MNI ASIA MARKETS ANALYSIS - Trump/Putin Meet Outcomes in Focus

MNI (NEW YORK) -

HIGHLIGHTS:

- USD Index pinned to 50-dma - although the trend signal is flattening out for first time in Trump's term

- Equities finish near record highs, but it's outcomes that matter in Trump-Putin meeting

- Leaders play down odds of immediate peace deal, with White House seeing more opportunity at subsequent meetings

US TSYS: Bear Steepening Caps Poor Week For Long End

The Treasury curve bear steepened Friday, to complete a week of underperformance at the long end.

- The rise in yields across the curve was steady through the US session. There was no particular event or headline that stood out, but recent whiffs of stagflation (following on from Thursday's hot producer price report) and follow-through from European long-end weakness (partly on fiscal concerns) appeared to weigh.

- While July retail sales appeared solid in our view (and led to an slight upgrade to the Atlanta Fed's GDPNow est for Q3), the August prelim UMichigan survey was decidedly stagflationary with weaker sentiment and higher inflation expectations, while industrial production was uninspiring and import price inflation was a little firmer than expected despite lower revisions.

- This environment tested Fed rate cut expectations slightly with December Fed implied rates up 2bp, but it was the long end that bore the brunt. In one notable move, 5s30s hit a fresh cycle high (109.11bp).

- For the week, the theme was twist steepening, with the short-end actually a little stronger (2Y down 0.8bp) vs sharp rises further down the curve (+9.8bp for 10s).

