EMISSIONS: EU End-Of-Day Carbon Summary: EUAs/UKAs Rise On Mixed Signals

{EUAs Dec25 are trending higher, supported by gains in EU equities amid optimism over a potential ceasefire in Ukraine and the US chip tariff ceiling for the EU. However, losses in TTF gas prices, driven by steady storage injections, may be limiting further carbon upside. Meanwhile, UKAs Dec25 are also rising, supported by strength in EUAs and the BOE’s decision to cut interest rates to a two-year low, from 4.25% to 4%, in line with market expectations. The market is pricing in one additional rate cut by year-end to around 3.5%, as the BOE forecasts inflation will peak at 4% in September.

- EUA DEC 25 up 1.27% at 71.89 EUR/t CO2e

- UKA DEC 25 up 1.35% at 51 GBP/t CO2e

- TTF Gas SEP 25 down 0.9% at 32.951 EUR/MWh

- NBP Gas SEP 25 down 1.1% at 81.21 GBp/therm

- Estoxx 50 up 1.4% at 5335.65

- The latest EU ETS CAP3 auction cleared at €70.1/ton CO2e, up 0.04% compared with the previous EU auction at €70.07/ton CO2e according to EEX.

- Last week’s gains in ICE EUA futures initially resulted in a move through resistance at €72.79, the Jul 3 high. However, prices have faded since - instead pushing prices closer to nearby support - which held into the Monday low. The next downside level to watch lies at €68.71, the May 19 low. A clear break of this level would reinstate a bearish theme and open €66.44, a Fibonacci retracement. Any continuation higher would open €76.75, the Jun 13 high and a key bull trigger.

- EUA Auction Calendar Week Ahead (Calendar Week 33) - A total of 11.3mn EUAs will be auctioned next week, with 4 auction sessions will be held. The latest EU ETS auction cleared at €70.1/ton CO2e, down 2.64% w/w, oscillating between 50 and 100-day averages and falling below the 10-day averages.

- EUA Dec25 implied volatility as of 6 Aug was at 28.47%, remained stable compared with the 28.34% from the last trading session in the prior week. EUAs Dec25 edged down by 0.07% w/w, while open interest in call contracts increased, suggesting growing expectations of upside potential, while participants foreseeing limited short-term disruptions.

- The UKA auction cleared at a premium to the Dec25 futures contract for a second consecutive session, though no clear pattern in the spread has been identified, ICE data showed.

- Uniper cut direct CO2 emissions by 24% y/y in H1 2025 to 6.3mn tonnes, down from 8.3mn tonnes in the same period of 2024, and expects full-year emissions to fall significantly below 2024 levels, it said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 52W BILL AUCTION: HIGH 3.925%(ALLOT 32.25%)

- US TSY 52W BILL AUCTION: HIGH 3.925%(ALLOT 32.25%)

