EU CONSUMER STAPLES: General Mills: Moody's holds unch for now

(GIS: Baa2/BBB)

So Moody's will hold unch despite a expected rise above its gross 4.0x threshold in FY26 (12m to May-26). We have encouraged caution on the curve and it is wide of even JABHOL (6.5yr at Z+102/3.4%). We have no firm view, investors who do will have to trust mgmt that it can reset volume to growth through new product launches - it is targeting fresh pet food which it says is a fast growing market and says it is reshaping portfolio to protein demand, pointing to Cheerio's Protein Cereal and Nature Valley bars as evidence.

- Moody's notes despite ending May at net 3.7x, company targets 3.0x and will now use some of the yoghurt divestiture proceeds ($2.1b) for debt paydown (alongside the original buybacks).

- Moody's does seem optimistic on growth returning noting co is strategically reshaping portfolio.

- Unclear if S&P who has similar net 4.0x threshold will stay unch (small cash on hand means 0.1x diff. between n/g).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USD: Extending broader gains

- Some broader extension higher for the Dollar, at an intraday high against the EUR, JPY, KRW, PHP, CAD, CHF, GBP.

- The SEK is the only Currency in positive territory in G10s following the Higher inflation print in Sweden.

- Initial support in the EURUSD is still further out, down to 1.1708 Low Jun 30.

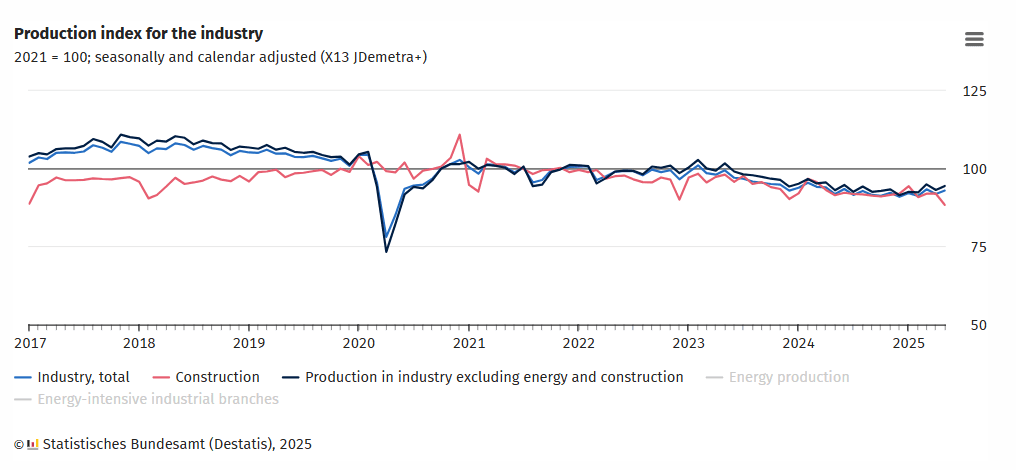

GERMAN DATA: May Industrial Production Stronger On Manufacturing, Energy

German industrial production outperformed expectations in May at 1.2% M/M, compared to consensus of -0.2% following a slight downward revision of April's rate to -1.6% (-1.4% unrevised). On a yearly basis, IP came in at 1.0% (vs -0.3% cons; -2.1% Apr revised, from -1.8% unrevised).

- This means that the orders and production data from May point in different directions (May orders, published Friday, were weak) - that is not totally uncommon; overall, our reading remains that also taking consensus into consideration, the picture in the sector is arguably brighter than what it was a couple of months ago.

- We saw risks to today's IP consensus figures following Friday's weak turnover in manufacturing print tilting to the downside - however, the correlation between the two measures was negative this month, with manufacturing production (excl. construction and energy) also up 1.4% M/M.

- Energy production was notably up, also, at +10.8% M/M while construction came in at -3.9%. Destatis doesn't comment on the energy jump - dry and sunny conditions may have boosted solar output in the month.

- Within manufacturing, drivers were automotive production (+4.9% M/M) and pharmaceutical production (+10.0%). Auto production seems to be stabilising around H2-23/H1-24 levels after some weakness around the turn of the year. Pharmaceutical production appears to have also stabilised somewhat after weakness in H2-24 and early '25. We would argue these are both sectors which can be strongly driven by foreign demand, both appear to have weak domestically-generated orders (based on Friday's data). It is too soon to tell if we will see continued growth in these sectors or whether they will remain more consistently at current levels in coming months, after moving off their lows.

- Looking a month ahead, the truck toll index for the full month of June, which correlates with the industrial production index to a decent extent, will only be published on Wednesday - but daily data already published points towards some moderate pick-up in activity last month. Sentiment, as said, stands at (partially multi) year highs in the sector.

FOREX: FX OPTION EXPIRY - Large in EUR Today

FX OPTION EXPIRY: Large Expiry in the EUR Today.

Of note:

EURUSD 4.37bn at 1.1750/1.1770.

EURUSD 1.96bn at 1.1770 (fri).

- EURUSD; 1.1700 (771mln), 1.1725 (433mln), 1.1750 (1.35bn), 1.1770 (3.02bn), 1.1800 (1bn), 1.1810 (311mln), 1.1825 (1.04bn).

- GBPUSD; 1.3600 (414mln).

- USDJPY: 144.75 (325mln), 144.90 (280mln).

- AUDUSD: 0.6500 (475mln), 0.6515 (297mln), 0.6600 (885mln).

- AUDNZD: 1.0825 (318mln).

- USDCNY: 7.1500 (520mln), 7.1700 (490mln).