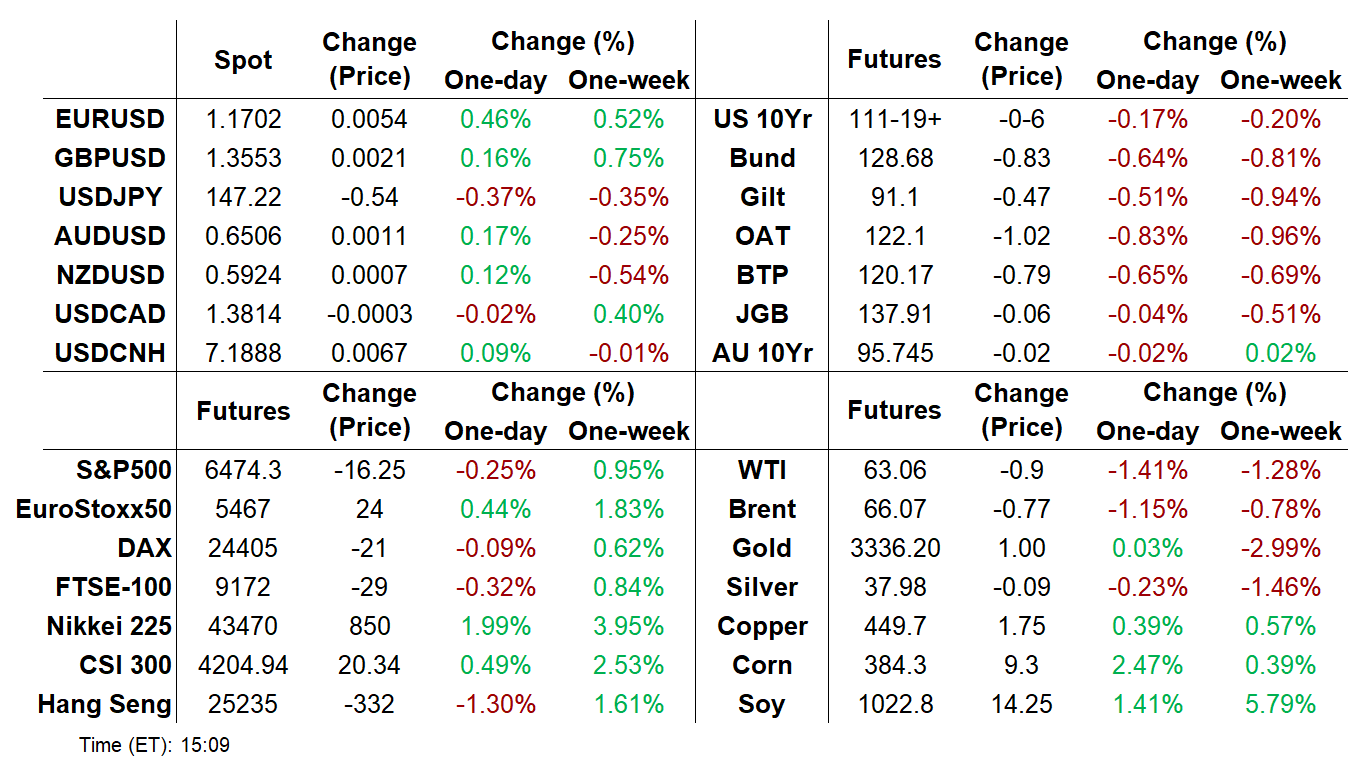

- Latest Friday levels: The 2-Yr yield is up 2.2bps at 3.7547%, 5-Yr is up 2.8bps at 3.8414%, 10-Yr is up 3.9bps at 4.3238%, and 30-Yr is up 5bps at 4.9224%. Sep 10-Yr futures (TY) down 6/32 at 111-19.5 (L: 111-17.5 / H: 111-30.5).

- Attention later in the day turns to Alaska for developments from the Trump-Putin summit on the Ukraine conflict.

- Next week's calendar includes residential sector data (housing starts, homebuilder sentiment, existing home sales) and flash August PMI data as well as a few Fed speakers (notably Waller and Bowman) ahead of Friday's keynote speech by Fed Chair Powell as part of the annual Jackson Hole symposium Aug 21-23.

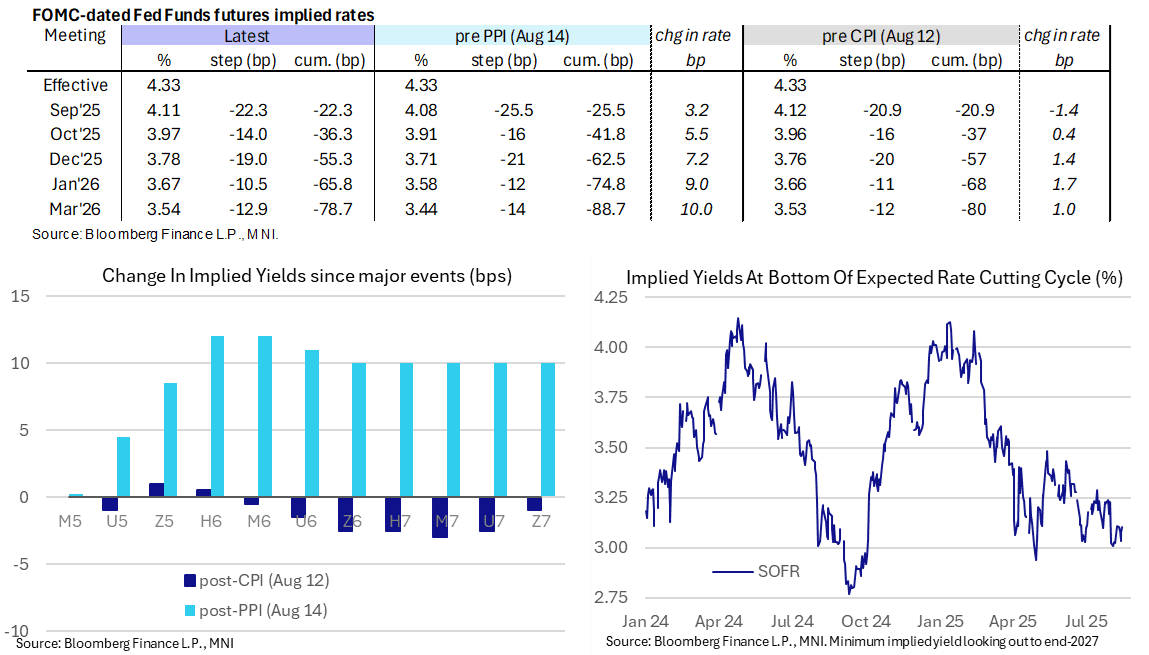

STIR: Fed Rates Eyeing Close With Fewest 2025 Cuts Since NFPs

- Fed Funds implied rates have steadily pushed higher over the past two hours as US fixed income more broadly appears to slowly catch up with sizeable European underperformance earlier in the session (with its lack of fresh catalysts).

