 9.5 ref 96.235/0.24%

-3,900 0QH6 96.75/97.25 put spds, 25 ref 97.065/0.25%

1,000 SFRZ5 96.25/96.31/96.44/96.50 call condors ref 96.235

Treasury Options:

-10,000 TYX5 111.5/113 strangles, 110

+1,500 wk5 FV 109.25/109.5 call over risk reversals, 4.0 vs. 109-14.75/0.64%

over 7,800 wk5 TY 112.75 calls ref 112-17.5

-3,000 TYV5 113/113.75 1x2 call spds, 3.0 ref 112-17.5

-1,250 TYX5 113 calls, 44

+29,400 FVV5 110 calls, 16.5-18 ref 109-16.5 to -14.5

+4,000 wk1 TU 104.37/104.75 1x2 call spds, 3.5

+2,000 wk5 TY 112.25 puts, 5

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform Ahead Of Inflation Data

Gilts easily outperformed Bunds Thursday, with periphery/semi-core EGBs regaining ground after a poor start to the week.

- Bunds and Gilts gained in overnight trade, catching up to a Treasury rally late Wednesday, but turned lower in the European morning.

- There were no major data/headline triggers for the reversal, but EGBs appeared to track equity moves fairly closely, with a top in Bund yields and move back lower coinciding with the mirror-image move in Eurostoxx.

- The converse was true for periphery/semi-core EGBs, with OAT spreads nearing the session's widest levels in the early afternoon. However, spreads opened the session tighter (in a slight recovery move after Wednesday saw a post-January wide in 10Y OAT/Bund spread) and closed the day narrower.

- The accounts of the July 23-24 ECB meeting noted that "a view" was expressed about cutting rates but that keeping rates unchanged was deemed a "robust approach".

- In data, Belgium HICP inflation held steady in August, while Eurozone bank lending to households and non-financial corporations continued to steadily accelerate in July. Eurozone and Italian confidence indicators failed to move the needle.

- The German curve twist flattened, with the UK's bull flattening.

- Friday's scheduled highlight is flash August inflation data for Spain, France, Italy, and Germany. MNI's preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.9bps at 1.934%, 5-Yr is up 0.6bps at 2.243%, 10-Yr is down 0.5bps at 2.695%, and 30-Yr is down 0.9bps at 3.298%.

- UK: The 2-Yr yield is down 2.8bps at 3.936%, 5-Yr is down 3.6bps at 4.097%, 10-Yr is down 3.7bps at 4.699%, and 30-Yr is down 3bps at 5.57%.

- Italian BTP spread down 3.1bps at 84.2bps / French OAT down 3.8bps at 78.6bps

MNI OPTIONS: Euribor Upside Plays And Sonia Call Condor Trades Continue

Thursday's Europe rates/bond options flow included:

- OEV5 118.20/119.25cs vs 117.50p, bought the cs for 6 in 1k

- OEV5 117.25/117.00ps, bought for 3 in 4k

- ERZ5 98.125/98.1875/98.25c fly, bought for 0.75 in 2k

- ERZ5 98.0625/98.1875/98.3125c fly, bought for 2.25 in 2k

- ERH6 99.00/99.50cs, bought for half in 10k

- SFIZ5 96.25/96.35/96.45/96.55c condor vs 96.05p, bought the condor for 0.25 in 5k

- SFIZ6 97.25/97.75 call spread paper paid 4.5 on 5K

MNI FOREX: USD Index Lower, But Remains Anchored by 50-dma

- Having started Thursday trade on a more stable footing, the USD faded Thursday, putting the USD Index into negative territory - although remaining anchored by the 50-dma of 98.061 throughout. Further Fed independence questions follow the counter-suing of President Trump from Fed's Cook - leaving a notable question mark over the make-up of the FOMC later this year.

- Meanwhile, a renewed phase of USD sales pressured USD/CNH to new pullback - and year-to-date lows - of 7.1212. Much market focus remains on the PBOC fix overnight, which was marked higher (USD/CNY lower) relative to expectations - making for the strongest CNY fix since November of last year (down to 7.1063 from 7.1108).

- The stronger CNY fix provides more evidence that Chinese authorities are endorsing and pursuing strength in the currency in the context higher global trade tensions (Mexico are set to join the US in raising tariffs on Chinese imports) and as China's top trade negotiator Li Chenggang has travelled to Washington this week for talks with US officials. While no groundbreaking trade deal news is expected, it is a further sign of warmer relations, and may set up a Trump-Xi summit later this year.

- Datapoints pick up notably on Friday, with Japanese jobless data, prelim CPIs from France, Italy and Germany keeping markets busy ahead of the US open, with July PCE, trade balance, MNI Chicago PMI and UMich sentiment data set to follow.

- Fed's Waller is set to speak after the market close today - a leading contender for the next Fed Chair role and now one of the outright doves on the FOMC, there are two-sided risks to market reaction. Whilst there is a low bar to him surprising hawkishly vs prior comments (especially if he offers stronger pushback against recent independence challenges), it's worth noting that his dissenting statement warning on labor market stresses came just before the weak payrolls report. Kalshi betting has for a few weeks now had Waller as the lead contender for Fed Chair, with 30% chance.

