COMMODITIES: Crude Extends Gains, Gold At One-Month High

- WTI crude has rallied in recent trade and is now higher on the day as the market awaits an expected Trump announcement on Russia/Ukraine later.

- Markets are leaning towards a more bullish outcome for oil in the form of threatened secondary sanctions given the lack of progress regarding Putin/Zelenskyy peace talks.

- WTI Oct 25 is up by 0.8% at $64.7/bbl.

- From a technical perspective, a bear cycle in WTI futures remains intact and the latest round of short-term gains still appear corrective.

- Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $66.56, the Aug 4 high.

- Meanwhile, spot gold is up by 0.6% at $3,419/oz, taking the yellow metal to its highest level since July 23.

- The medium-term trend condition in gold remains bullish. Moving average studies are in a bull-mode position, highlighting a dominant uptrend.

- Today’s gains narrow the gap to resistance at $3,439.0, the Jul 23 high, which is followed by $3,451.3, the Jun 16 high. Key resistance and the bull trigger is at $3,500.1, the Apr 22 high.

- Elsewhere, copper has also rallied by 1.2% to $455/lb.

- Copper futures are in consolidation mode, with initial resistance at $486.88, the 50-day EMA. On the downside, a move lower would signal scope for a test of key support at $418.85, the Apr 7 low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Forecasts To Be Less Pessimistic, Uncertainty Precludes Firm Guidance(3/4)

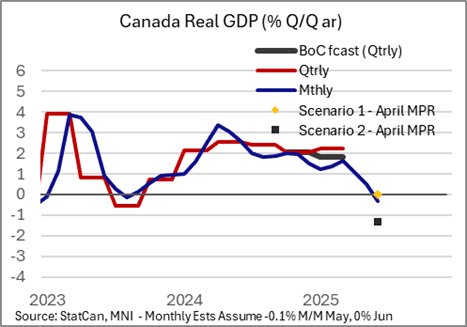

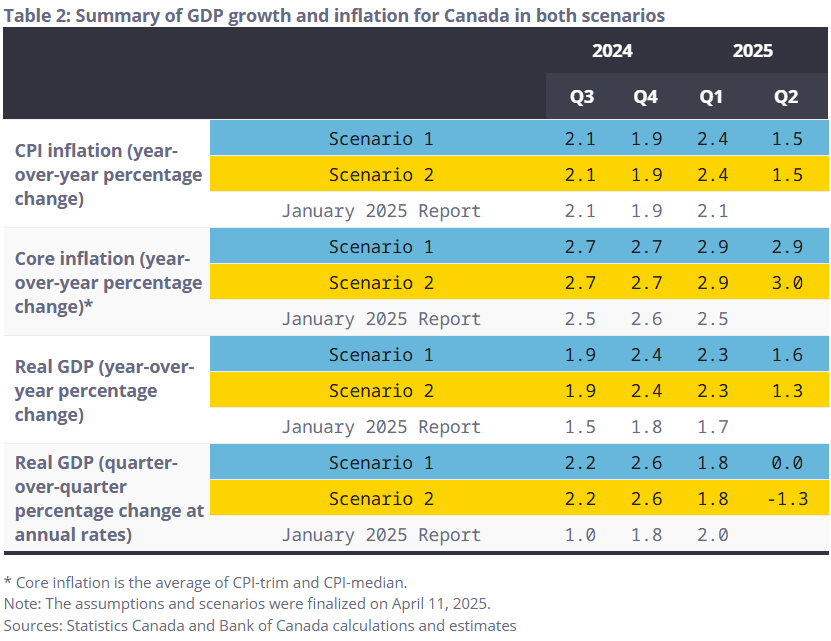

The prior Monetary Policy Report (April)'s summary table is below, showing two “scenarios”, one more pessimistic on the outlook than the other amid tariff threats. The BOC has signaled a preference to get back to a central forecast as opposed to dual scenarios, though it’s not likely that will happen in July.

- That’s because of multiple areas of uncertainty that could continue to warrant scenario-based analysis. First and foremost is US President Trump’s stated deadline of August 1 to reach a trade deal with Canada, absent which a 35% tariff rate on Canadian exports to the US has been threatened.

- We could add to such areas of uncertainty the federal government’s fall budget and various incoming data, but those are fairly ordinary areas of uncertainty and the US tariff situation is enough to keep the outlook extremely clouded.

- Given the above, we expect to see another dual-scenario outlook, albeit a more optimistic one than April’s on the activity front.

- As the aforementioned data since April suggests, this will include a less negative estimate for Q2 GDP with slightly higher core inflation. If they do publish a single, central forecast, this would be a surprise and suggest that the BOC has more confidence in its ability to make projections despite aforementioned uncertainties.

- The policy statement should reflect this better-than-expected economic activity evolution as well, suggesting as Gov Macklem has previously that reality has unfolded much closer to Scenario 1 than Scenario 2. There could be some note of continued elevation in core inflation metrics. In June the BOC noted "firmness in recent inflation data" which could stand, though "softer but not sharply weaker" economic activity could sound a little more positive this time.

- Once again, however, we do not expect any firm forward guidance given tariff uncertainty.