- The day’s moves, with the Dec 2025 rate now 2bp higher, modestly extend yesterday’s hawkish reaction to very strong PPI inflation and leaves the near-term path above pre-CPI levels except for September.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 36.5bp Oct, 55.5bp Dec, 66bp Jan and 78.5bp Mar.

- The SOFR implied terminal yield of 3.105% (SFRH7) is 2.5bp higher on the day as it just nudges back below fully pricing five cuts from current levels having flittered either side of this since the hugely weak revisions to the July NFP report on Aug 1.

- The Trump-Putin meeting in Alaska at 1500ET is still to come today.

- In firm focus next week, Fed Chair Powell’s Jackson Hole address on Friday at 1000ET. It’s in the unenviable position of coming ahead of August NFP and CPI/PPI reports before the Sept 17 FOMC decision.

- Chicago Fed’s Goolsbee (’25 voter), historically one of the most dovish FOMC members, reiterated today that he needs to see at least another inflation report to be sure persistent price pressures aren’t picking up.

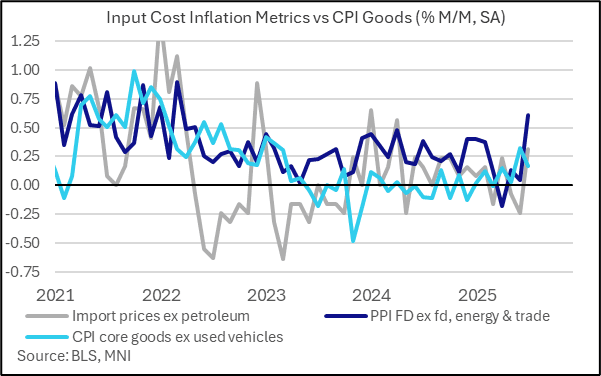

MNI US Macro Weekly: Inflation Two-Step

- The latest edition of US “inflation week” brought twists and turns, as CPI data appeared to suggest a slight reprieve from tariff-related price pressures but a hot PPI report told a different story.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

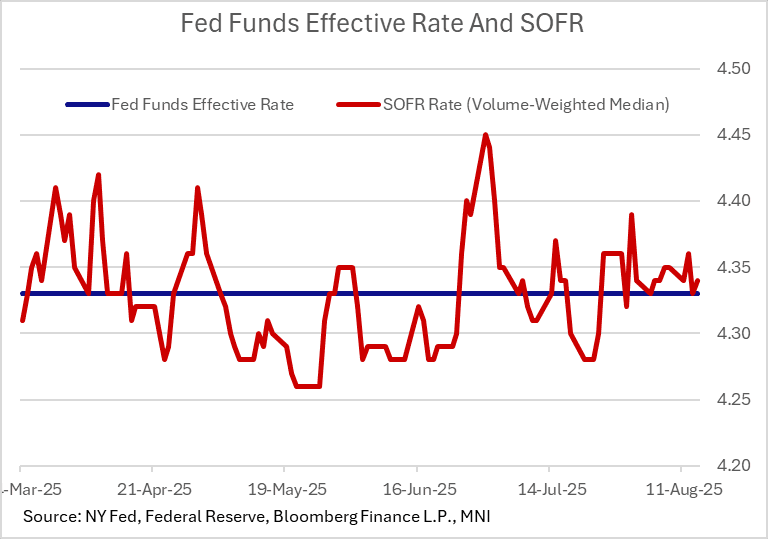

US TSYS/OVERNIGHT REPO: Secured Rates Should Remain Firm On Coupon Settles

Secured rates were modestly firmer Thursday, amid upside pressure from Treasury bill auction settlements (net $42B cash raised). Though SOFR rose 1bp to 4.34%, it remained within recent ranges (and other rates remained steady).

