US STOCKS: Late Equities Background: SPX Eminis New High, Comm, Tech, Oil Lead

Aug-28 18:50

- Major US stock indexes are drifting higher - the tech heavy Nasdaq outperforming late Thursday. Currently, the DJIA trades up 37.1 points (0.08%) at 45602.26, S&P E-Minis Future up 21.7 points (0.33%) at 6517.75 record high, Nasdaq up 136.2 points (0.6%) at 21725.5.

- Communication Services and Information Technology sector shares continued to lead gainers in the second half, communication shares rebounding from midweek selling: Trade Desk +4.23%, Alphabet +2.05%, TKO Group Holdings +1.70% and Take-Two Interactive Software +0.95%.

- Tech stocks added to midweek gains with hardware & software shares outpacing semiconductor makers for once (Nvidia -0.39% despite announcing higher sales and strong demand after Wednesday's close): Datadog +7.07%, ServiceNow +4.92%, Crowdstrike Holdings +3.94% and Fair Isaac Corp +3.92%.

- Of note, oil and gas shares gained in late trade as crude prices bounced (WTI to 64.60 from 63.57) amid reports Trump will make a statement on Russia's latest bombardment of Ukraine: EQT Corp +2.08%, APA Corp +1.55%, Occidental Petroleum +1.27% and Diamondback Energy +1.25%.

- Conversely, Health Care sector shares underperformed for the second day running: following lower guidance and multiple downgrades - Cooper Cos dropped 10.26%, Bio-Techne Corp -4.40%, Moderna -3.65% and Biogen -2.60%.

- Meanwhile, Consumer Staples shares retreated: Hormel Foods -12.87% as cost pressures hamper profits, Brown-Forman -5.02%, Conagra Brands -2.58% and Tyson Foods -2.47%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Instant Answers For BOC Decision (4/4)

Jul-29 18:43

Following are the Instant Answers for the Bank of Canada decision due Wed at 945am EST:

- Overnight Rate Target (%)

- Does the Bank signal it's prepared to LOWER rates in the future?

- Does the Bank reiterate it could LOWER rates if the economy weakens amid tariffs and inflation is contained?

- Does the Bank signal it is prepared to RAISE rates in the future?

- Does the Bank signal it intends to leave rates ON HOLD?

BOC: Forecasts To Be Less Pessimistic, Uncertainty Precludes Firm Guidance(3/4)

Jul-29 18:38

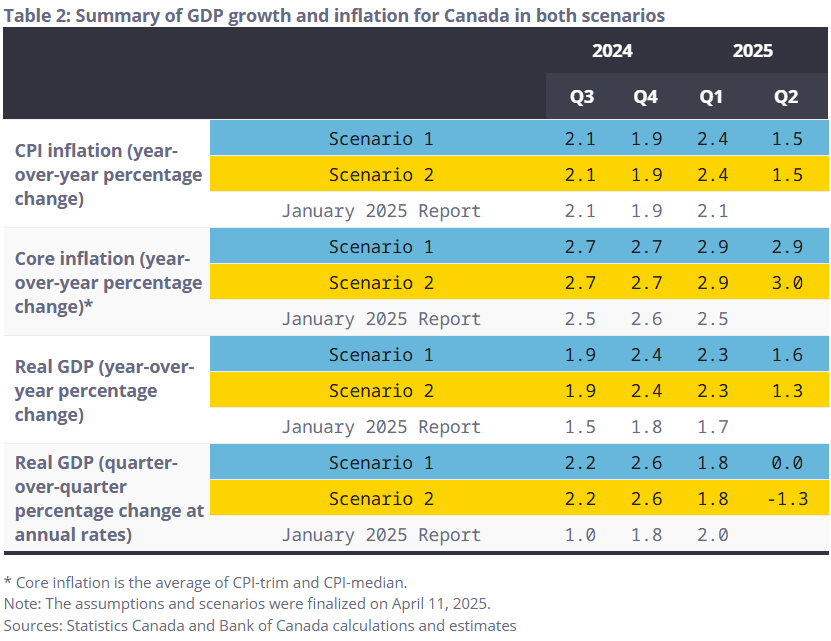

The prior Monetary Policy Report (April)'s summary table is below, showing two “scenarios”, one more pessimistic on the outlook than the other amid tariff threats. The BOC has signaled a preference to get back to a central forecast as opposed to dual scenarios, though it’s not likely that will happen in July.

- That’s because of multiple areas of uncertainty that could continue to warrant scenario-based analysis. First and foremost is US President Trump’s stated deadline of August 1 to reach a trade deal with Canada, absent which a 35% tariff rate on Canadian exports to the US has been threatened.

- We could add to such areas of uncertainty the federal government’s fall budget and various incoming data, but those are fairly ordinary areas of uncertainty and the US tariff situation is enough to keep the outlook extremely clouded.

- Given the above, we expect to see another dual-scenario outlook, albeit a more optimistic one than April’s on the activity front.

- As the aforementioned data since April suggests, this will include a less negative estimate for Q2 GDP with slightly higher core inflation. If they do publish a single, central forecast, this would be a surprise and suggest that the BOC has more confidence in its ability to make projections despite aforementioned uncertainties.