BOC: Data Calls For Further Patience (2/4)

Looking at recent inter-meeting data informing the likely rate hold Wednesday (more detail in our PDF preview):

- June's Labour Force Survey saw much-better-than-expected employment (+83.1k, vs 0.0k consensus) and unemployment rate (6.9%, vs 7.1% consensus) data. This was the biggest overall monthly job gain in 6 months.

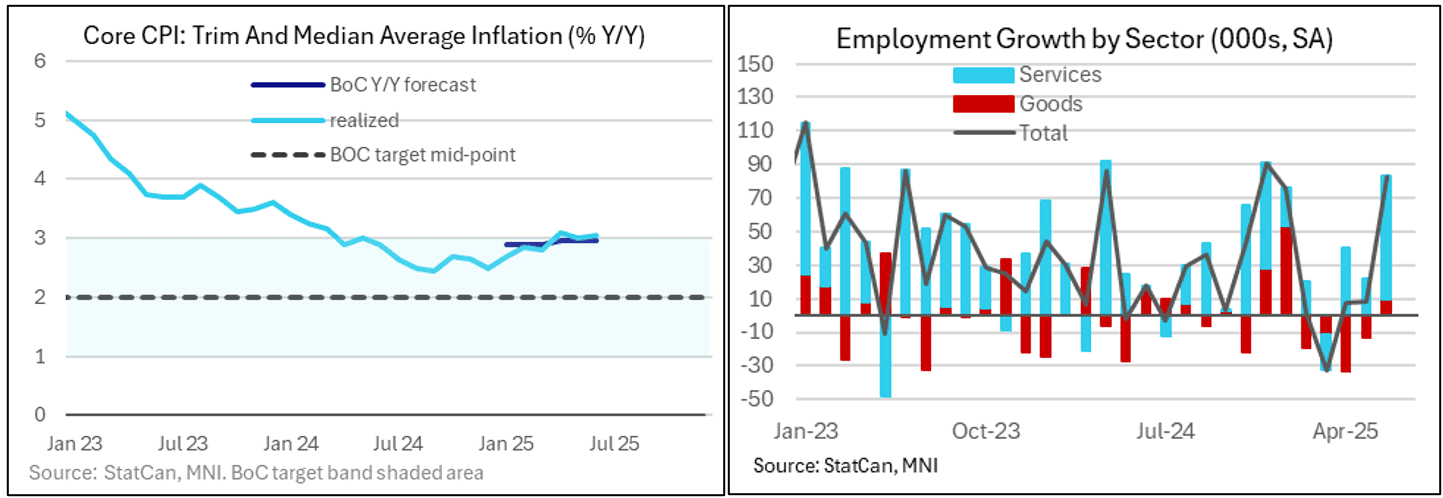

- June CPI report showed stronger-than-anticipated price pressures. The main takeaway was the slightly-higher-than-expected print for the BOC's preferred inflation metric: with the trim / median average finishing Q2 averaging 3.05%, higher than the 2.95% "forecast" by the BOC in its April projections (its two tariff scenarios were 2.9% or 3.0%). For the quarter, Y/Y trim averaged 3.03% and median 3.07%. June didn't see a major upside miss on the major core metrics, but when combined with the upside "miss" in headline CPI (a below-BOC target 1.8% Y/Y in Q2, but vs 1.5% in April's BOC projections), the apparent acceleration in inflation momentum is reason enough to stay on hold.

- The advance estimate for June's retail sales is for 1.6% M/M gains - which would be the fastest pace since December.

- The Bank of Canada's quarterly Business Outlook Survey (BOS) and Canadian Survey of Consumer Expectations (CSCE) showed broadly that the economy and inflation expectations stabilized between February (the Q1 survey) and May (the Q2 report released this month). Neither survey's findings are an obstacle for further BOC rate cuts, but nor do they make a compelling case for further easing.

- The latest monthly GDP reading showed a below-consensus -0.1% M/M reading for April, with the May flash estimate also pointing to a 0.1% contraction (we get the data on July 31, the day after the BOC decision). That was indicative of quarterly growth of -0.3% in Q2, if June comes in flat (which looks like pessimistic assumption given other activity data for the month). This would be between the BOC's two scenario estimates of -1.3% and 0.0% in its April projections. This comes after the latest quarterly GDP release on May 30 showed Q1 annualized GDP +2.2%, above the BOC forecast for +1.8%

USDJPY TECHS: Key Resistance Remains Exposed

- RES 4: 151.21 High Mar 28

- RES 3: 150.49 High Apr 2

- RES 2: 149.38 50.0% retracement of the Jan 10 - Apr 22 bear leg

- RES 1: 148.80/149.18 High Jul 29 / High Jul 16 and the bull trigger

- PRICE: 148.47 @ 18:12 BST Jul 29

- SUP 1: 146.92 20-day EMA

- SUP 2: 146.11/145.86 50-day EMA / Low Jul 24

- SUP 3: 145.16 61.8% retracement of the Jul 1 - 16 bull cycle

- SUP 4: 144.21 76.4% retracement of the Jul 1 - 16 bull cycle

A bull cycle in USDJPY remains in place. The latest recovery signals the end of the corrective phase between Jul 16 - 24. Attention is on key resistance and the bull trigger at 149.18, the Jul 16 high. A break of this hurdle would confirm a resumption of the uptrend. Pivot support to monitor is 146.11, the 50-day EMA. A clear breach of it would instead signal scope for stronger reversal. First support is at 146.92, the 20-day EMA.