MNI INTERVIEW: RBA TO Cut Twice More - Ex-Economist

The Reserve Bank of Australia is most likely to make only two more cuts to the 3.6% cash rate, with the strength of the labour market firmly guiding future decisions, a former senior bank official told MNI, adding that risks skew toward fewer cuts rather than additional easing.

“My baseline is they do two more cuts, but with a much greater risk they only do one rather than three,” said Justin Fabo, founder of Antipodean Macro and the RBA’s former head of international financial markets. Labour market conditions have softened only gradually over the past three years, a trend he expects to continue, with faster or deeper easing contingent on a sharper downturn.

"The labour market is everything, and it's basically very, very gradually deteriorating," he said, pointing to July's unemployment data published this week which showed the rate tightening 10bp to 4.2%. "There's no huge red flags in any of the labour market data that we have at the moment."

Fabo’s view aligns with market pricing, which factors in a cut in November and a 3.1% cash rate by Q1, versus his earlier call for 3.0% by year-end. (See MNI INTERVIEW: RBA To Eye 2025 3% Cash Rate Floor - Ex Econ) He noted recent improvements in business surveys, while the RBA’s August Statement on Monetary Policy and Governor Michele Bullock's comments following Tuesday's 25bp cut reflected a cautious stance on inflation. (See MNI RBA WATCH: Bullock Points Toward Further Cuts)

“They’ve got 2.5% inflation, but they can’t really have any confidence at all that they’re going to undershoot their target,” he said.

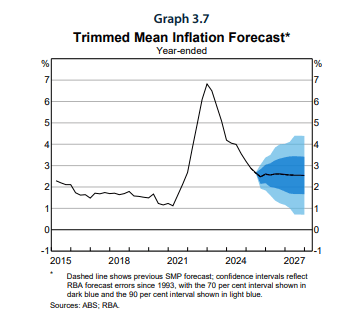

The RBA's forecasts showed underlying inflation reaching the 2.5% midpoint target by the end of 2027.

Recent housing market performance, though not a direct policy input, historically foreshadowed pressure on underlying inflation, he added, noting the Bank would continue to remain vigilant.

PRODUCTIVITY TURNAROUND

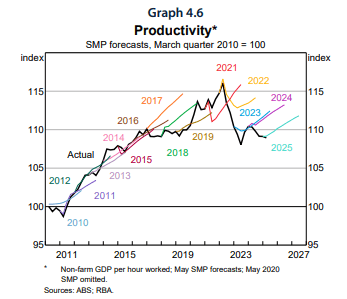

The RBA, which has been criticised for its overly optimistic view, cut its productivity forecast by 60bp to a 0.3% gain by December. Fabo welcomed the reassessment, saying it was less a change in outlook than an acknowledgement that conditions have already shifted. The Bank has been broadly accurate on unemployment and core inflation forecasts over the past year, but consistently overestimated GDP and wages growth, he noted.

“What is going on in the economy around productivity growth, in an underlying sense, matters a lot for those two variables they’ve been getting wrong,” he said, stressing the revision has little bearing on the inflation outlook. “They've basically made an assumption that has no impact on inflation or unemployment… but stay tuned.”