US TSYS: Bear Steepening Caps Poor Week For Long End

The Treasury curve bear steepened Friday, to complete a week of underperformance at the long end.

- The rise in yields across the curve was steady through the US session. There was no particular event or headline that stood out, but recent whiffs of stagflation (following on from Thursday's hot producer price report) and follow-through from European long-end weakness (partly on fiscal concerns) appeared to weigh.

- While July retail sales appeared solid in our view (and led to an slight upgrade to the Atlanta Fed's GDPNow est for Q3), the August prelim UMichigan survey was decidedly stagflationary with weaker sentiment and higher inflation expectations, while industrial production was uninspiring and import price inflation was a little firmer than expected despite lower revisions.

- This environment tested Fed rate cut expectations slightly with December Fed implied rates up 2bp, but it was the long end that bore the brunt. In one notable move, 5s30s hit a fresh cycle high (109.11bp).

- For the week, the theme was twist steepening, with the short-end actually a little stronger (2Y down 0.8bp) vs sharp rises further down the curve (+9.8bp for 10s).

- Latest Friday levels: The 2-Yr yield is up 2.2bps at 3.7547%, 5-Yr is up 2.8bps at 3.8414%, 10-Yr is up 3.9bps at 4.3238%, and 30-Yr is up 5bps at 4.9224%. Sep 10-Yr futures (TY) down 6/32 at 111-19.5 (L: 111-17.5 / H: 111-30.5).

- Attention later in the day turns to Alaska for developments from the Trump-Putin summit on the Ukraine conflict.

- Next week's calendar includes residential sector data (housing starts, homebuilder sentiment, existing home sales) and flash August PMI data as well as a few Fed speakers (notably Waller and Bowman) ahead of Friday's keynote speech by Fed Chair Powell as part of the annual Jackson Hole symposium Aug 21-23.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Thursday Data Calendar: Weekly Claims, Retail Sales, Fed Speakers

- US Data/Speaker Calendar (prior, estimate)

- 07/17 0830 Initial Jobless Claims (227k, 234k)

- 07/17 0830 Continuing Claims (1.965M, 1.965M)

- 07/17 0830 Retail Sales Advance MoM (-0.9%, 0.1%)

- 07/17 0830 Import Price Index MoM (0.0%, 0.3%), YoY (0.2%, 0.3%)

- 07/17 0830 Export Price Index MoM (-0.9%, 0.0%), YoY (1.7%, 1.9%)

- 07/17 0830 Philadelphia Fed Business Outlook (-4.0, -1.0)

- 07/17 1000 NAHB Housing Market Index (32, 33)

- 07/17 1000 Business Inventories (0.0%, 0.0%)

- 07/17 1000 Fed Gov Kugler on housing market, economic outlook

- 07/17 1130 US Tsy $90B 4W, $80B 8W bill auctions

- 07/17 1245 SF Fed Daly on Bbg TV

- 07/17 1330 Fed Gov Cook on AI innovation (text, Q&A)

- 07/17 1600 Net Long-term TIC Flows (-$7.8B, --)

- 07/17 1600 Total Net TIC Flows (-$14.2B, --)

- 07/17 1830 Fed Gov Waller economic outlook (text, Q&A)

