EU CONSUMER CYCLICALS: Consumer & Transport: Week in Review

Aug-08 14:38

As earnings fall away it is replaced by rating action - thus far only the expected names but we expect some higher beta downgrades to come. Some signs of compression as IG moved 1bp tighter but did not extend to already rejected names (VF, Groupe SEB). Earnings near completely disappear next week, as may primary.

- Diageo results were lacklustre and likely leaves leverage holding above raters comfort levels.

- Molson Coors issued more lacklustre results. Low leverage may protect it from rating action for now.

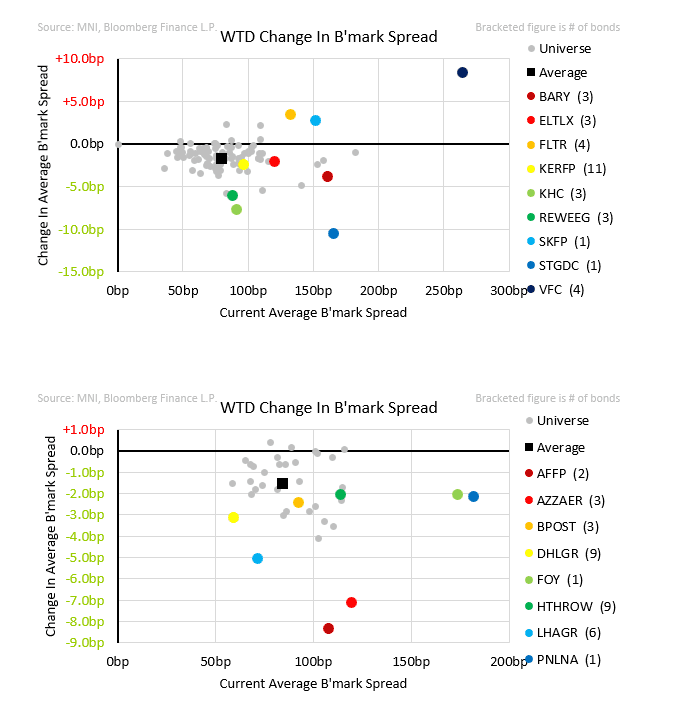

- PostNL results remained lacklustre, FY guidance was kept unchanged including for negative FCF. It is still demanding financial support from the Dutch government.

- Bpost results remained lacklustre and will leave the co levered around the mid 3-handle. FY EBIT is now expected at top end of original guidance – a low bar to beat.

- Adecco 2Q results saw volume growth and indicated outperformance vs. peers. But profitability trends remained lacklustre. It said 2H will be better and keeps its leverage target unchanged. In line with latter, it is guiding to paydown without refi the CHF225m due this year.

- InterContinental Hotels flexed its asset-light but scalable model as system growth offset the lacklustre RevPAR growth in its core US and China regions. Leverage comfortably in target has equity payouts continuing at pace.

- Walgreens Boots saga came to an end with the vast majority in all lines tendering in for cash redemption their bonds. Dollar long-end will walk away with up to a 30pt gain year-to-date. Acquirer, Sycamore, escapes potential CoC at 101.

- Amsterdam airport parent, Royal Schiphol, is given an upgrade to A+, standalone rating of A- now on par with highest-rated ADP (Paris). Reasoning behind upgrade despite sizeable capex here.

- Kellanova’s standalone ratings are affirmed by Moody’s after earnings, while it remains on review for upgrade pending the Mars guarantee. The latter on pause by the EU regulator, co still guiding to a close by year-end.

- Whirlpool is moved to negative outlook as S&P now sees leverage remaining at 5x this year. It also questions if the India sale to help with $700m of debt paydown will go ahead this year.

- Electrolux is downgraded by S&P but with the outlook stabilised. The net take from S&P is fairly optimistic. As we noted post earnings fundamentals for credit are trending upwards, but weighed on by one-offs this year.

- General Mills got a reprieve from Moody’s who holds ratings unchanged despite an expected move above its gross 4.0x threshold. It notes management efforts to reshape the portfolio into higher growth segments and recently revised UoP on yoghurt sale ($2.1b) to include debt paydown.

- Heathrow got no immediate rating action from S&P after announcing third runway spend last week, given lack of disclosure on funding details, uncertain tariff increases regulator will allow and (as always) uncertainty on if plans will proceed.

- No Primary

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUDNZD Approaches May Highs Following RBNZ Hold

Jul-09 14:37

- A relatively subdued session for the greenback has allowed NZDUSD to consolidate its most recent pull lower, after printing a fresh pullback low below 0.5980 overnight. The pair continues to exert pressure on the 50-day EMA, of which spot has not closed below since April 09. Continued weakness would signal scope for a move towards 0.5883 and 0.5847 (double bottom seen in mid-May and an important pivot level).

- AUDNZD has also extended its recovery to a seven-week high above 1.0900. Trendline support drawn from the April lows has helped underpin the latest bounce for the cross, targeting 1.0922 (May 15 high) initially, before the early April highs just above 1.10.

- As a reminder, the RBNZ held the Official Cash Rate steady at 3.25% on Wednesday as expected, but signalled further cuts may follow if medium-term inflation continues to ease in line with forecasts.

- The decision followed signs of a patchy domestic recovery, as high-frequency data from April and May suggest growth momentum has been slowing. Additionally, the committee weighed the option of a 25bp cut, citing subdued growth and the risk that heightened uncertainty may lead to sustained caution among households and firms.

MNI: US EIA: CRUDE OIL STOCKS EX SPR +7.07M TO 426.0M JUL 04 WK

Jul-09 14:30

- US EIA: CRUDE OIL STOCKS EX SPR +7.07M TO 426.0M JUL 04 WK

- US EIA: DISTILLATE STOCKS -0.82M TO 102.8M IN JUL 04 WK

- US EIA: GASOLINE STOCKS -2.66M TO 229.5M IN JUL 04 WK

- US EIA: CUSHING STOCKS +0.46M TO 21.2M BARRELS IN JUL 04 WK

- US EIA: SPR +0.24M TO 403.0M BARRELS IN JUL 04 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE -0.2% TO 94.7% IN JUL 04 WK

STIR FUTURES: BLOCK: Dec'25/'26 SOFR Flattener

Jul-09 14:27

- SOFR Flattener posted at 1016:46ET:

- -5,000 SFRZ5 96.18, post time bid vs. +SFRZ6 96.81, post time offer