- The policy statement should reflect this better-than-expected economic activity evolution as well, suggesting as Gov Macklem has previously that reality has unfolded much closer to Scenario 1 than Scenario 2. There could be some note of continued elevation in core inflation metrics. In June the BOC noted "firmness in recent inflation data" which could stand, though "softer but not sharply weaker" economic activity could sound a little more positive this time.

- Once again, however, we do not expect any firm forward guidance given tariff uncertainty.

BOC: Data Calls For Further Patience (2/4)

Jul-29 18:35

Looking at recent inter-meeting data informing the likely rate hold Wednesday (more detail in our PDF preview):

- June's Labour Force Survey saw much-better-than-expected employment (+83.1k, vs 0.0k consensus) and unemployment rate (6.9%, vs 7.1% consensus) data. This was the biggest overall monthly job gain in 6 months.

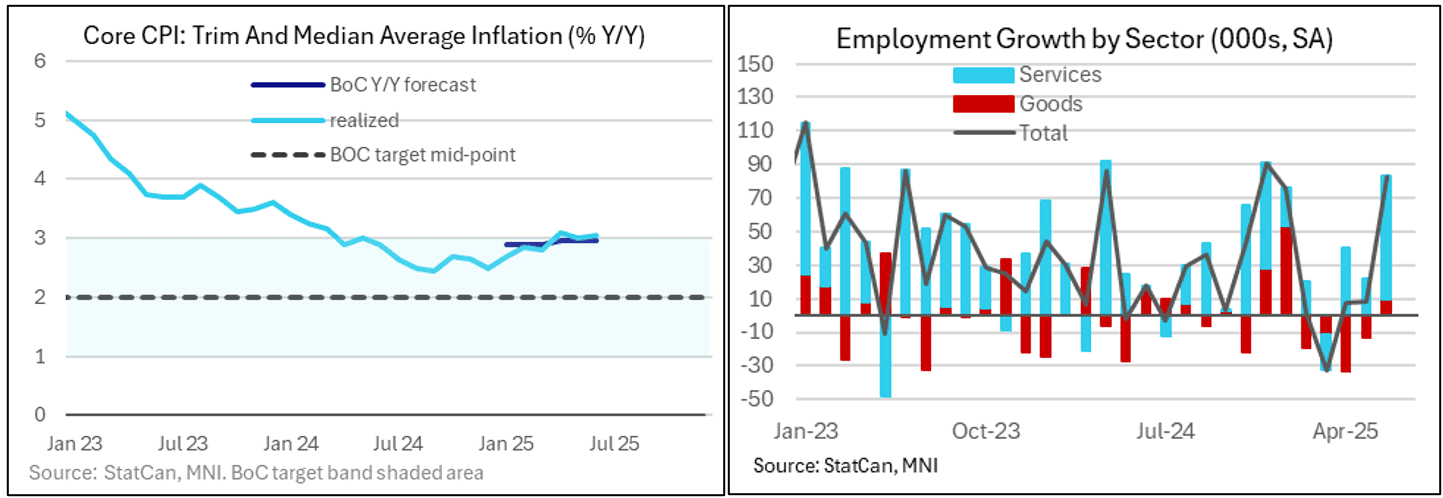

- June CPI report showed stronger-than-anticipated price pressures. The main takeaway was the slightly-higher-than-expected print for the BOC's preferred inflation metric: with the trim / median average finishing Q2 averaging 3.05%, higher than the 2.95% "forecast" by the BOC in its April projections (its two tariff scenarios were 2.9% or 3.0%). For the quarter, Y/Y trim averaged 3.03% and median 3.07%. June didn't see a major upside miss on the major core metrics, but when combined with the upside "miss" in headline CPI (a below-BOC target 1.8% Y/Y in Q2, but vs 1.5% in April's BOC projections), the apparent acceleration in inflation momentum is reason enough to stay on hold.

- The advance estimate for June's retail sales is for 1.6% M/M gains - which would be the fastest pace since December.

- The Bank of Canada's quarterly Business Outlook Survey (BOS) and Canadian Survey of Consumer Expectations (CSCE) showed broadly that the economy and inflation expectations stabilized between February (the Q1 survey) and May (the Q2 report released this month). Neither survey's findings are an obstacle for further BOC rate cuts, but nor do they make a compelling case for further easing.

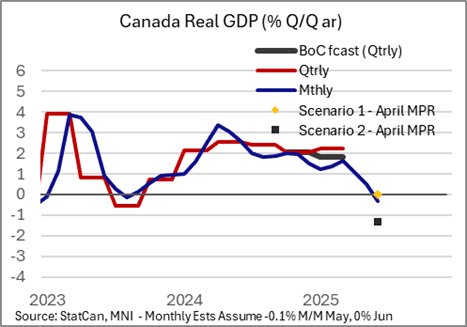

- The latest monthly GDP reading showed a below-consensus -0.1% M/M reading for April, with the May flash estimate also pointing to a 0.1% contraction (we get the data on July 31, the day after the BOC decision). That was indicative of quarterly growth of -0.3% in Q2, if June comes in flat (which looks like pessimistic assumption given other activity data for the month). This would be between the BOC's two scenario estimates of -1.3% and 0.0% in its April projections. This comes after the latest quarterly GDP release on May 30 showed Q1 annualized GDP +2.2%, above the BOC forecast for +1.8%