- Source: Bloomberg Finance L.P. / MNI

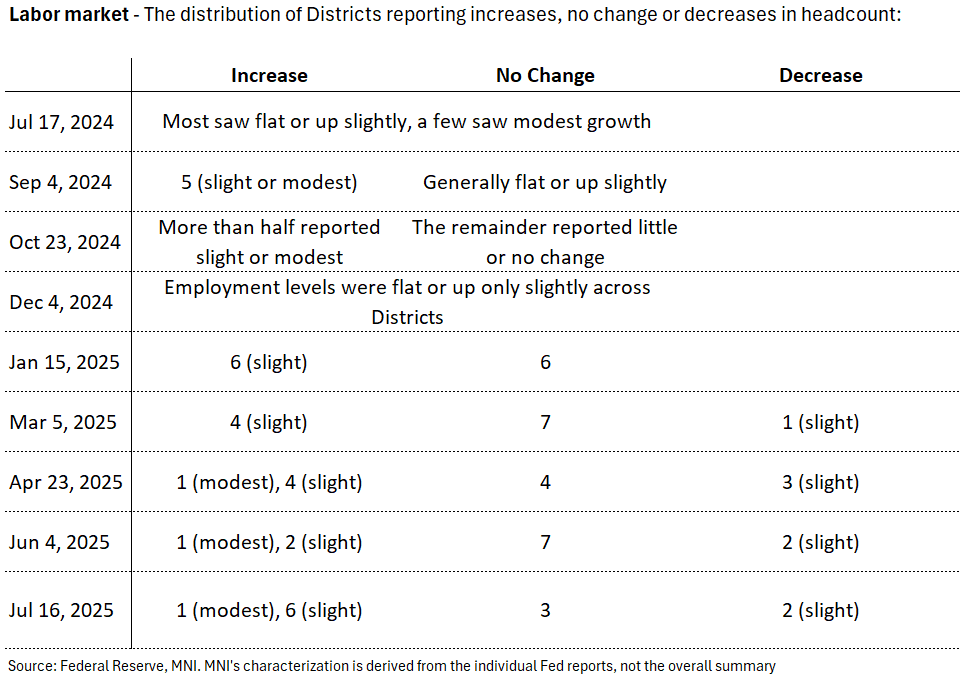

FED: Beige Book: Hiring Looking Solid Despite Lingering Uncertainty (2/3)

The July Beige Book characterizes the labor market in fairly mixed fashion, though generally stable to slightly-positive across most Fed Districts compared with the June beige book. Arguably this is the most solid Beige Book on the employment front since the start of the year, though businesses continued to report holding off on hiring plans "until uncertainty diminished" . Wages were seen as flat-to-moderate.

- The biggest shift is that 7 of 12 Districts are now reporting employment increases (Boston, NY, Cleveland, Richmond, Chicago, Minneapolis, Kansas City), vs 3 in June's report; the number reporting flat/unchanged fell to 3 (Atlanta, St Louis, Dallas) from 7; the number seeing decreases remained at 2 (Philadelphia, San Francisco).

- Labor market conditions were overall seen mixed-to-looser in some respects, with tighter immigration policy and skilled worker shortages reducing supply, but on the other hand availability improving "for many employers" amid reduced worker turnover.

- Per the report: "Hiring remained generally cautious, which many contacts attributed to ongoing economic and policy uncertainty. Labor availability improved for many employers, with further reductions in turnover rates and increased job applications. A growing number of Districts cited labor shortages in the skilled trades. Several Districts also mentioned reduced availability of foreign-born workers, attributed to changes in immigration policy. Employers in a few Districts ramped up investments in automation and AI aimed at reducing the need for additional hiring. Wages increased modestly overall, extending recent trends, with reports that ranged from flat wages to moderate growth. Although reports of layoffs were limited in all industries, they were somewhat more common among manufacturers. Looking ahead, many contacts expected to postpone major hiring and layoff decisions until uncertainty diminished."

USDJPY TECHS: Bulls Remain In The Driver’s Seat

- RES 4: 151.21 High Mar 28

- RES 3: 150.49 High Apr 2

- RES 2: 149.38 50.0% retracement of the Jan 10 - Apr 22 bear leg

- RES 1: 149.18 High Jul 16

- PRICE: 148.19 @ 17:06 BST Jul 16

- SUP 1: 146.86 Low Jul 14

- SUP 2: 145.89 20-day EMA

- SUP 3: 145.44 50-day EMA

- SUP 4: 144.23 Low Jul 7

A short-term bull cycle in USDJPY remains firmly in place - even as an acute spell of intraday volatility saw the price test Y147.00. This week’s gains reinforce current conditions. The latest rally has resulted in a breach of resistance at 148.03, the Jun 23 high, and a move through key resistance at 148.65, the May 12 high. Clearance of both levels strengthens the bull theme and opens 149.38, a Fibonacci retracement. On the downside, support to watch is 145.44, the 50-day EMA.