- Upward pressure is likely to be sustained Friday due to $35B in net Treasury cash raised via coupon settlements.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.34%, 0.01%, $2767B

* Broad General Collateral Rate (BGCR): 4.32%, no change, $1169B

* Tri-Party General Collateral Rate (TGCR): 4.32%, no change, $1144B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $114B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $253B

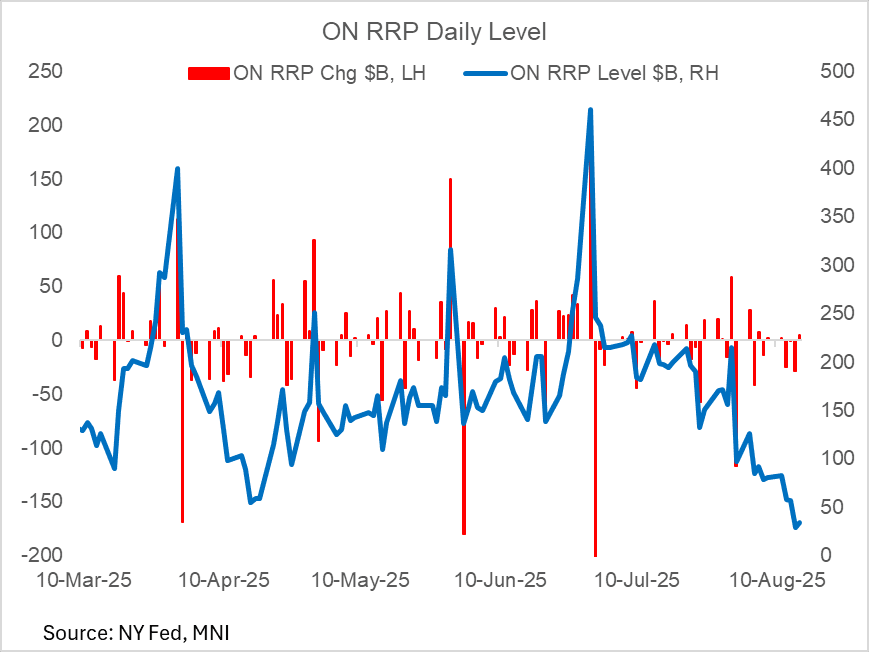

US TSYS/OVERNIGHT REPO: ON RRP Ticks Higher, Still Subdued

Overnight reverse repo facility takeup rose Friday for the first session in 4, by $4.9B to $33.8B. This brings it off Thursday's post-2021 low but keeps it under $100B for a 9th consecutive session. The number of counterparties likewise ticked only slightly higher, to 16 from 14.

- It's unlikely that outside of month-/quarter-end dynamics that ON RRP takeup will move sharply higher again for the foreseeable future, with some expectations that it will wind down to effectively zero by September as Treasury bill issuance continues apace.

OPTIONS: US Options Roundup - Aug 15 2025

Friday's US rates/bond options flow included:

- SFRU5 96.06/96.12cs, traded 0.75 in 5.5k

- SFRU5 96.00c, traded 3 in 3k

- SFRV5 96.18/96.25cs, traded 2.75 in 3.5k

- SFRV5 96.37/96.62cs, traded 1.375 in 10k and 3.5 in 14k

- SFRZ5 96.18^, traded for 28.5 in 1.5k

- SFRZ5 96.50/96.62cs, traded 2 in 4k

- 0QZ5 97.37/97.50cs vs SFRU5 95.93/96.12cs, traded -0.5 in 2k

FOREX: USD Index Pinned to 50-dma as Putin Shakes Hands with Trump

- USD slipped against all others Friday, with a poor set of retail sales and Uni of Michigan sentiment numbers meeting a higher-than-expected import price index to further stimulate concerns over a stagflarionary phase in the US economy. The USD Index trades either side of the 50-dma which, notably, has begun to flatten out after maintaining a solid downtrend throughout 2025.

- JPY is the strongest currency in G10, extending the breakout and bearish conclusion of the consolidation phase in USD/JPY. Recent weakness puts the price through support drawn off the early August lows as well as 146.71, a key retracement. Price action this week marks a full reversal of the previously overbought condition, keeping the downside argument in focus.

- Anticipation ahead of the Putin-Trump meeting has reached fever pitch. Footage showing the Presidents shaking hands in Alaska has helped ease concerns over a hostile meeting, but it's the outcomes that will matter to markets - particularly as equities hold at alltime highs. Any signs of progress toward a ceasefire would be warmly received by risk sentiment - although both Trump and Putin cautioned against a optimistic outcome in comments to press.

