MNI US Macro Weekly: Inflation Two-Step

Aug-15 18:29By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

Executive Summary

- The latest edition of US “inflation week” brought twists and turns, as CPI data appeared to suggest a slight reprieve from tariff-related price pressures but a hot PPI report told a different story.

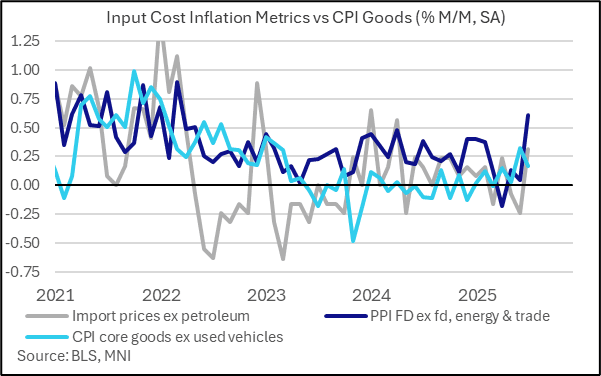

- The July CPI report saw further acceleration in monthly core inflation as expected but it was driven by the volatile supercore category. Instead, core goods inflation, an area of focus for tariff passthrough clues, was surprisingly soft. This category only maintained the still-solid monthly clip seen in June, whilst median core goods inflation moderated after a strong increase in June.

- This would see a 25bp September Fed cut get fully priced in, with some analysts pulling forward their expectation for the next cut amid rising speculation that the Fed could even go with an outsized 50bp reduction (reminiscent of September 2024) next month.

- But very strong July PPI data, with undertones of businesses passing along higher tariff-related costs to consumers, reversed those dovish cues - keeping a Sept cut largely priced but no longer quite a sure thing.

- Otherwise, activity data was mixed. In the major non-inflation release, July's retail sales report was generally in line with expectations, with the main upside surprise being an upward revision to June's data suggesting a more solid end to consumption in the second quarter than previously estimated. Overall despite some pockets of weakness and the caveat that the figures are in nominal terms and thus overstate real sales, this report should bolster confidence in consumer solidity entering Q3.

- Indeed, current GDP estimates based on recent data peg Q3 growth at steady to slightly stronger than in Q2. Surveys painted a mixed picture, with Empire State activity much stronger than expected, but UMichigan consumer sentiment falling sharply amid a leap in inflation expectations. Jobless claims data, as ever, portrayed a low hiring, low firing labor market environment.

- A few more names for Fed Chair were floated in media reports, but President Trump appeared to suggest that the shortlist was still limited (3-4 names, which we surmise includes the two "Kevins" Warsh and Hassett, along with Waller), while adding that he will announce his choice "a little bit early".

- In the meantime, Treasury Secretary Bessent who is leading the search said Fed rates should be 150bp lower, possibly with a 50bp cut in September. However, three of the four regional Fed presidents who are in the FOMC voting rotation this year (Goolsbee, Musalem, Schmid) to varying degrees wouldn't commit this week to support a 25bp September cut.

- Next week's data calendar is slightly lighter, with residential sector data (housing starts, homebuilder sentiment, existing home sales) and flash August PMI data featuring.

- Instead the attention will be on Fed communications. The July FOMC minutes Wednesday, while slightly stale as usual, could offer some color on that meeting's deliberations over a rate cut.

- But all eyes will be on the Jackson Hole Symposium Aug 21-23. Most attention will of course mostly be on any nod Chair Powell makes (or doesn’t) to a potential September Fed rate cut in his Friday keynote.