BONDS: EGBs-GILTS CASH CLOSE: Bunds Underperform Ahead Of Inflation Data

Gilts easily outperformed Bunds Thursday, with periphery/semi-core EGBs regaining ground after a poor start to the week.

- Bunds and Gilts gained in overnight trade, catching up to a Treasury rally late Wednesday, but turned lower in the European morning.

- There were no major data/headline triggers for the reversal, but EGBs appeared to track equity moves fairly closely, with a top in Bund yields and move back lower coinciding with the mirror-image move in Eurostoxx.

- The converse was true for periphery/semi-core EGBs, with OAT spreads nearing the session's widest levels in the early afternoon. However, spreads opened the session tighter (in a slight recovery move after Wednesday saw a post-January wide in 10Y OAT/Bund spread) and closed the day narrower.

- The accounts of the July 23-24 ECB meeting noted that "a view" was expressed about cutting rates but that keeping rates unchanged was deemed a "robust approach".

- In data, Belgium HICP inflation held steady in August, while Eurozone bank lending to households and non-financial corporations continued to steadily accelerate in July. Eurozone and Italian confidence indicators failed to move the needle.

- The German curve twist flattened, with the UK's bull flattening.

- Friday's scheduled highlight is flash August inflation data for Spain, France, Italy, and Germany. MNI's preview is here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.9bps at 1.934%, 5-Yr is up 0.6bps at 2.243%, 10-Yr is down 0.5bps at 2.695%, and 30-Yr is down 0.9bps at 3.298%.

- UK: The 2-Yr yield is down 2.8bps at 3.936%, 5-Yr is down 3.6bps at 4.097%, 10-Yr is down 3.7bps at 4.699%, and 30-Yr is down 3bps at 5.57%.

- Italian BTP spread down 3.1bps at 84.2bps / French OAT down 3.8bps at 78.6bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGBs-GILTS CASH CLOSE: Bunds Modestly Underperform Ahead Of HICP Data

Curve bellies underperformed Tuesday.

- Bund yields largely traded within Monday's ranges, with Gilt yields fading an early rise.

- Early core FI losses didn't appear to reflect any new news, instead continuing to trade on speculation regarding the weekend's EU-US trade pact (some details remain scarce despite the EU releasing a fact sheet).

- US Treasuries drove much of the afternoon's price action, with soft labour market data helping boost global core instruments before a modest sell-off going into the close.

- In data, UK consumer credit data and Spanish Q2 prelim GDP were stronger-than-expected, though had little market impact.

- The German curve lightly bear steepened, with the UK's leaning bull flatter - though the 5-7Y segments underperformed in both cases. Periphery/semi-core EGB spreads tightened modestly.

- Wednesday brings Eurozone Q2 GDP data, but focus will likely be more firmly placed on the first readings of flash July inflation starting with Spain (MNI's preview is here). Global attention will be on the Federal Reserve's decision (though after Wednesday's cash close).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.4bps at 1.942%, 5-Yr is up 2.6bps at 2.293%, 10-Yr is up 1.9bps at 2.708%, and 30-Yr is up 0.8bps at 3.204%.

- UK: The 2-Yr yield is down 1.2bps at 3.894%, 5-Yr is down 0.8bps at 4.067%, 10-Yr is down 1.4bps at 4.633%, and 30-Yr is down 1.3bps at 5.441%.

- Italian BTP spread down 0.7bps at 81bps / French OAT down 0.6bps at 65.6bps

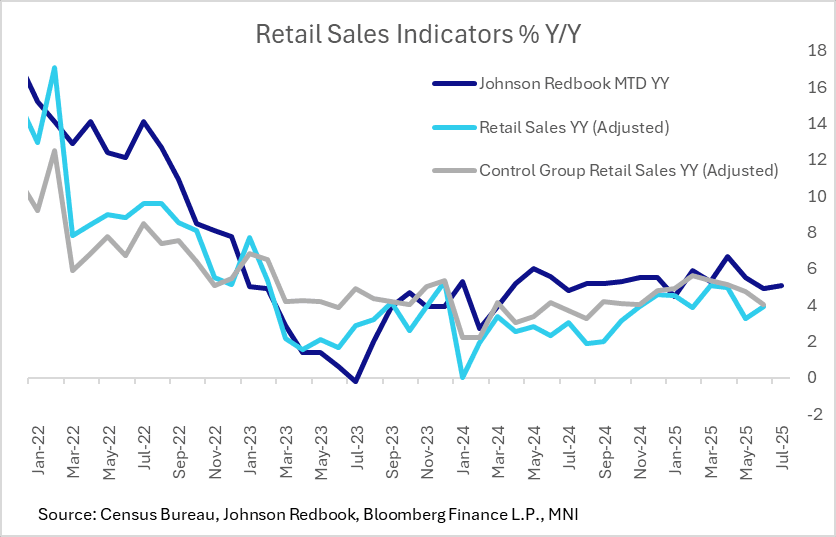

US DATA: Redbook Retail Sales Stay Solid, Weather And Tariff Inventories Noted

The Johnson Redbook Retail Sales Index continued to post 5.1% Y/Y month-to-date July sales growth after a 4.9% rise in the week ending July 26.

- While lower than retailers' targeted gain of 5.7%, this suggests that retail activity remains solid (the index captures 80% of Census Bureau retail sales).

- Census Bureau retail sales rose 3.9% Y/Y in June, with no consensus yet for the July data (out August 15).

- The anecdotal portion of the report notes potential weather-related factors weighing on demand, though it is interesting to hear that retailers are reporting they are getting through pre-tariff inventories: "retailers have continued to focus on clearing out summer inventories and introducing back-to-school merchandise, as they work through the stock they imported before tariffs took effect. Sales fell below expectations in the third week of July. Some retailers noted that the heat waves across much of the country deterred budget-conscious shoppers from visiting stores. Others reported sluggish business and unmotivated consumers, which seemed to indicate the usual mid-July slowdown. However, by mid-August, back-to-school demand is expected to revive all sectors."

EURGBP TECHS: Short-Term Reversal Threat

- RES 4: 0.8835 High May 3 2023

- RES 3: 0.8800 Round number resistance

- RES 2: 0.8781 2.236 pro of the Mar 3 - 11 - 28 price swing

- RES 1: 0.8769 High Jul 27 and the bull trigger

- PRICE: 0.8653 @ 18:11 BST Jul 29

- SUP 1: 0.8649/42 20- day EMA/Low Jul 29

- SUP 2: 0.8581 50-day EMA

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8508 Low Jun 27

EURGBP reversed sharply lower from Monday’s intraday high. For now, the trend set-up remains bullish, however, Monday’s price pattern - a bearish engulfing candle - does signal a potential short-term reversal. A continuation lower exposes support at the 20-day EMA, at 0.8649 - a level tested on Tuesday. Clearance of this average would signal scope for a deeper retracement. For bulls, a move through 0.8769, the Jul 27 high, would confirm a resumption of the uptrend.