MNI FX OPTIONS: Expiries for Aug29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-05(E4.1bln), $1.1600(E1.7bln), $1.1625(E4.1bln), $1.1650(E735mln), $1.1700(E1.1bln), $1.1725(E1.1bln), $1.1745(E1.1bln)

- GBP/USD: $1.3250(Gbp873mln)

- USD/JPY: Y145.00($1.7bln), Y146.50($1.1bln), Y147.50($807mln)

- USD/CAD: C$1.3830($676mln)

- EUR/GBP: Gbp0.8563-80(E2.1bln), Gbp0.8725(E1.1bln)

- AUD/USD: $0.6500-15(A$1.4bln), $0.6555-60(A$809mln)

MNI US STOCKS: Late Equities Background: SPX Eminis New High, Comm, Tech, Oil Lead

- Major US stock indexes are drifting higher - the tech heavy Nasdaq outperforming late Thursday. Currently, the DJIA trades up 37.1 points (0.08%) at 45602.26, S&P E-Minis Future up 21.7 points (0.33%) at 6517.75 record high, Nasdaq up 136.2 points (0.6%) at 21725.5.

- Communication Services and Information Technology sector shares continued to lead gainers in the second half, communication shares rebounding from midweek selling: Trade Desk +4.23%, Alphabet +2.05%, TKO Group Holdings +1.70% and Take-Two Interactive Software +0.95%.

- Tech stocks added to midweek gains with hardware & software shares outpacing semiconductor makers for once (Nvidia -0.39% despite announcing higher sales and strong demand after Wednesday's close): Datadog +7.07%, ServiceNow +4.92%, Crowdstrike Holdings +3.94% and Fair Isaac Corp +3.92%.

- Of note, oil and gas shares gained in late trade as crude prices bounced (WTI to 64.60 from 63.57) amid reports Trump will make a statement on Russia's latest bombardment of Ukraine: EQT Corp +2.08%, APA Corp +1.55%, Occidental Petroleum +1.27% and Diamondback Energy +1.25%.

- Conversely, Health Care sector shares underperformed for the second day running: following lower guidance and multiple downgrades - Cooper Cos dropped 10.26%, Bio-Techne Corp -4.40%, Moderna -3.65% and Biogen -2.60%.

- Meanwhile, Consumer Staples shares retreated: Hormel Foods -12.87% as cost pressures hamper profits, Brown-Forman -5.02%, Conagra Brands -2.58% and Tyson Foods -2.47%.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trend Needle Points North

- RES 4: 6600.00 Round number resistance

- RES 3: 6587.42 2.0% 10-dma envelope

- RES 2: 6523.63 1.764 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6517.75 intra-day & all-time High

- PRICE: 6516.00 @ 1455 ET Aug 28

- SUP 1: 6362.75 Low Aug 20

- SUP 2: 6318.96 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

S&P E-Minis bulls remain in the driver’s seat and the contract is holding on to its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment. Attention is on 6508.75, the Aug 15 high. Clearance of this hurdle would confirm a resumption of the uptrend and open 6523.63, a Fibonacci projection. Support to watch lies at 6318.96, the 50-day EMA.

MNI COMMODITIES: Crude Extends Gains, Gold At One-Month High

- WTI crude has rallied in recent trade and is now higher on the day as the market awaits an expected Trump announcement on Russia/Ukraine later.

- Markets are leaning towards a more bullish outcome for oil in the form of threatened secondary sanctions given the lack of progress regarding Putin/Zelenskyy peace talks.

- WTI Oct 25 is up by 0.8% at $64.7/bbl.

- From a technical perspective, a bear cycle in WTI futures remains intact and the latest round of short-term gains still appear corrective.

- Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

- Meanwhile, spot gold is up by 0.6% at $3,419/oz, taking the yellow metal to its highest level since July 23.

- The medium-term trend condition in gold remains bullish. Moving average studies are in a bull-mode position, highlighting a dominant uptrend.

- Today’s gains narrow the gap to resistance at $3,439.0, the Jul 23 high, which is followed by $3,451.3, the Jun 16 high. Key resistance and the bull trigger is at $3,500.1, the Apr 22 high.

- Elsewhere, copper has also rallied by 1.2% to $455/lb.

- Copper futures are in consolidation mode, with initial resistance at $486.88, the 50-day EMA. On the downside, a move lower would signal scope for a test of key support at $418.85, the Apr 7 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 29/08/2025 | 0600/0800 | *** | GDP | |

| 29/08/2025 | 0600/0800 | ** | Retail Sales | |

| 29/08/2025 | 0600/0800 | ** | Import/Export Prices | |

| 29/08/2025 | 0600/0800 | ** | Retail Sales | |

| 29/08/2025 | 0630/0730 | DMO to release FQ3 (Oct-Dec) issuance ops calendar | ||

| 29/08/2025 | 0645/0845 | *** | HICP (p) | |

| 29/08/2025 | 0645/0845 | ** | PPI | |

| 29/08/2025 | 0645/0845 | *** | GDP (f) | |

| 29/08/2025 | 0645/0845 | ** | Consumer Spending | |

| 29/08/2025 | 0700/0900 | *** | HICP (p) | |

| 29/08/2025 | 0755/0955 | ** | Unemployment | |

| 29/08/2025 | 0800/1000 | *** | GDP (f) | |

| 29/08/2025 | 0800/1000 | *** | Bavaria CPI | |

| 29/08/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 29/08/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 29/08/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/08/2025 | 0900/1100 | *** | HICP (p) | |

| 29/08/2025 | 0900/1100 | ECB de Guindos at Cursos Europeos de Verano | ||

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 29/08/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 29/08/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 29/08/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 29/08/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/08/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 29/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 29/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 29/08/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |