EU CONSUMER CYCLICALS: InterContinental Hotels: 2Q results

(IHGLN; Baa2/BBB)

IHG showing the strength of its asset light but scalable model - very modest RevPar growth still being met with sizeable margin expansion and double digit EBITDA growth (on new hotel/room growth). Both Accor and IHG will send most FCF to equity holders now as they hold comfortably in leverage targets. IHG 31s gives +20bps above Accor and +10 above easyJet - that continues to screen relative value to us.

- 1H RevPAR +1.8% (Q2 +0.3%); daily rates +1.4% & occupancy +0.3pts

- Core Americas RevPar +1.4% - driven by pricing. Q2 was -0.5% as Occupancy fell -0.7ppts

- Greater China -3.2% on pricing (-3.6%). Q2 little changed at -3%.

- System growth +5.4%, alongside above RevPar left fee revenue +7% y/y and total group revenue +5%

- EBIT +12% y/y up to a 51.4% margin (+310bps). Core fee margin was +390bps at 64.7%; 260bps of that was operating leverage as cost base actually fell y/y while system size increased. Another +130bps came from ancillary revenue; co-branding credit card agreements and sale of loyalty points.

- FCF at €302m (vs. $131m LY), buybacks and dividends totalled $605m increasing debt by $580m. Targeting $1.1b in equity pay-outs this year.

- EBITDA growth of 10% limits impact to leverage to +0.3x, now at 2.7x. Affirms target of 2.5-3.0x. $565m of cash, front maturity is the £300m Aug -25 line for which we would expect refi as it guides to leverage ending the year ~2.75x.

- 1H gross room revenue was $16.7b, +3.7% y/y: $10.5b franchised, $5.9b under management contracts and only $0.3b directly in owned/leased.

- Has 999k rooms across 6.8k hotels, 2/3 in midscale, 1/3 in luxury

- Pipeline is skewed to China at 35% (20% of system currently) and US at 26% (45% currently)

- Signings are 51% in midscale and 49% upscale/luxury - part of its strategy to push lux weight up

FY25 Guidance - on track to meet consensus which is at:

- RevPar +2%, System growth +4%, to leave revenue +6%

- EBITDA +11%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: Preview 3Y Note Auction

Tsy futures are near midmorning lows (TUU5 103-20.5, -.38 vs. 103-19.75 low) ahead of the $58B 3Y note auction (91282CNM9) at 1300ET, WI is currently at 3.881%, 9.1bp rich to last month's tail. Results will be available shortly after the competitive auctions closes at 1300ET.

- June auction recap: Treasury futures showed little reaction after $58B 3Y note auction (91282CNH0) tailed 0.5: 3.972% high yield vs. 3.967% WI; 2.52x bid-to-cover vs. 2.56x prior.

- Peripheral stats saw indirect take-up climb to 66.78% vs. 62.37% prior; direct bidder take-up retreated to 18.03% from 23.71% prior; primary dealer take-up 15.19% vs. 13.92% prior.

ITALY AUCTION PREVIEW: On offer this week

MEF has announced it will be looking to sell the following at its auction this Friday, July 11:

- E3.25-3.50bln of the new 3-year 2.35% Jan-29 BTP (ISIN tba)

- E3.00-3.50bln of the 3.25% Jul-32 BTP (ISIN: IT0005647265)

- E1.25-1.75bln of the 3.85% Oct-40 BTP (ISIN: IT0005635583)

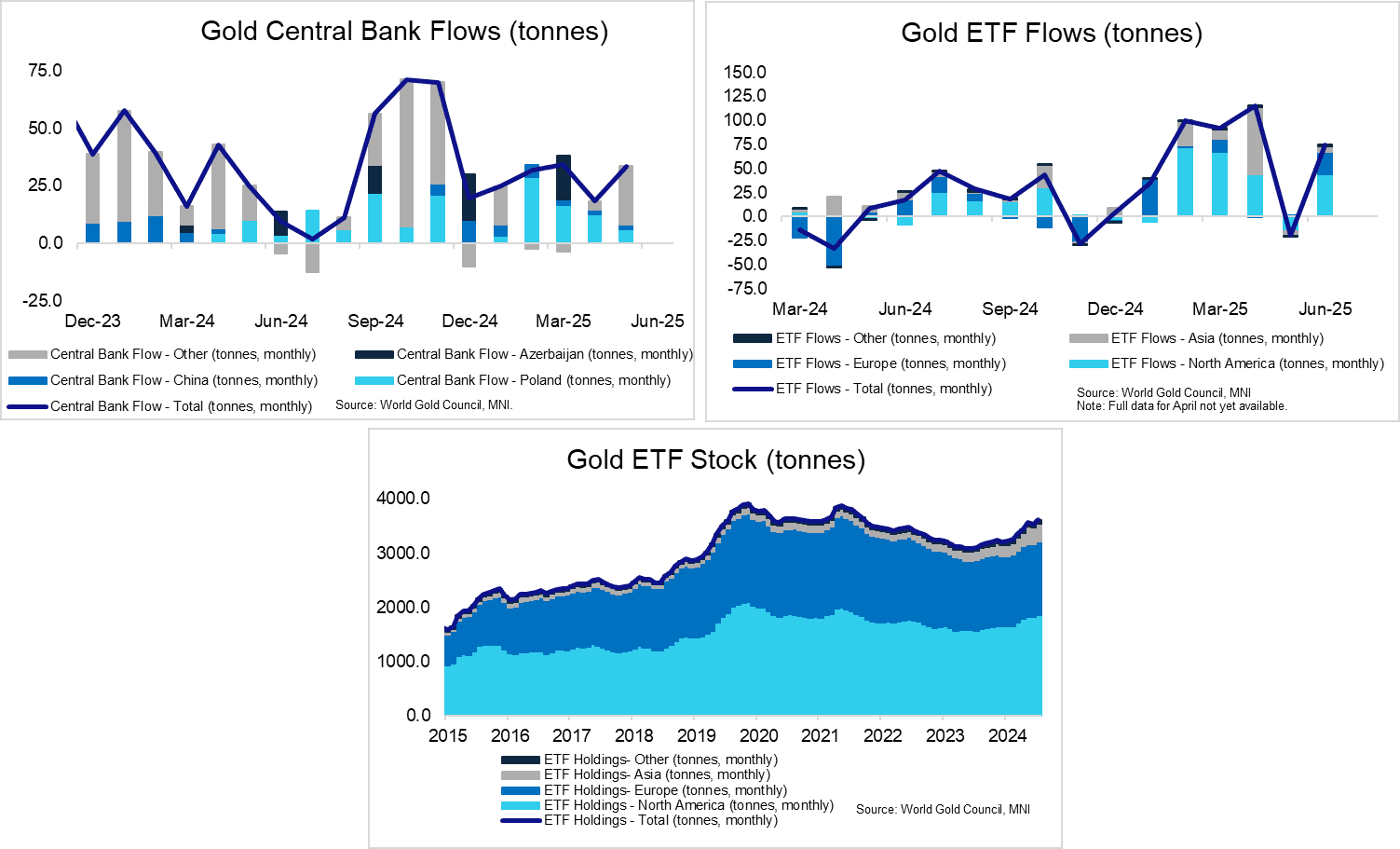

GOLD: Central Banks Still Buying; Strong ETF Inflows In June

Demand data from the World Gold Council (WGC) has been updated for June (ETFs) and May (central banks). While investor flows will be sensitive to economic/geopolitical developments and price/technicals, central banks are considered to have more inelastic demand. Latest data indicates another month of strong central bank purchases in May, a trend which should provide structural support to spot prices even if the technical picture has turned less bullish.

- There were ETF inflows equivalent to 74.6 tonnes in June, spearheaded by the US (44.3 tonnes) and Europe (23.1 tonnes). Asian ETFs, which saw huge inflows of 69.3 tonnes in April, saw a more modest 5.3 tonne inflow in June (after a 4.8 tonne outflow in May).

- The stock of gold in Asian ETFs is still substantially smaller than the US and Europe, but the 321 tonnes held in June 2025 is almost double that of a year ago (179 tonnes).

- Central Banks purchased 33.5 tonnes of gold in May, according to WGC data. There were familiar inflows from Poland (6.2 tonnes, though smaller than Feb-Apr purchases), alongside notable purchases from Kazakhstan and Turkey.

- China reported purchases of 1.9 tonnes in May, and more recent reserves data indicates another 2.2 tonnes were added in June. As always, there will be speculation that these figures could be underreporting actual PBOC purchases.