- US TSY 52W BILL AUCTION: DEALERS TAKE 31.91% OF COMPETITIVES

- US TSY 52W BILL AUCTION: DIRECTS TAKE 4.87% OF COMPETITIVES

- US TSY 52W BILL AUCTION: INDIRECTS TAKE 63.22% OF COMPETITIVES

- US TSY 52W AUCTION: BID/CVR 3.23

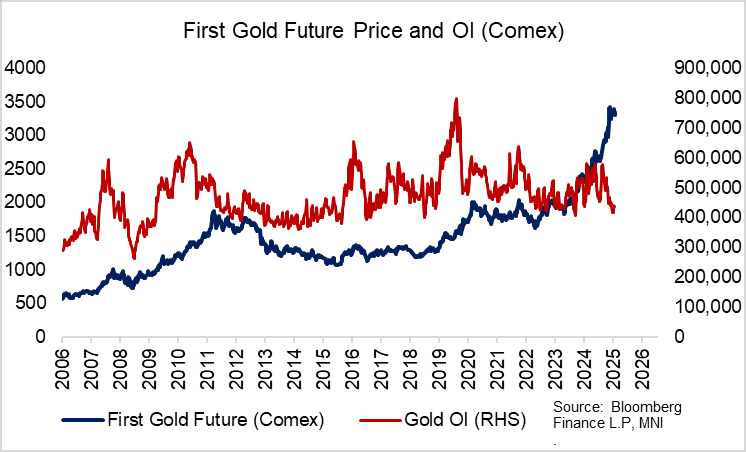

GOLD: Back Below $3,300; Near-term Focus On Tariff Letters

Spot gold has pushed through yesterday’s low, now down 1.2% today and back below the $3,300 handle. The pullback in gold comes in tandem with the recent dollar bounce, with the DXY finding support at the long-term uptrend drawn from the 2011 low. Key support and the bear trigger in gold is $3,248, the June 30 low.

- After an aggressive rally through 2024 and Q1 2025, Gold has been relatively rangebound since mid-April. Continued tariff policy uncertainty, global fiscal concerns and geopolitical risk have not been enough to encourage a retest of the April 22 all-time high of $3,500.1.

- Near-term focus will be on the remaining US “tariff letters” to be sent out over the coming days. However, but risk assets have generally taken the announcements made thus far in their stride, limiting any positive spillovers into gold.

- In the week to July 1 (prior to Trump’s “tariff letter” announcement), non-commercial net longs in Comex gold futures rose by 7k contracts to 202k. That brought total net longs to the most since mid-April, and may have factored into the pullback over the last four sessions.

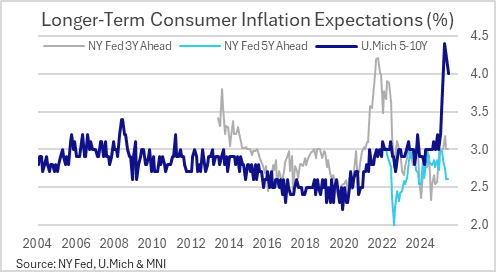

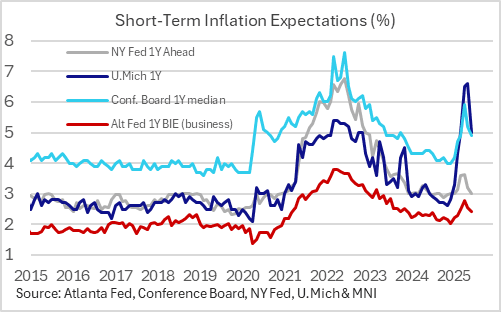

US DATA: NY Fed Survey Adds Further Evidence Of Anchored Inflation Expectations

Overall inflation expectations receded in June for the 2nd consecutive month in the New York Fed's Survey of Consumer Expectations, following April's apparent peak amid tariff announcements. It adds to evidence that inflation expectations are "well anchored", or at least, certainly not becoming de-anchored even as tariffs are expected to start feeding into goods price inflation over the coming months.

- 1Y ahead median expected inflation fell to a 5-month low 3.02% (3.20% prior), well down from the 3.63% peak in April. 3Y expectations were steady at 3.00%, and has now been at a rounded 3.0% for 6 of 7 months with the exception being 3.2% in April. And longer-term expectations were also steady, with the 5Y median remaining at 2.61%, a joint 16-month low.

- With almost all FOMC members citing inflation expectations as a key determinant in whether higher tariff-related inflation could lead to broader and more sustained price pressures, continued deceleration in expectations in what is a well-regarded report will provide a little more confidence that a resumption of the easing cycle can begin sooner rather than later.

- While the NY Fed survey has been the steadiest of its kind through the tariff episode, other surveys (UMichigan / Conference Board) have also reflected a moderation in consumer price expectations albeit still at elevated levels.

- In other NY Fed survey results, mean expected probability of losing a job dipped 1.8pp to 14.0% (5-month low), with one-year expected household income growth rising 0.2pp to 2.9% (4-month high), though median expected earnings growth fell 0.2pp to 2.5% and expectations of finding a job in 3 months if one's job is lost fell 1.1pp to 49.6%. Spending growth expectations dipped slightly but remained near the 5% Y/Y area (4.9% after 5.0%).