- We noted earlier in the week the pressure building on USD/HKD, with price action not matching the pattern of HKMA intervention. That move extended overnight, and is still building at typing, putting spot down to new pullback lows of 7.8119 shortly after the European open. Overnight swap rates have surged further still Friday (hitting 1.7% at typing), well ahead of the 0.3% prevailing rate mid-week and should continue to support a recovery in HIBOR fixes ahead. Today's 1m HIBOR fixed higher by 41bps, hitting 1.45% for the highest fix since mid-May. It's these factors that should work against the HKD carry trade (selling HKD, buying USD), evident in the further tightening of the HKD forward discount today: down 975 points from as high as 1270 this month.

- Focus in the coming week shifts to Jackson Hole and Powell's comments on Friday. With the September meeting still in flux - any conviction toward tipping the board toward a rate cut at the next FOMC will be carefully watched, but it's a hawkish outturn that could be more consequential for markets, as OIS prices a near 90% chance of easing on September 17th.

BONDS: EGBs-GILTS CASH CLOSE: Long-End Weakness Cements Bear Steepening Move

European yields roundly rose Friday to conclude a week of bear steepening.

- Yields more or less rose continuously following the cash open, through to the close. 30Y German yields notably hit a post-2011 year high, with yields across the space closing near the session highs.

- There wasn't an obvious catalyst for the move on the day, with the most logical explanation that it was a continuation of recent trends including fiscal concerns in Germany/UK as well as idiosyncratic factors such as and Dutch pension fund reform.

- Added to this are potential concerns over US inflation, amid Thursday's hotter-than-expected producer price data, and today's solid retail sales and surprise jump in UMichigan consumer inflation expectations.

- The German and UK curves both bear steepened on the day, cementing bear steepening on the week. Vs last week, German yields: 2Y +1.7bp, 10Y +9.8bp; UK yields: 2Y +3.4bp, 10Y +9.5bp.

- Periphery/semi-core EGB spreads widened modestly; BTPs reversed the tightening to Bunds seen earlier in the week.

- The Trump-Putin summit on Ukraine will be the focus after the week's close. Next week brings a relatively quieter schedule, with UK July CPI and flash August PMIs featuring.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.7bps at 1.973%, 5-Yr is up 5.7bps at 2.34%, 10-Yr is up 7.6bps at 2.788%, and 30-Yr is up 8.3bps at 3.35%.

- UK: The 2-Yr yield is up 2.5bps at 3.933%, 5-Yr is up 3.8bps at 4.09%, 10-Yr is up 5.5bps at 4.696%, and 30-Yr is up 7.2bps at 5.564%.

- Italian BTP spread up 2.2bps at 80.1bps / French OAT up 2.2bps at 68.1bps

EUROPE OPTIONS: Significant Lean Toward Put Structures (And Outrights) To End The Week

Friday's Europe rates/bond options flow included:

- RXU5 126.50p, bought for 1 in 5k

- RXV5 128/126.5ps, bought for 50.5 in 2.5k

- ERH6 98.06/98.00/97.93p ladder x1 with ERM6 98.06/98.00/97.93p ladder x2, bought for -2.75 in 5kx10k

- ERU6 98.37/98.18/97.93p ladder, bought for 2.75 in 10k

FX OPTIONS: Expiries for Aug18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1560(E1.1bln), $1.1575(E678mln), $1.1600-05(E606mln), $1.1640-50(E1.2bln), $1.1800(E683mln)

- USD/JPY: Y147.90-00($544mln)

- AUD/USD: $0.6475(A$542mln), $0.6500-10(A$689mln)

| Date | GMT/Local | Impact | Country | Event |

| 18/08/2025 | 0900/1100 | * | Trade Balance | |

| 18/08/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 18/08/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 18/08/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 18/08/2025 | 1430/1530 | DMO likely to publish FQ3 consultation agenda | ||

| 18/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 18/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 19/08/2025 | 0800/1000 | ** | EZ Current Account | |

| 19/08/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 19/08/2025 | 1230/0830 | *** | CPI | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 19/08/2025 | 1810/1410 | Fed Vice Chair Michelle Bowman | ||

| 20/08/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 20/08/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 20/08/2025 | 2350/0850 | * | Machinery orders | |

| 20/08/2025 | 0200/1400 | *** | RBNZ official cash rate decision |